Feb 25, 2019

Barrick swings hard for Newmont – maybe too hard: Liam Denning

, Bloomberg News

Hostile bids bring out the worst in people. On the other hand, they also foster tremendous creativity.

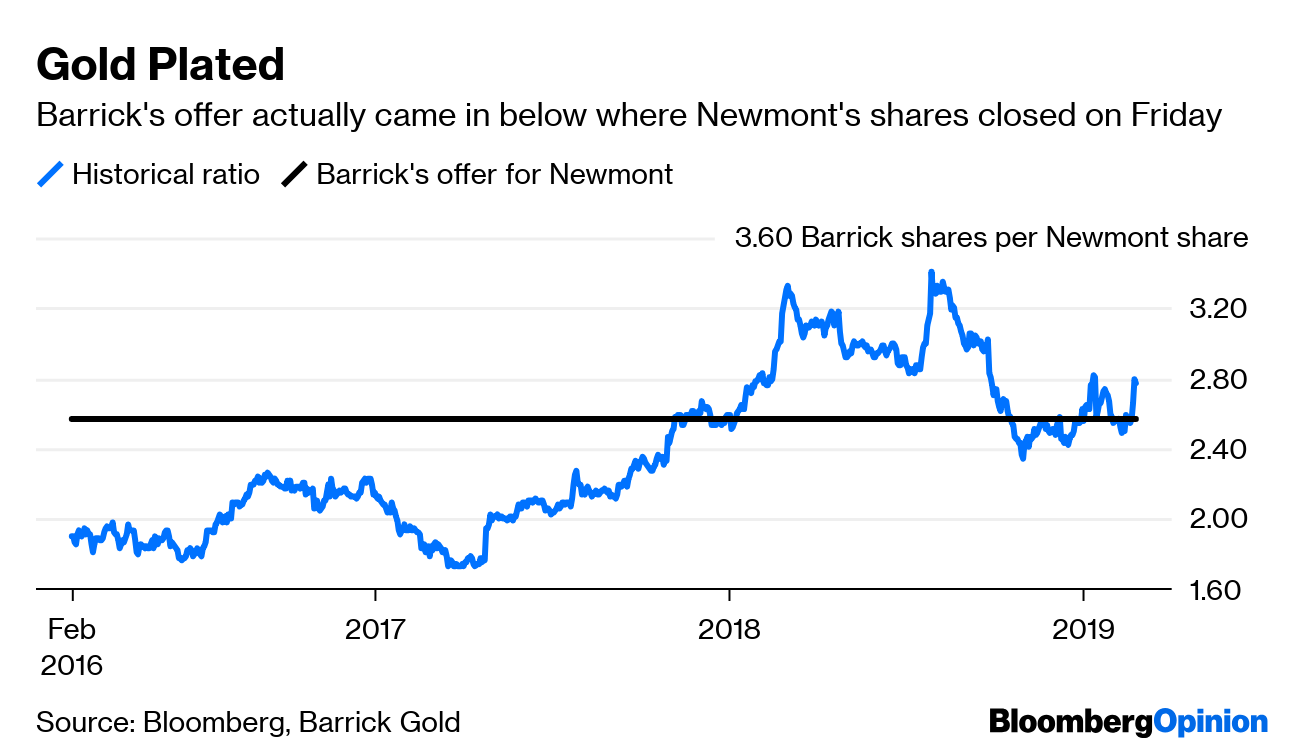

Take Barrick Gold Corp.’s (ABX.TO) US$17.8 billion unsolicited bid for Newmont Mining Corp. (NEM.TO), unveiled (or unleashed) Monday morning. Barrick led with its (publicized) letter to Newmont’s board, pointing out that on the day the latter’s recently announced deal for Goldcorp Inc. hit the wires, “your market capitalization dropped by more than the estimated present value of the synergies you announced” – about as cold as it gets in corporate-finance circles. Barrick CEO Mark Bristow followed up on the analyst call, calling Newmont’s Goldcorp bid “desperate and bizarre.” Knife, meet twist.

Where Barrick may have gone in a mite too hard is with its headline figure: US$7 billion. This is the gold miner’s estimate of the present value of synergies from its proposed all-stock deal. It is, as intended, a big number, equivalent to more than a third of Newmont’s market cap. It also comes with a footnote:

Barrick synergies are projected over a twenty year period, assuming analyst consensus commodity prices and a 5 per cent discount rate.

Just to give you a sense of how easy it is to project things over 20 years, cast your mind back to February 1999 and consider all the things that have happened since then, including (in no particular order): 9/11; the bursting of the tech bubble; the inflating and bursting of the real-estate bubble; quantitative easing; Bush-Obama-Trump; Greenspan-Bernanke-Yellen-Powell; Brexit (maybe); the Star Wars reboot (including the really bad ones); the iPhone; “Green Book” winning Best Picture. You no doubt have your own list. Either way, it’s a lot of unexpected stuff.

Quite apart from debating the utility of even offering a 20-year projection in the first place, I’m not sure a 5 per cent discount rate really cuts it here; Barrick’s own bonds maturing in 2038 yield more than that. At one point, Bristow responded to an analyst’s question with “What part of the US$7 billion don’t you think adds value?” The rather obvious answer would have been “the taxes.” And given this is an all-stock offer, the majority of any benefit (roughly 56 per cent) accrues to Barrick’s shareholders, not Newmont’s.

Even the near-term annual figure provided in Barrick’s slide deck of US$750 million a year looks aggressive, being equivalent to all of Newmont’s non-depreciation operating expenses. Taking Barrick’s guidance at face value, though, taxing it and discounting it at 10 per cent, taking off the US$650 million break fee that would go to Goldcorp, and it spits out an implied value of about US$3.4 billion, which isn’t nothing.

Synergies, of course, are very much in the eye of the beholder (or modeler), so any estimate is just that. By leading with such a huge number, though, Barrick rather opened itself up to the question (which duly came on the call) as to why it wasn’t offering a premium for Newmont.

Bristow’s response that the US$7 billion net present value of the synergies is the premium suffers from (a) the dubious nature of that figure and (b) the prevailing tendency not to take synergies estimates at face value at the best of times. Plus, the lion’s share of Barrick’s estimates relate, as they should, to the two companies’ overlapping operations in Nevada. That prompted yet more questions as to why the two companies couldn’t just agree some sort of joint venture there without all this unpleasantness. Barrick said it tried, but Newmont demanded too much, something Newmont effectively disputed in its Monday-morning rebuttal.

In certain respects, Barrick’s arguments are valid. Newmont’s bid for Goldcorp didn’t look terribly compelling (see this). Newmont’s sudden uncovering on Monday of US$165 million a year of annual “full potential cost and efficiency improvements” (which are on top of and somehow different from the US$100 million of synergies unveiled originally) may be intended to address this but suffers from the same credibility issue as Barrick’s big number.

Most of all, Bristow’s observation that miners too often build new capacity in order to retain control, rather than collaborate, is spot on and gets to the heart of why consolidation is warranted in this commodity. Yet, as my colleague David Fickling has pointed out, the current frenzy of deal-making risks prioritizing empire-building over value creation; a risk that increases as we head into hostile territory. It is telling that both stocks are down as of writing this, taking off about US$600 million or so in value. Strange that investors would leave US$7 billion of value, and more, on the table like that. Possibly, they just don’t see it.

Liam Denning is a Bloomberg Opinion columnist covering energy, mining and commodities. He previously was editor of the Wall Street Journal's Heard on the Street column and wrote for the Financial Times' Lex column. He was also an investment banker.