Feb 28, 2023

Cash pays more than 60/40 portfolios for first time since 2001

, Bloomberg News

It's becoming a stock picker's market, here's what to buy: Michele Schneider

VIDEO SIGN OUT

For the first time in more than two decades, some of the world’s most risk-free securities are delivering bigger payouts than a 60/40 portfolio of stocks and bonds.

The yield on six-month U.S. Treasury bills rose as high as 5.14 per cent Tuesday, the most since 2007. That pushed it above the 5.06 per cent yield on the classic mix of US equities and fixed-income securities for the first time since 2001, based on the weighted average earnings yield of the S&P 500 Index and the Bloomberg USAgg Index of bonds.

The shift underscores how much the Federal Reserve’s most aggressive monetary tightening since the 1980s has upended the investing world by steadily driving up the “risk-free” interest rates — such as those on short-term Treasuries — that are used as a baseline in world financial markets.

The steep jump in those payouts has reduced the incentive for investors to take risks, marking a break from the post-financial crisis era when persistently low interest rates drove investors into increasingly speculative investments to generate bigger returns. Such short-term securities are typically referred to as holding cash in investing parlance.

“After a 15-year period often defined by the intense cost of holding cash and not participating in markets, hawkish policy is rewarding caution,” Morgan Stanley strategists led by Andrew Sheets said in a note to clients.

The yield on six-month bills rose above five per cent on Feb. 14, making it the first U.S. government obligation to reach that threshold in 16 years. That yield is slightly higher than those on 4-month and one-year bills, reflecting the risk of a political skirmish over the federal debt limit when it comes due.

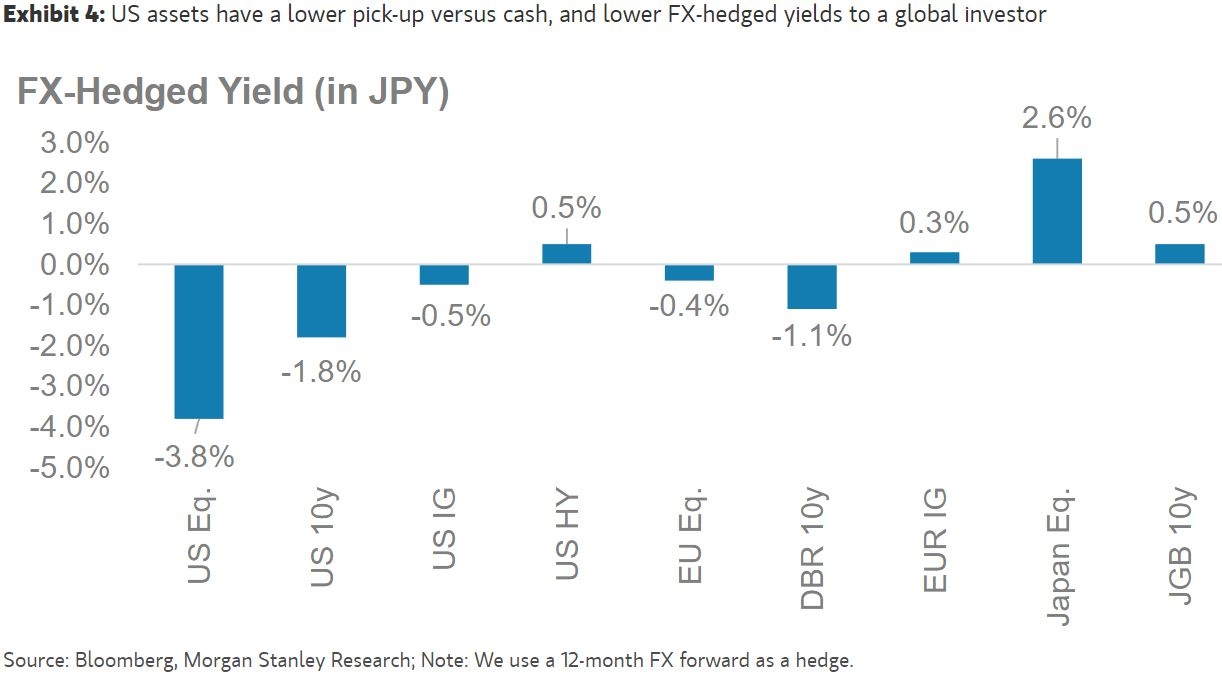

The high rates on short-term Treasuries are casting broad ripples in financial markets, according to Sheets. It has reduced the incentive for typical investors to take on more risk and driven up the cost for those who use leverage — or borrowed money — to boost returns. He said it has also cut the currency-hedged yields for foreign investors and made it more expensive to use options to bet on higher stocks.

Investing in stocks and bonds has also been challenging recently. After a strong start to the year, the 60/40 portfolio has given up most of its gains since a string of strong economic and inflation data prompted investors to bet on a higher peak to the Fed’s policy rate. That sparked a simultaneous selloff in stocks and bonds this month. The 60/40 strategy has returned 2.7 per cent this year, after tumbling 17 per cent in 2022 in its biggest decline since 2008, according to Bloomberg’s index.

Photographer: Chris McGrath/Getty Images Europe, Photographer: Chris McGrath/Getty Images Europe")