Feb 7, 2019

Chipotle jumps as analysts cheer traffic turnaround, more sales

, Bloomberg News

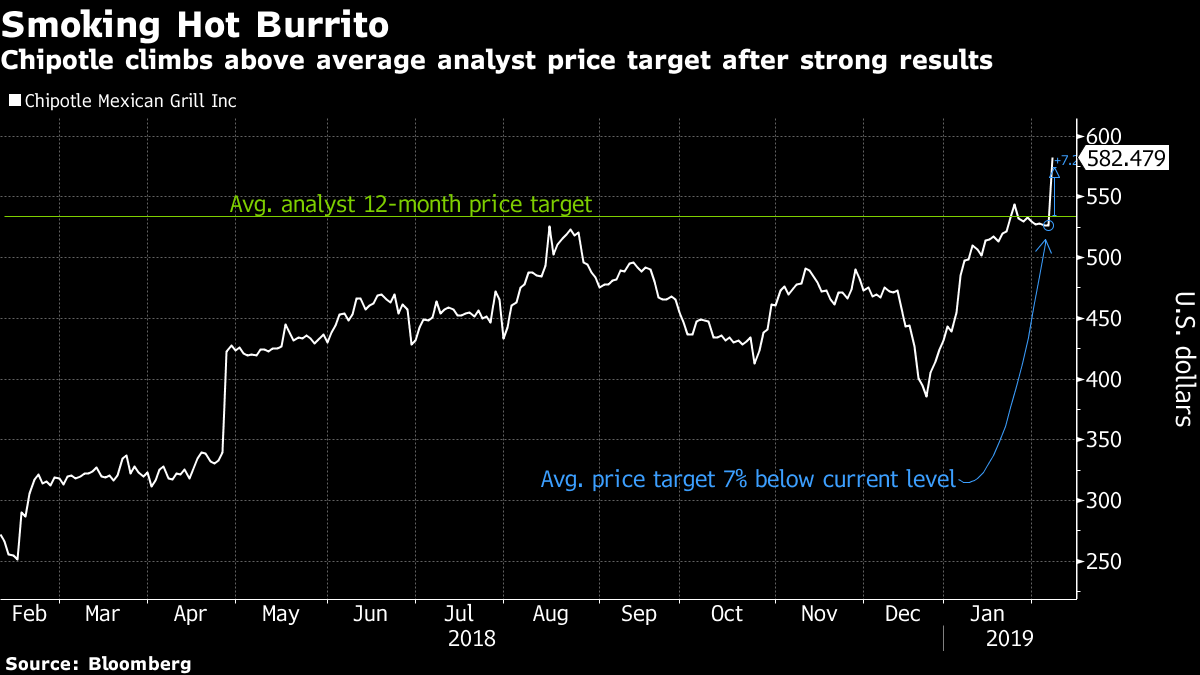

Chipotle Mexican Grill Inc. (CMG.N) soared to the highest in more than three years on Thursday after the chain handily beat earnings, sales, and margin expectations in the fourth quarter as traffic turned positive, rising 2 per cent.

Efforts to boost the business have paid off through the use of expanded delivery, digital capabilities and a new loyalty program that have reclaimed customers after a series of food-borne illness scares. In the past 12 months, Chipotle shares have climbed 117 per cent.

But even with the improved results, analysts stuck to their ratings, providing commentary that supported their existing buy, hold, or sell positions. But the average 12-month price target for Chipotle has increased to US$534 per share from US$494 just a week ago, according to Bloomberg data.

Here’s what Wall Street analysts have to say:

Bernstein, Sara Senatore

“Positive traffic is especially encouraging as is 2019 mid-single digit comp. guidance, suggesting strength has continued QTD.”

“The 210 bps margin expansion reflects price and sales leverage but also greater in store efficiencies; we see further margin expansion ahead, undergirding strong unit economics and a long growth runway.”

Rates outperform, price target to US$650 (matches Street high), from US$560

Morgan Stanley, John Glass

“4Q results showed a meaningful positive trend change in sales, especially later in the quarter, with carry-through to 2019 and more initiatives still either in early stages or to come.”

“This quarter validates the thesis that the economic model has the potential to substantially recapture former average unit volumes and margins.” The bull case, which centers on high-single digit comparable sales in 2019/2020, with approximate 23 per cent restaurant margins and EPS more than US$20 by 2020, “ is still in play” with fourth quarter results “supporting, not detracting, from that case.”

Rates overweight, while acknowledging that CMG is an expensive stock and “a lot still has to go right to achieve this bull case.” Price target to US$617 from US$600.

SunTrust Robinson Humphrey, Jake Bartlett

“4Q results give us greater confidence in both CMG’s SSS recovery (+6.1 per cent vs our consensus-matching +4.5 per cent est.) and the flow through to margins.”

“With the exception of menu price, we expect the drivers of 4Q18 SSS to build in ’19, including new marketing, digital sales and operations (throughput), potentially driving upside” to the initial mid-single digit same-store sales growth forecast.

Chipotle is in the “early stages of its sales recovery.” Rates buy, price target to US$635 from US$595

Telsey Advisory, Bob Derrington

“Shares are likely to continue to drift higher (for now) supported by its better than expected operating momentum.”

“While we are encouraged by the considerable improvements management continues to make within its core fundamentals and CEO Niccol and his team continue to prep the company for even stronger trends to come, it’s hard to justify chasing an incremental investment in CMG shares here.”

Rates market perform, PT US$600 from US$500

Goldman, Karen Holthouse

“We were somewhat surprised by the strength of CMG shares after the close despite a strong earnings beat in the quarter ($1.72 versus Consensus Metrix of $1.37) when near-term commentary did little to confirm fairly bullish 1Q19 investor expectations.”

“2019 cost commentary actually brought our already below consensus EPS estimate down despite a higher top-line, and still very qualitative versus quantitative commentary on various initiatives did little to firm an out-year valuation based bull case.”

Holthouse noted that flow-through on delivery is “a key differentiator to the story.” Commentary that CMG is consistently one of the fastest deliveries for their third party vendor may mean “lower costs for the vendor, and, over time, could put CMG in a position to argue for reduced delivery commissions as a result.”

Rates neutral , price target US$473

Raymond James, Brian Vaccaro

“While we have increased confidence in the company’s underlying fundamentals, (as reflected in our raised comp/ EPS estimates), we believe very high expectations are reflected in the stock’s elevated valuation metrics (2020 P/E nearing 40x), leaving little room for error.”

Rates market perform

--With assistance from Gregory Calderone.