Jun 3, 2021

Crypto-crash aftershocks hit traders with 50% premiums vanishing

, Bloomberg News

Over 80% of AMC shareholders are retail investors: AMC analyst

VIDEO SIGN OUT

Speculative investors may have been pushing meme stocks “to the moon” earlier this week, but their crypto counterparts have been coming back down to Earth en masse.

Hedging activity is on the rise and bullish bets are finding limited demand -- even with Bitcoin still almost 40 per cent below its peak. These are rare times of restraint among day traders, who until last month’s US$500 billion crash were famously in the throes of bullish mania.

Another way of looking at it: A slew of market excesses fueled by leverage are getting snuffed out.

“Price and narrative are the fundamentals in cryptocurrency markets -- right now, both are shaken,” said Nico Cordeiro, chief investment officer at Strix Leviathan, a digital-asset investment firm.

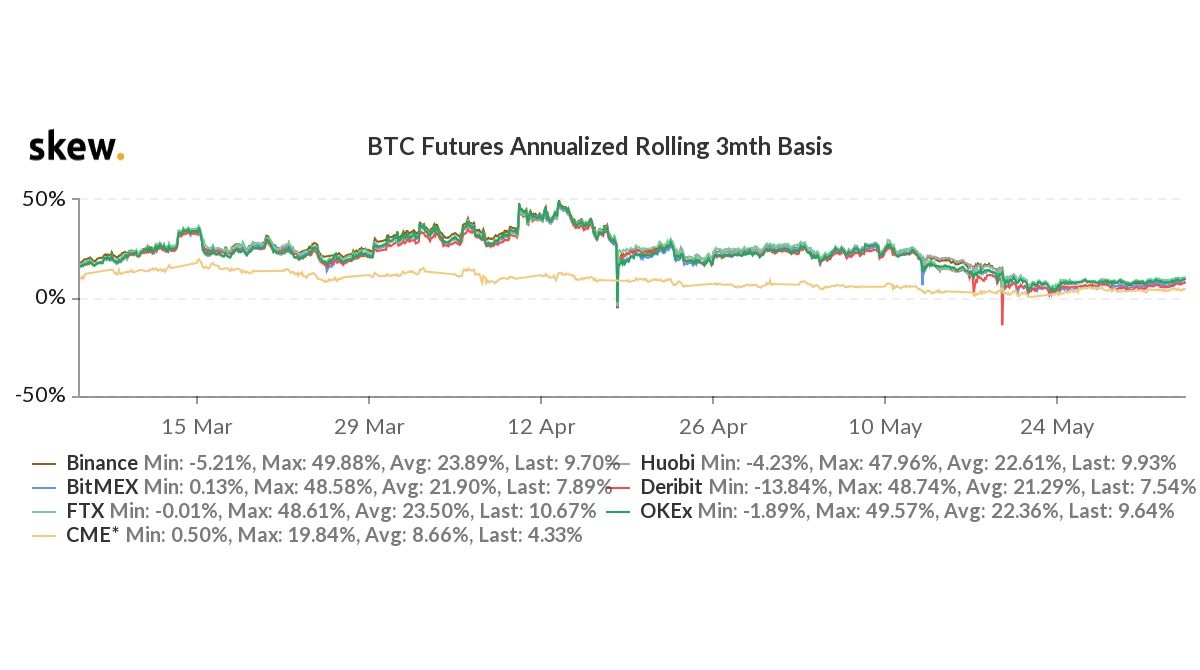

Take the gap between Bitcoin futures market and the spot price. At the height of the mania in April, the premium shot to 50 per cent on an annualized basis -- meaning investors could lock in a massive profit with a simple convergence trade.

It’s now collapsed to just 9 per cent, according to data provider Skew, which tracked rolling three-month contracts on crypto exchange Binance.

Volume in derivatives typically exceeds spot activity on most days, on strong demand to speculate with easy-to-trade instruments that offer leverage -- often 100 times -- to boot. All that means bulls almost always outnumber bears.

Now, crypto conviction is falling. Support from Bitcoin’s star promoter Elon Musk has wavered and there are new regulatory hurdles in China and the U.S. For the past two weeks, prices have wobbled around US$40,000, unable to move much in either direction.

Retail demand for long positions across the curve is vanishing. The futures-spot spread is narrowing on BitMEX and other crypto platforms to bring it closer to the level on the Chicago Mercantile Exchange, an institutionally oriented platform.

It all signals harder times for quants like BKCoin Capital who have notched outsize gains with simple arbitrage strategies that involve going short futures and long the spot.

“In mature, liquid markets, institutional and sophisticated investors search for various arb opportunities,” said Kelly Pettersen, head of business development at Skew, now acquired by Coinbase Global Inc. “Applying this same strategy in crypto, over time, means the market and the trade will continue to get more popular, and the spread will narrow.”

Demand to go long is also falling in a typically lucrative trade known as perpetual futures.

The uniquely crypto derivative has no expiry date and is kept in line with the spot price thanks to incentives created by a funding rate. When sentiment was rosy, the charge got as high as 0.3 per cent on the BitMEX platform -- meaning bulls were willing to pay up to hold onto a Bitcoin bet for just hours.

But over the past two weeks, the rate has been sitting at zero or in negative territory.

Hedging demand

While traders in the stock market primarily use options for hedging, investors in crypto assets have long preferred to buy them as a way to bet on further gains. For that reason, outstanding calls have always exceeded puts in crypto markets, Skew figures show.

Open-interest data show that’s still true. Yet over the past month the cost of one-month puts on Bitcoin has risen above the price of comparable calls -- a sign of rising demand to hedge.

That suggests crypto options are looking more like equities where defensive contracts have long commanded a premium over bullish counterparts.

The upshot? Caution is building across a Bitcoin ecosystem acutely prone to speculative extremes.

, Photographer: Scott Olson/Getty Images North America")

used to mine the Ethereum and Zilliqa cryptocurrencies at the Evobits crypto farm in Cluj-Napoca, Romania, on Wednesday, Jan. 22, 2021. The world’s second-most-valuable cryptocurrency, Ethereum, rallied 75% this year, outpacing its larger rival Bitcoin. Photographer: Akos Stiller/Bloomberg, Bloomberg")