James Bullard’s inflation epiphany came when he tried to buy a bicycle.

It was March 2021, and the Federal Reserve Bank of St. Louis president couldn’t find the model he wanted in the local store, which was 90 per cent empty. So he ordered online -- only to be asked, when the bike was delivered four months later, for an inflation surcharge of around U.S.$200. He refused to pay, but came away distressed.

“The idea that you’re changing prices in the middle of some transaction was alarming to me,” Bullard recalled in an interview last month. “It was very telling about the environment.”

That environment, it turned out, was the initial phase of the worst wave of inflation to hit the U.S. in four decades. Bullard has been in the vanguard of the Fed’s campaign to crush it with high interest rates.

Way back when Chair Jerome Powell was still describing pandemic inflation as “transitory,” the St. Louis Fed chief was already raising red flags. He would become the first policy maker to urge hikes of a half-point or more, and the first to publicly discuss the idea of 75 basis-point increases. He’s repeatedly urged “front-loading” of monetary tightening.

‘A LITTLE PREMATURE’

Since the Fed ended up doing all of those things, Bullard’s prescience has made him a favorite policymaker for Wall Street to follow.

“He’s very non-consensus,” says Simona Mocuta, chief economist at State Street Global Advisors in Boston. “Concepts he has introduced -- novel concepts -- have ultimately become more mainstream.”

Right now, amid growing concern that tight money will trigger recessions in the US and beyond, the question at the top of Wall Street’s collective mind is: When will the Fed ease up? It’s natural that investors should turn to Bullard for an answer.

“The markets look to him as a secondary proxy to the chairman,” says Lindsey Piegza, chief economist at Stifel Nicolaus & Co. in Chicago. “When he adopts a softer tone, that could be an indication the committee is taking that view.”

Bullard says that’s unlikely to be anytime soon.

“It’s a little premature to say when we can declare victory,” he says. “The near- and medium-term goal is get moving in the right direction,” toward the Fed’s 2 per cent inflation goal.

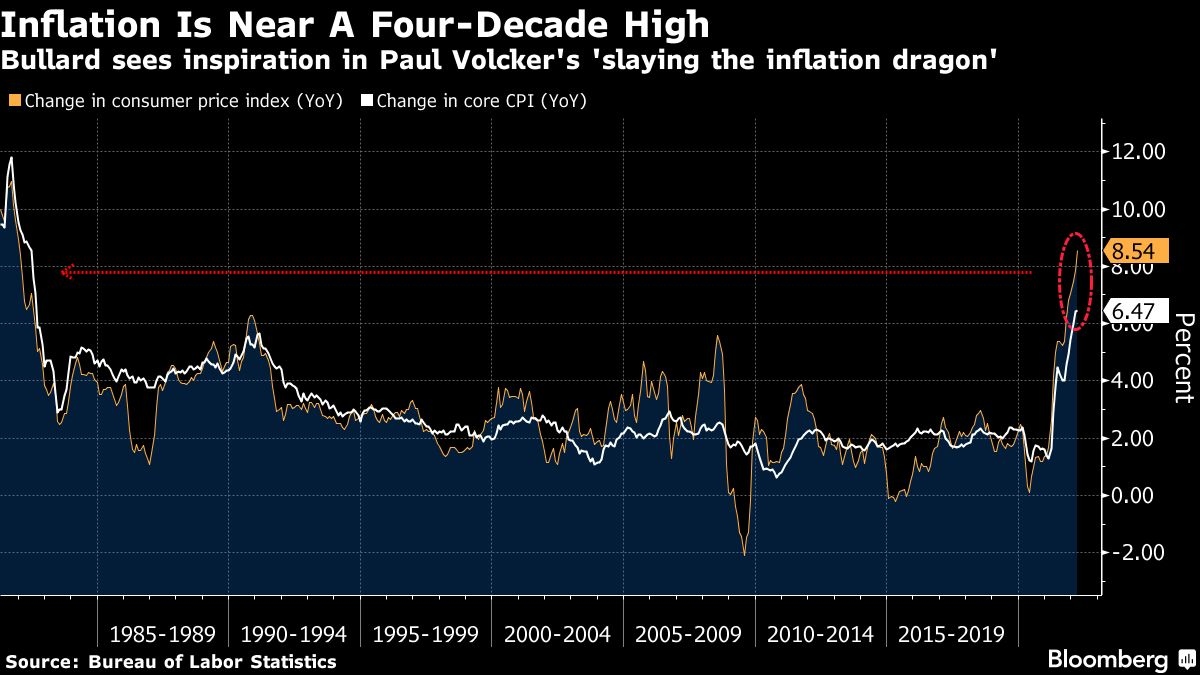

SLAYING THE DRAGON

U.S. consumer prices have been rising at more than triple that pace throughout 2022, driven by a combination of bottlenecks and stimulus-led demand from the pandemic, and made worse by a commodity squeeze after Russia invaded Ukraine.

