The rapidly-changing dynamics of the mortgage market have pressured alternative lending stocks this year, leading one analyst to warn there could be more room for their share prices to continue falling in the coming months.

“While these depressed levels may signal an attractive entry point, we believe caution and patience remain the appropriate strategy heading into [second-quarter] results and likely for the remainder of the year,” Jaeme Gloyn, an analyst with National Bank of Canada Financial Markets, said in a note on Tuesday.

Shares of Home Capital Group Inc., EQB Inc., Timbercreek Financial Corp. and First National Financial Corp. have fallen between 12 and 35 per cent since the beginning of the year, with Home Capital the biggest laggard. Those stock declines underperformed the broader S&P/TSX Financials subgroup, which is down 11.3 per cent year-to-date.

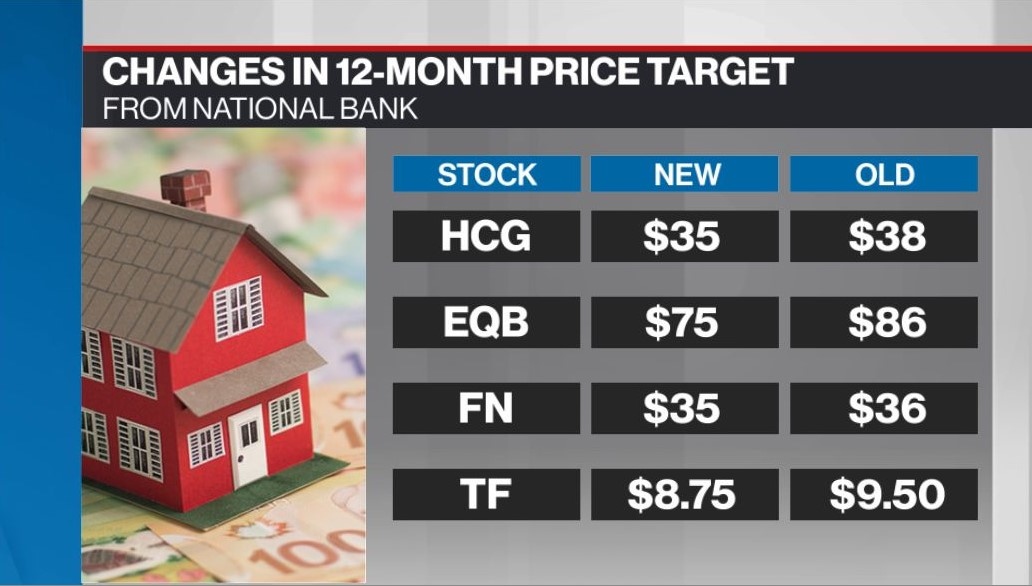

Gloyn cited a myriad of potential downside risks for mortgage stocks and lowered his 12-month price targets on all four companies. His stock recommendations remain unchanged. Home Capital and EQB are rated as outperform (the equivalent of a buy). First National and Timbercreek are rated as sector perform (the equivalent of a hold).

He said the regulatory backdrop for mortgage companies “remains unfavourable for the foreseeable future” since Canada’s banking regulator has announced plans to cap loan-to-value thresholds for reverse mortgages and readvanceable mortgages, and could announce further measures to safeguard against potential housing market vulnerabilities.

The impact of rising interest rates and a housing slowdown are also factors.

“In the near term, we believe the rapid increase in mortgage rates will most visibly transmit through reduced mortgage origination volumes,” Gloyn said.

“Longer term, we could see the impact of ‘payment shocks’ on renewing borrowers' flow through credit performance, assuming borrowers face difficulty servicing a higher mortgage payment.”

He said EQB is his preferred stock pick in the sector because of the diversification in its loan portfolio and funding channels, and its banking operations compared to other alternative lenders.

“While these fundamental strengths do NOT provide EQB with immunity, the company is more favourably positioned to manage through the above-noted risks in our view,” he said.

Home Capital is more exposed to residential mortgages and real estate investors, he said, although the company’s excess capital could lead to improved return on equity.

While Gloyn said First National’s diversification and recurring revenue model will work in its favour, the company is very sensitive to changes in mortgage origination volumes.

First National reported Tuesday mortgage origination volumes for single-family properties fell 10 per cent to $6.8 billion in its latest quarterly results due to lower housing activity. Although it noted single-family mortgage originations were well above pre-pandemic levels.

Lastly, he said Timbercreek has a good-quality loan portfolio and should benefit from stability in the commercial real estate sector.

As he cautioned that mortgage stocks are likely to remain under pressure until the risk outlook improves, he said employment trends and central bank messaging on monetary policy will be key to watch.

“We believe more widespread employment losses (e.g., Shopify, tech players) will pressure mortgage stocks lower, potentially to previous crisis trough levels that would offer investors an attractive entry. A dovish turn from the Federal Reserve and/or Bank of Canada could also cause a change in our currently softer view,” Gloyn said.