The European Central Bank unexpectedly accelerated its wind-down of monetary stimulus, signaling it’s more concerned about record inflation than weaker economic growth as Russia’s invasion of Ukraine threatens to propel prices even higher.

Calling the war a “watershed” moment for Europe, ECB officials pledged to slow bond buying from the start of May, and said they could halt the program as soon as the third quarter. They tried to temper that by making a subsequent interest-rate hike less automatic.

“The Governing Council sees it as increasingly likely that inflation will stabilize at its 2 per cent target over the medium term,” President Christine Lagarde, who wore a badge with the colors of the Ukrainian flag on her jacket, told reporters in Frankfurt. “The war in Ukraine is a substantial upside risk, especially to energy prices.”

The outcome defied the expectations of economists who anticipated a delay in major policy decisions to allow time to assess the implications of Russia’s attack. Some Governing Council members had also indicated that plans to end large-scale asset purchases and negative interest rates would probably be postponed.

The euro fell by 0.7 per cent on the day to US$1.0996. Italian bonds tumbled, sending the yield on 10-year securities up 24 basis points to 1.915 per cent.

Investors took the more rapid withdrawal of asset purchases as a sign that rate rises are nearing, with money markets now betting on a quarter-point increase in October, compared with December earlier. They see two more hikes in the first half of 2023, taking the key rate to 0.25 per cent.

While the Governing Council no longer suggests interest rates could go “lower” than at present, it also now says any hikes will be “gradual” and take place “some time after” bond purchases end rather than “shortly” after.

“Clearly ‘some time after’ is all-encompassing,” Lagarde said. “It can be the week after, but it can be months later. By that, I think we want to indicate that the time horizon is not what’s going to matter most. It’s the data that will support the decision.”

A hike this year would still leave the ECB behind some of its major peers in taking on inflation. The Bank of Canada raised rates last week and predicts its balance sheet will shrink quickly once it starts running off its bond holdings. At the Federal Reserve, liftoff is all but certain next week, when the Bank of England is widely expected to lift borrowing costs for a third straight meeting.

What Bloomberg Economics Says...

“On balance, Bloomberg Economics sees the outcome of the European Central Bank’s meeting as hawkish. At its first gathering since Russia invaded Ukraine, the Governing Council accelerated the wind down of its asset purchases, but loosened the link between the end of bond buying and its first interest rate increase, creating a lot of flexibility around the timing of the first rate hike.”

-- David Powell, Maeva Cousin, euro-area economists.

Since Russia’s invasion two weeks ago, Lagarde and her colleagues have been racing to evaluate how badly the 19-nation bloc will be affected by sanctions, trade disruptions and, above all, surging energy costs.

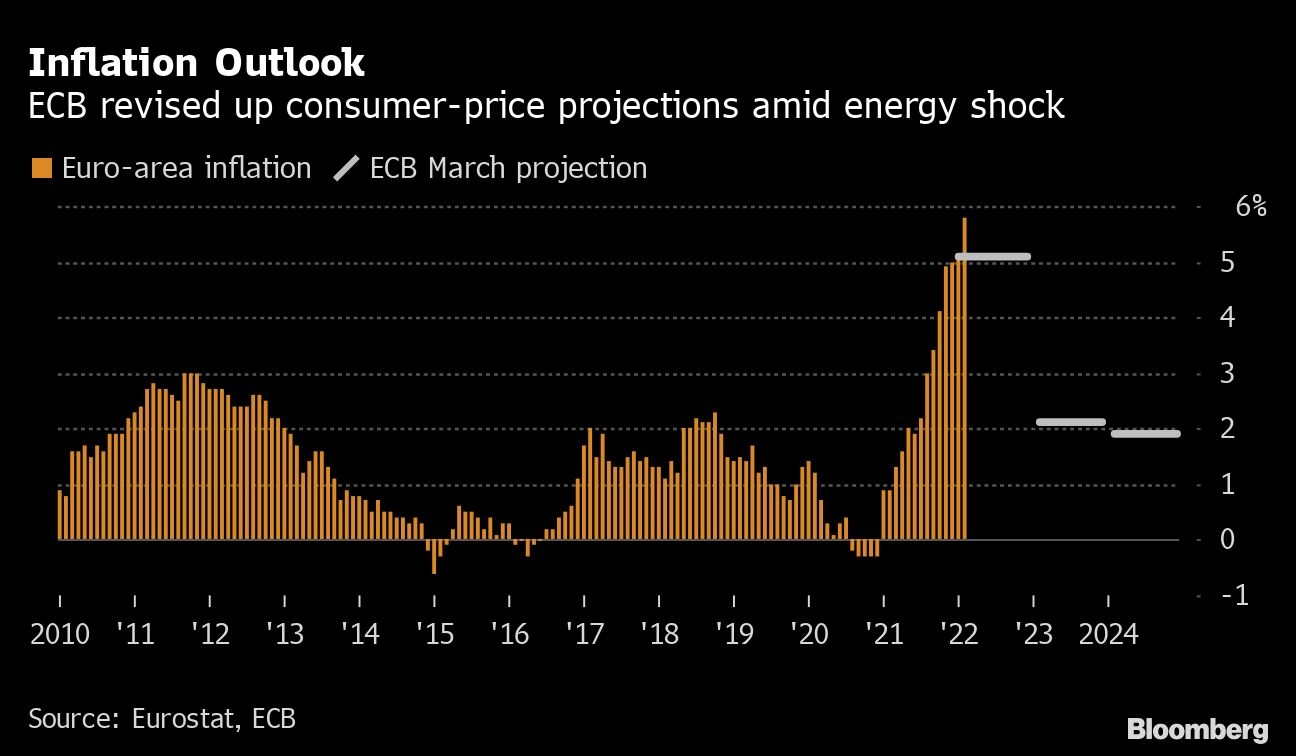

What looks certain is that the Kremlin’s assault and the resulting advance for oil and natural gas contracts will drive inflation further beyond the current 5.8 per cent record. That makes it harder to provide support while keeping prices from spinning out of control.

“The balancing act faced by the ECB is an extremely challenging one,” Paul Craig, portfolio manager at Quilter Investors, said in a statement. Faced with an inflationary shock that requires “quick and decisive action” as well as the threat of recession due to Russia’s invasion, the “ECB has opted for the path of least resistance.”

Given the surge in energy prices, the ECB unveiled new forecasts that raised the inflation outlook for this year to 5.1 per cent from 3.2 per cent. The average for 2024 will be 1.9 per cent, Lagarde said, just under the ECB’s target.

While the ECB cut its outlook for growth for this year and next, its forecast still showed healthy momentum. By contrast, Goldman Sachs on Thursday said economic output will shrink in the second quarter, with inflation likely to climb toward 8 per cent. Former ECB official Otmar Issing warned that a repeat of 1970s stagflation is “the biggest risk” facing the currency bloc.

The wind-down in stimulus will start in May, when the ECB will slow bond buying to 30 billion euros (US$33 billion), followed by 20 billion euros in June.

“We’re not talking about accelerating, we’re not talking about tightening, we’re talking about normalizing,” Lagarde said, referring to the pace of debt-buying. “The support that net asset purchases can give to policy rates is getting close to a conclusion and therefore requires that we decelerate the pace of purchases.”

Lagarde said that policy makers differed on what to do at Thursday’s decision.

“There were some members who said that given uncertainty we have we should be uncertain as well and do nothing,” she said.

Advertisement