Some economists argue that a lot of those price pressures will dissipate anyway as supply-chain problems ease –- and that Bullard and his colleagues are inflicting unnecessary pain on the economy by raising rates so fast.

“He at least has been prepared to give a different view, which is good, and the least subject to groupthink,” says David Blanchflower, a former Bank of England policymaker who’s now a professor at Dartmouth College. “I disagree, and am concerned that nobody represents the dovish view any more.”

The last time the U.S. suffered from persistently high inflation was in the late 1970s and early 1980s, when Bullard started studying economics.

A native of Forest Lake, Minnesota, he’d been a basketball player at high school -- a 5-foot-8-inch guard playing pickup games with fellow Minnesotan Kevin McHale, who went on to become a Boston Celtics star. Bullard dropped the sport when he went to study economics at St. Cloud State University.

He was struck at the time both by the economic turmoil around him –- the long lines at gas stations –- and by the high-stakes attempt of the Fed, under Paul Volcker, to fix it by ratcheting interest rates up to around 20 per cent.

Bullard recalls a giant poster on the wall at St. Cloud’s economics department that was supposed to illustrate the causes of inflation. Government spending was there, and so were labor unions –- but the Fed wasn’t. There was no consensus that the central bank was at least partly to blame, until “Volcker slayed the inflation dragon,” Bullard says.

'REPEAT,REPEAT,REPEAT'

In his time at the St. Louis Fed -- he joined the research department there after earning his Ph.D. in 1990, and was named president in 2008 -– Bullard has earned a reputation as something of a maverick.

He has little time for the idea, widely accepted at the Fed, that there’s a close relationship between unemployment rising and inflation falling – calling it an argument that “doesn’t make sense.”

His own preferred theory for how to keep prices in check highlights the importance of competition. “It has to come through the businesses themselves, the price-setters in the economy,” he says. “They have to have the fear of God in them that if they raise their prices too much, they’re going to lose market share.”

Bullard tends to hammer home his arguments by repeating them over and over, delivering identical talking points both in Federal Open Market Committee meetings and in his frequent public speeches and interviews. It’s a deliberate strategy, according to David Andolfatto, an economist who recently left the bank to head the University of Miami’s economics department.

“David, you can never just say something once,” Andolfatto cites Bullard as telling him. “Repeat, repeat, repeat. People can’t absorb immediately.”

Bullard took over as president in April 2008, with financial crisis looming. On his first day, he got a call from then-Chair Ben Bernanke which he expected to be “kind of a pep talk” – but instead turned into a detailed discussion about the recent bailout of Bear Stearns.

The St. Louis Fed’s new chief soon became a leading dove. He published a paper titled “Seven Faces of the Peril,” urging the Fed to buy more Treasuries as a way to prevent deflation -- which it subsequently did in a second round of quantitative easing.

'ASK JIM'

It’s a role he repeated in 2020, backing aggressive Fed easing to cushion unemployment that soared to near 15 per cent after Covid hit.

By January 2021, Bullard was issuing tentative warnings about inflation, even though the headline rate was still only 1.4 per cent. With vaccinations being rolled out, and unprecedented fiscal stimulus, he saw price pressures building -- and worried that monetary policy wasn’t well positioned to deal with them.

Now, with Fed policy already restricting economic growth -- and officials promising plenty more hikes to come -- the shift to hawkish mode is complete, and markets are wondering about the next pivot.

“At some point you can make further judgments about whether you think you’ve done enough, and make further adjustments from that,” Bullard said. His own stance would change if he thinks the Fed isn’t giving enough weight to downside risks for the economy, as opposed to the threat of inflation.

Bullard has a reputation for being early with policy calls. It may happen again, according to James McKelvey, chair of the St. Louis Fed board of directors.

“He has a stellar record of predicting what is going to happen,” said McKelvey, a serial entrepreneur who co-founded mobile-payments service Square. “If you want to know what is going to happen tomorrow, you ask Jim today.”

Advertisement