Jan 9, 2020

Bed Bath & Beyond sinks after results go 'from bad to worse'

, Bloomberg News

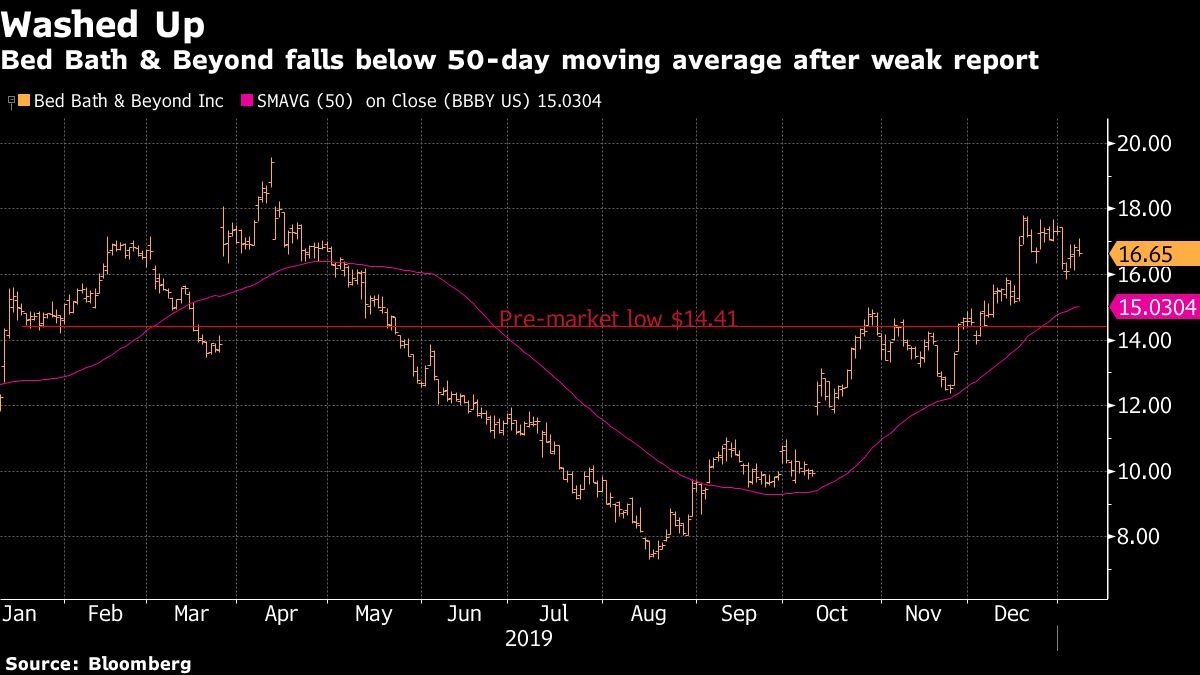

Bed Bath & Beyond Inc. shares tumbled to their lowest intraday level since Nov. 25 after the home-goods retailer pulled its year forecast after third-quarter results missed estimates. Disappointing holiday sales reports from Kohl’s Corp. and J.C. Penney further pressured the stock.

Comparable sales handily missed estimates in the quarter and EBIT margin turned negative “for the first time in recent history,” noted Guggenheim’s Steven Forbes. Loop Capital analyst Anthony Chukumba called the report “the worst we can remember since the Great Recession.”

However, Wall Street may already have been bracing for a pullback. The average analyst estimate on Jan. 7, the day before earnings were announced, was US$15, implying about 10 per cent downside from closing levels. Meanwhile, short interest on the stock is 47 per cent of float, according to data analytics firm S3 Partners.

Shares fell as much as 19 per cent to US$13.53, the most intraday since September 2018 and below its 50-day moving average. The stock ended 2019 with a 53 per cent gain after five straight years of declines.

Loop Capital, Anthony Chukumba

Third-quarter results were “much worse than expected” and highlight the “steep uphill climb” new President and CEO Mark Tritton faces in turning around the company.

That said, Tritton has a strong background in two areas most pressing for Bed Bath & Beyond -- merchandising and private label. In addition, the company has a “relatively strong” liquidity position, further bolstered by the recent US$250 million sale-leaseback. With this in mind, Chukumba’s willing to be “somewhat patient as we see how the turnaround unfolds (or does not).”

He maintains a hold rating on the stock, “despite things going from bad to worse.” Price target US$15.

Guggenheim, Steven Forbes

“Not only do 3Q results lower the 2020 ‘starting point,’ but we continue to see a more elongated turnaround effort,” Forbes said, adding that he doesn’t expect free cash flow “stability” until at least 2021.

Comparable sales missed expectations despite management initiatives which included elevated clearance activity, a new national Black Friday advertising campaign and an increase in the depth and frequency of promotions.

He expects comparable sales to “remain challenged,” with EBIT margin eroding by as much as 200 basis points, bringing full-year EBIT down to about $200 million and EPS to within a range of 80 to 85 cents versus his prior estimate of $1.60.

Despite slashing estimates, Forbes kept his rating at neutral, citing the potential for various near-term catalysts, including share repurchases and asset divestitures.

Raymond James, Bobby Griffin, Budd Bugatch

While the third quarter miss reinforces the reality that “turnarounds, particularly retail turnarounds, are rarely (if ever) linear,” the analysts told clients “don’t abandon ship yet.”

They believe the year forecast withdrawal “de-risks” some of the early part of this turnaround by ensuring expectations are “kept in check,” while the sale-leaseback announcement “clearly indicates that the new leadership is intent on unlocking shareholder value.”

They rate the stock strong buy, with a price target of US$17 per share and believe the potential for additional non-core asset sales, and related capital redeployment, remain positive near-term catalysts.

Morgan Stanley, Simeon Gutman

Gutman maintained his equal-weight rating given “inexpensive valuation and scope for improvement from here.” He also noted that the balance sheet is “relatively healthy” and the potential for expected asset sales to help “streamline the business and raise funds to be reinvested or returned to shareholders.”

But Bed Bath & Beyond still faces significant headwinds around its inability to sustain sales growth, its high reliance on coupons/promotions and underinvestments in the business, all at a time when “competition is intensifying and the home furnishings category is migrating online at a fast pace.”

As such, he sees about 20 per cent downside to his current US$12 price target.