Apr 28, 2023

Bets offering 2,400% payout on U.S. default lure growing crowd

, Bloomberg News

Consumer spending keeping U.S. economy afloat for now: Strategist

VIDEO SIGN OUT

In what is a traditionally moribund corner of Wall Street, speculators are piling into a bet that once seemed unthinkable: that the U.S. government will default on its debts.

With the Treasury Department inching ever closer to running out of cash — most estimates give it another few months — trading in the derivatives, known as credit-default swaps, is growing. The amount of money tied to the contracts, which will reward investors if the U.S. misses any payments, has increased roughly eight-fold since the start of the year.

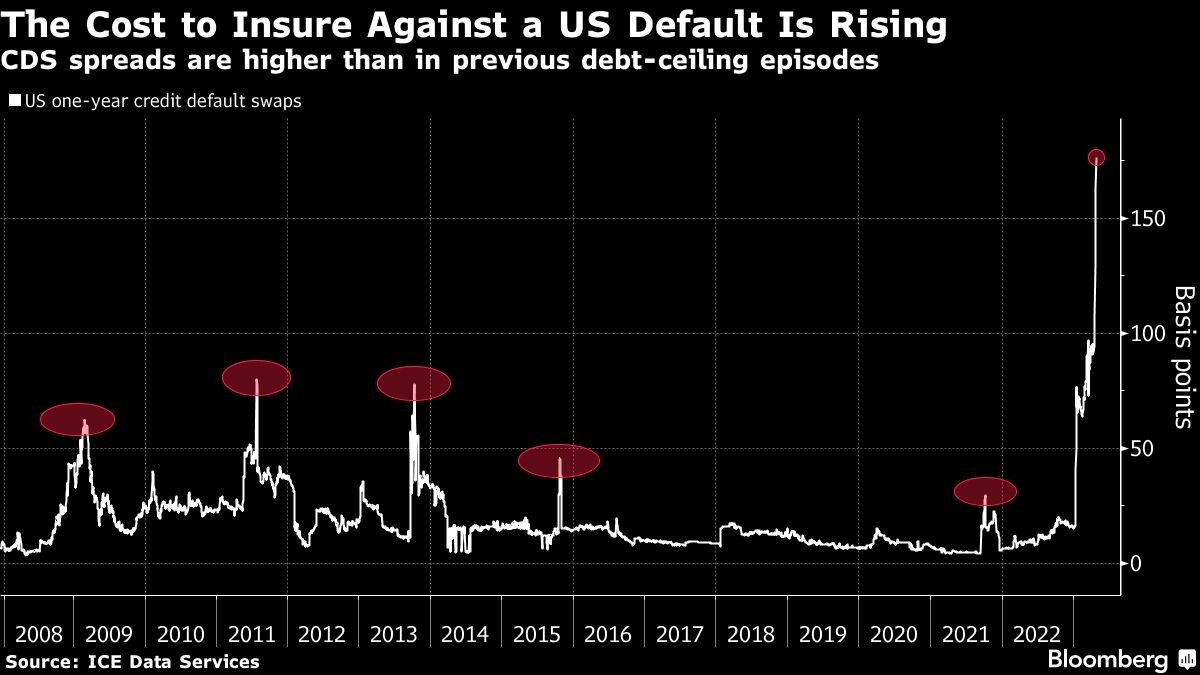

This isn’t the first time that a mini-mania around this trade has erupted. There were episodes back in 2011, 2013, and to a lesser extent 2021. But this time, it all feels a bit different. For one, there’s a greater chance of a lapse in payments. The polarization in Washington is now so extreme that there’s no guarantee Republicans and Democrats can broker a deal to lift the debt ceiling in time to avert a crisis.

And there’s an added sweetener for speculators. A quirk in the derivatives market means they can take advantage of the rock-bottom prices on long-term U.S. bonds to juice gains on the contracts should the U.S. actually default. With some Treasuries recently trading below 60 cents on the dollar — the result of the Federal Reserve’s rapid-fire series of interest-rate hikes — the potential payout could exceed 2,400 per cent, according to Bloomberg calculations.

“In Washington people think it’s like 30 per cent likely to happen, and on Wall Street people think it’s like zero to 5 per cent that this doesn’t get resolved,” Boaz Weinstein, chief investment officer at US$4.3 billion hedge fund Saba Capital Management LP, said in an interview.

Weinstein, who rose to prominence a decade ago when he took on JPMorgan Chase & Co. in what became known as the London Whale episode, noted on Twitter earlier this week that he had been “interested” in getting in on the trade but failed to get his hands on enough of the contracts to make it worth his while.

