Jun 14, 2022

Big money in stocks is in mad dash to get out of U.S. Fed's way

, Bloomberg News

Recession following bear market likely scenario: Investment strategist Sam Stovall

VIDEO SIGN OUT

Despite a lot of confident predictions, nobody knows what will happen at the Federal Reserve Wednesday, never mind what the impact will be on markets. Professional investors aren’t waiting around to find out.

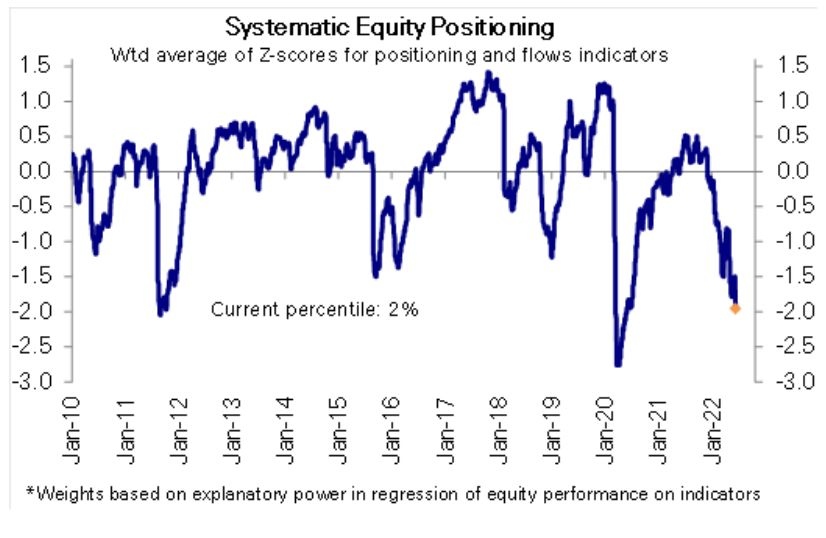

Particularly among managers who premise strategies on quantitative signals, exposure to stocks and other risky assets has been cut to the bone. Weeks of selling has pushed systemic positioning as measured by Deutsche Bank AG two standard deviations below average levels in data starting in 2010, among other examples.

