Banks Warn of Growing Energy-Related Risks in Mortgage Portfolios

Across Europe, banks are trying to figure out how to handle a growing risk lurking in residential mortgage portfolios: energy consumption.

Latest Videos

The information you requested is not available at this time, please check back again soon.

Across Europe, banks are trying to figure out how to handle a growing risk lurking in residential mortgage portfolios: energy consumption.

British Land Co. has sold its stake in Sheffield’s Meadowhall Shopping Centre, one of the largest shopping malls in the UK, to Norway’s sovereign wealth fund.

China’s latest housing initiative is aimed at vacant properties, a major pain point in a crisis that’s dragged on for almost three years. But analysts say the package of measures is still too small to end the rout.

Foreign buyers swooped in to purchase Chinese stocks on Friday as Xi Jinping’s government announced a slew of measures to bolster the housing market.

China’s property stocks need a sustainable turnaround in order to foster investor confidence that this year’s broader equities recovery can maintain, or even increase its momentum.

Aug 25, 2023

, Bloomberg News

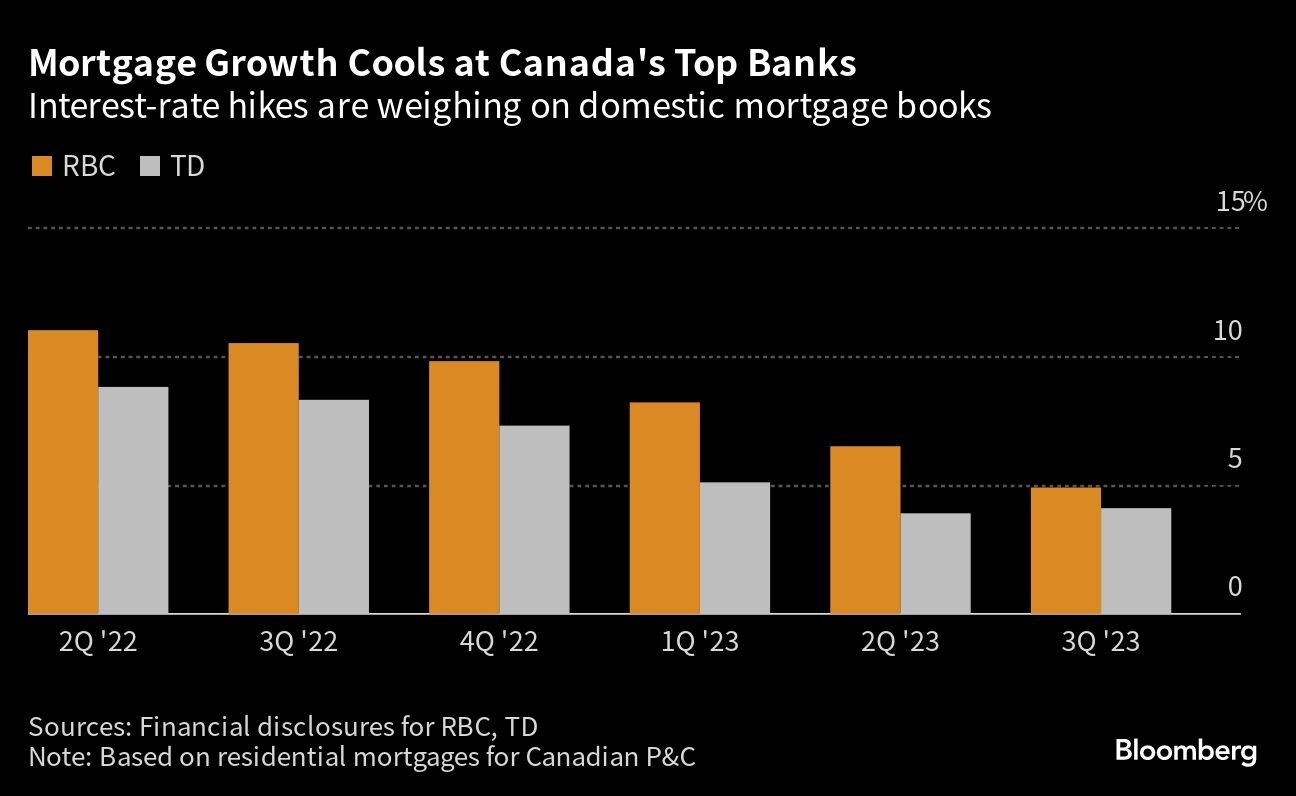

Mortgage data from Canada’s two biggest banks are painting a picture of homeowners straining under high borrowing costs.

Royal Bank of Canada, the country’s largest lender, disclosed that 43 per cent of its Canadian residential mortgages had an amortization period of longer than 25 years, as of July. That’s up from 40 per cent a year earlier, and just 26 per cent in January 2022.

Canadian banks have allowed customers to stretch payments for longer periods to help them bring down their monthly payments after a rapid rise in rates. Unlike in the U.S., it’s difficult for homeowners to lock in their rates for long periods. Most either have mortgages where the rates are fixed for one to five years, or variable-rate mortgages that reset with every move in the central bank rate.

That has meant higher payments for millions of borrowers after the Bank of Canada lifted its policy rate by 475 basis points in less than 18 months. RBC’s posted rate on variable mortgages is now above 7 per cent, from around 2.5 per cent before the central bank began tightening.

The situation has also brought about the return of mortgages that are amortized for more than 35 years. At the start of last year, those didn’t exist in RBC’s Canadian mortgage book; now, such loans represent 23 per cent of the portfolio.

Growth in mortgages, meanwhile, has slowed.

Toronto-Dominion Bank said 48 per cent of its Canadian mortgages had an amortization period of more than 25 years as of July, up from 35 per cent the year prior. Like RBC, it has experience a surge of loans being extended to more than 35 years.

In a conference call with analysts Thursday, Michael Rhodes, Toronto-Dominion’s head of Canadian personal banking, said the bank reached out to stretched borrowers who hit their so-called “trigger rate,” or the point where their payments on variable-rate mortgages may no longer cover interest.

Toronto-Dominion offers those customers options such as lump-sum payments, increased term payments and the option to switch to fixed rates.

The Bank of Canada raised its benchmark overnight rate to 5 per cent in July, the highest level in more than two decades.

Related