This underscores a crucial point about the market: As much as it’s grown, it remains highly illiquid (Net notional outstanding was only $5 billion at the end of March, equal to just a fraction of the U.S. bond market, according to Depository Trust & Clearing Corp. data.) And given the idiosyncrasies of the settlement process, there’s no guarantee the CDS will actually pay out, even if America does briefly miss a debt payment.

It can be hard to fathom the possibility of a U.S. default. The nation has never reneged on its debts, and the sanctity of America’s creditworthiness is a pillar of the global financial system. After all, Treasuries are commonly regarded as the “risk-free” asset — used to determine the cost of capital around the world.

Yet Wall Street, despite having seen this manufactured crisis get resolved time and again in recent years, is starting to get nervous once more.

The spread on one-year credit-default swaps, the most popular contracts for wagering on a missed payment, has surged in recent days, touching a record 1.75 percentage points on Thursday, according to ICE Data Services prices going back to 2007.

Put another way, it costs US$17,500 to insure $1 million of U.S. debt against default for a year (the contract is actually priced in euros.) That’s up roughly 10-fold since the beginning of 2023, and compares to less than $400 for Germany.

This angst is visible in the U.S. Treasury-bill market, too. Investors are demanding higher yields on the bills that would mature around the time of a potential default to compensate for the risk they may not get paid, even for just a short while.

Subadra Rajappa, head of U.S. interest-rate strategy at Societe Generale SA, says that while surging CDS spreads don’t necessarily suggest the U.S. is any more likely to default, “it’s an indication of the political environment we are in, and the potential for brinkmanship.”

Just Wednesday, Republican House Speaker Kevin McCarthy squeaked a debt limit bill through the chamber that also included trillions of dollars in budget cuts targeting President Joe Biden’s policy priorities. The White House, however, has dug in on its refusal to cave to GOP demands to attach spending cuts to raising the $31.4 trillion debt ceiling.

“I’m happy to meet with McCarthy, but not on whether or not the debt limit gets extended,” Biden said. “That’s not negotiable.”

‘CHEAP HEDGE’

In a credit-default swap, buyers make payments to a seller, who provides a payout if a borrower fails to make good on its obligations. That payout is essentially equal to the difference between the par value and market value of the underlying financial asset.

Most CDS contracts let the buyer choose between a number of bonds as the underlying asset, and buyers will typically choose the one with the lowest price to maximize their profits.

Because some longer-dated U.S. Treasuries are trading below 60 cents on the dollar, a buyer willing to pay the roughly $17,500 it costs to insure $1 million of U.S. debt for a year could receive the equivalent of more than $400,000 in the event of a default.

Of course, that’s assuming investors scoop up the Treasuries now with cash on hand, and not wait until the bonds potentially get more expensive as the debt ceiling approaches.

The cost to protect against non-payment is also rising fast, likely as CDS sellers increasingly account for the deep discounts on long bonds when determining premiums, according to RBC Capital Markets’s Blake Gwinn.

Still, “it feels like a cheap hedge in an environment when the odds of technical default are higher than usual and the payout is attractive relative to the upfront payment,” Rajappa said.

BAD BET

The wager has plenty of detractors.

Some say there are simply better, more accessible ways to hedge or profit from a potential US debt debacle.

For others, history has proven that lawmakers are capable of setting aside their differences before the clock runs out, even if it will ultimately require some 11th-hour deal making.

They say the chances of a deal getting done before CDS are triggered is especially high given a three-day grace period built into the contracts. Markets would react so badly in that intervening period, the thinking goes, that elected officials would have no other choice but to quickly hammer out a deal.

“It’s every couple of years, the same old, same old. A default is never going to happen,” said Mark Holman, a partner at TwentyFour Asset Management, a London-based investment firm that specializes in fixed-income securities.

Still others make the case that even if the US were to miss a debt payment, CDS holders still wouldn’t be assured a profit.

A so-called determination committee under the oversight of the International Swaps & Derivatives Association would ultimately have to decide if the swaps pay out, and market watchers say a lack of historical precedent (not withstanding a late payment on some maturing T-bills in 1979) would make what’s already a nebulous process even murkier.

“Unclear? Confusing? Undefined? Yes,” said Jim Bianco, who runs his own macro research firm. “Count us among those who think the credit-default swaps market for U.S. Treasury securities offers little in terms of an economic signal.”

With assistance from Hema Parmar and Tasos Vossos.