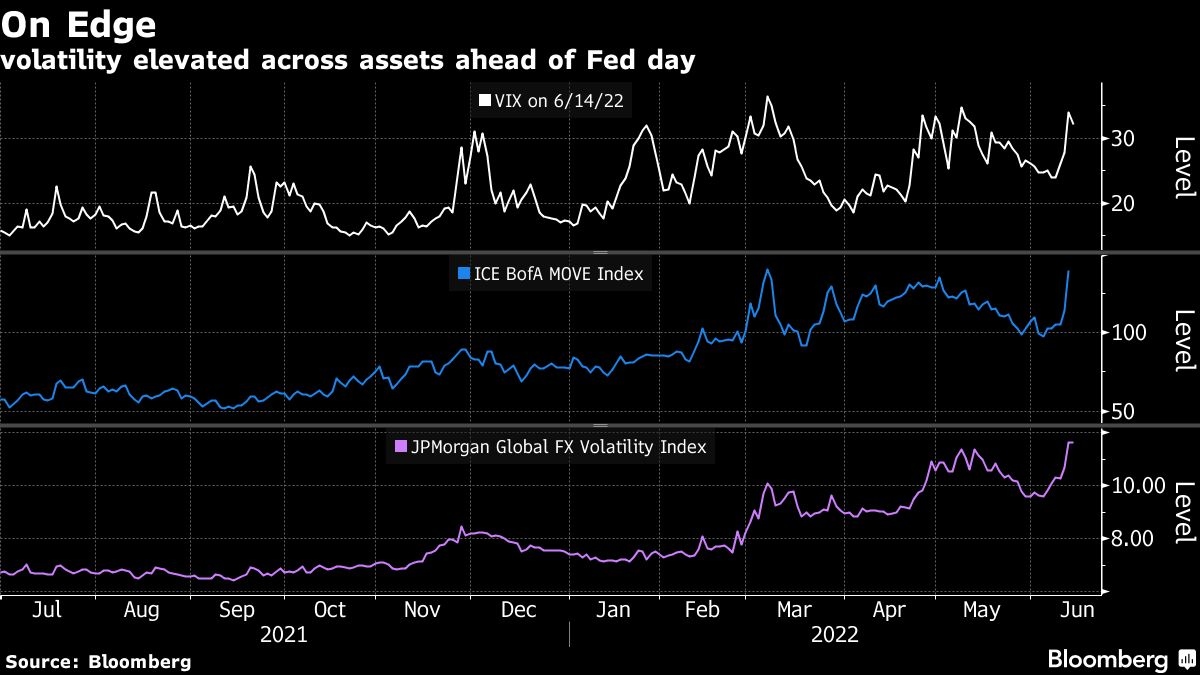

Hedge funds have been similarly expeditious, selling equities at the fastest rate on record over two days through Monday, according to Goldman Sachs Group Inc. prime brokerage data. They’re pulling out as implied volatility across assets sits at levels not seen for any pre-Fed session in more than a decade.

All of it is testament to swelling uncertainty headed into Wednesday’s Fed meeting, where anything from a half-point to a full-point increase in the federal funds rate is forecast. Stock prices have been flattened in the rush to the exit, with the S&P 500 heading for the worst month since the pandemic selloff in 2020. Bond turmoil is everywhere, with two-year Treasury yields spiking to the highest level since 2007.

“We’re sitting at the bottom and there’s plenty of dry powder, but everybody’s fleeing to cash because they’re afraid of runaway inflation,” Benjamin Dunn, president of Alpha Theory Advisors, said by phone. “There’s doomsayers out there saying that policy makers cannot engineer what they need to do to bring down prices without completely breaking the bond market.”

Anxiety is on vivid display. In the note published Tuesday, Goldman said short sales at its hedge-fund clients climbed “aggressively” over the previous two sessions, with broad-based investing strategies -- or macro products -- like exchange-traded funds dominating the flows. A gauge of their risk appetite that takes into account both bullish and bearish bets -- known as gross leverage -- sat near five-year lows, the data show.

It’s not hard to see why sentiment is deteriorating. All year, any attempt to buy the dip -- a strategy that had worked for a decade -- has been met with fresh lows in the market. Having fallen more than 20 per cent from its January peak amid concern the Fed’s efforts to subdue inflation will cause a recession, the S&P 500 this week entered a bear market for the second time since 2020.

On Monday, when losses spread across major assets, trend-following Commodity Trading Advisors -- which make long and short bets in the futures market -- sold about US$11 billion of bonds and US$21 billion of stocks, according to an estimate by Charlie McElligott, a cross-asset strategist at Nomura Holdings. Meanwhile, volatility target funds, such as risk parity, slashed holdings cross credit and bonds.

The risk aversion has been so intense that the equity exposure among these groups has fallen to the 2nd percentile of the historic range, data compiled by Deutsche Bank show.

“For systematic strategies it is purely a function of how the market is behaving, specifically the sharp rise in volatility,” said Parag Thatte, a strategist at Deutsche Bank. “For discretionary investors, whose positioning is aligned with slowing growth but not a recession, we think positioning will come down as more of them position for recession.”

Increasingly, angst is building that the Fed will have to raise rates more aggressively to tame the hottest inflation in four decades at the risk of causing an economic recession. The two-year and 10-year yield curve inverted briefly this week, signaling concerns that restrictive monetary policy may take a bigger toll on the economy.

“We’re going to tend to be short in a rising rate environment particularly when we get to close to inversion type of point where we’re moving into a more recessionary environment,” Katy Kaminski, AlphaSimplex’s chief research strategist, said in an interview on Bloomberg TV. “During those environments, our strategy will tend to be 70 per cent short bonds. If we move into that environment, we will see more short bond signals over the next few years.”