May 28, 2021

America's US$795B rescue saved jobs. No one's sure how many

, Bloomberg News

U.S. jobs report a preview of what we will see in Canada as we recover: CIBC's Mendes

VIDEO SIGN OUT

It’s been a lifeline for millions of U.S. small businesses during the pandemic, or a bloated bureaucratic nightmare, depending who you ask -- and maybe a bit of both.

The U.S. government’s sprawling Paycheck Protection Program officially wraps up its 13-month existence on Monday. Economists will be studying PPP for far longer than it was operating to figure out how many jobs it saved.

One of the most cited studies, led by a Massachusetts Institute of Technology economist David Autor, pegged the jobs saved by PPP’s first round at a fairly low 2.3 million -- at a high cost of US$224,000 per job. At the other end of the spectrum, two Federal Reserve economists estimated in January that PPP preserved 13 million jobs at a more modest US$43,000 each.

Overall, the government distributed more than 11.6 million forgivable loans worth over US$795 billion to small businesses since April 2020, an unprecedented program for a segment of the economy that rarely receives direct aid -- let alone bailouts -- during economic crises.

But the PPP was made for unprecedented times. The local economy, which bore the brunt of the financial hit from shutdowns, needed to be saved and fast, along with the tens of million of workers employed by small firms.

The program, which was extended twice by Congress, has been beset with operational glitches since the initial round, with lenders livid over having received insufficient guidance in how to process loans and borower complaints that the largest banks were favoring existing customers over other loan applicants.

More recently, some lenders have complained the agency running the program, the Small Business Administration, hasn’t provided enough information about how much money was left, leading to a scramble to get in last-minute applications.

The agency kept lenders informed about the funding level on a weekly basis through the program’s lender portal, said Shannon Giles, an SBA spokeswoman.

“There’s sort of a PPP PTSD, just because it’s been a significant struggle now for a long time, and you also know that the program fundamentally changed from round one to round two,” said Kurt Chilcott, president of a PPP lender in San Diego, CDC Small Business Finance. He, nonetheless, called PPP a success.

Here’s a closer look at the PPP in three charts:

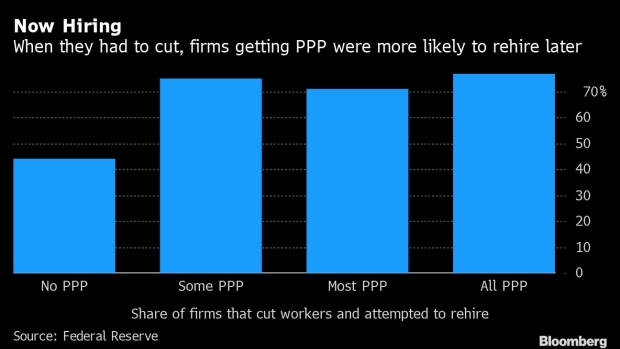

About 46 per cent of small businesses that had their PPP loans fully funded were forced to cut jobs at some point since March 1, 2020, while 71 per cent of those that got no PPP loans said they reduced their workforce, according to a 2021 Federal Reserve survey.

Companies getting PPP loans, which were forgivable under conditions including spending a majority of the funds on payroll, were much more likely to try to rehire the workers later, the survey showed.

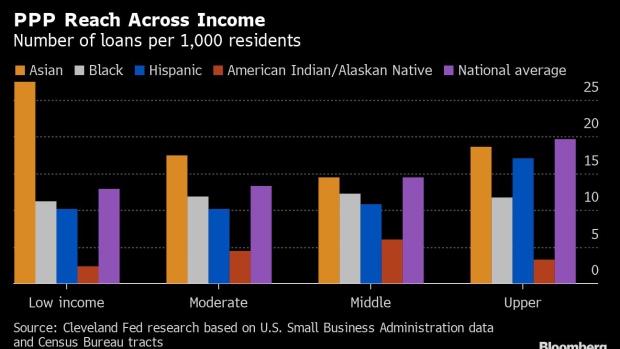

The broad-based program was not evenly distributed, however. Larger companies with ties to banks were able to get loans worth millions of dollars without having to offer proof of hardship, while tiny businesses and sole proprietors struggled with paperwork, worried about ever-changing rules to get the 1 per cent loans forgiven.

Upper-income areas received substantially more loans than lower-income communities, according to research by the Cleveland Fed. Minority groups, aside from Asian Americans, struggled to tap into the program as much as Whites, data show.

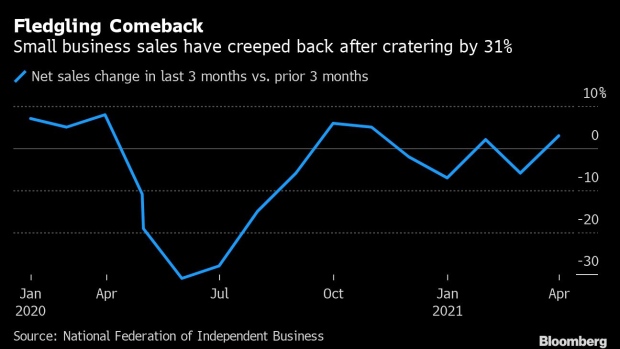

But overall the loans helped keep local businesses afloat during the depths of the pandemic and government-imposed quarantines. In June 2020, sales of small businesses slumped by almost a third compared with previous three months, according to the National Federation of Independent Business. They are now recovering, with revenue up 3 per cent on that basis in April this year.