Sep 3, 2019

For Bank of Canada, the trade war is getting harder to ignore

, Bloomberg News

Bank of Canada prepares to break silence

VIDEO SIGN OUT

The Bank of Canada is expected to open the door further to interest rate cuts at a decision Wednesday, amid worries U.S.-China tensions will curb a relatively robust expansion at home.

In a policy statement due at 10 a.m. that’s likely to keep benchmark rates unchanged at 1.75 per cent for now, economists expect Governor Stephen Poloz will underline his unease with the global trade outlook and signal a greater willingness to join the Federal Reserve and other central banks in cutting borrowing costs, as early as next month.

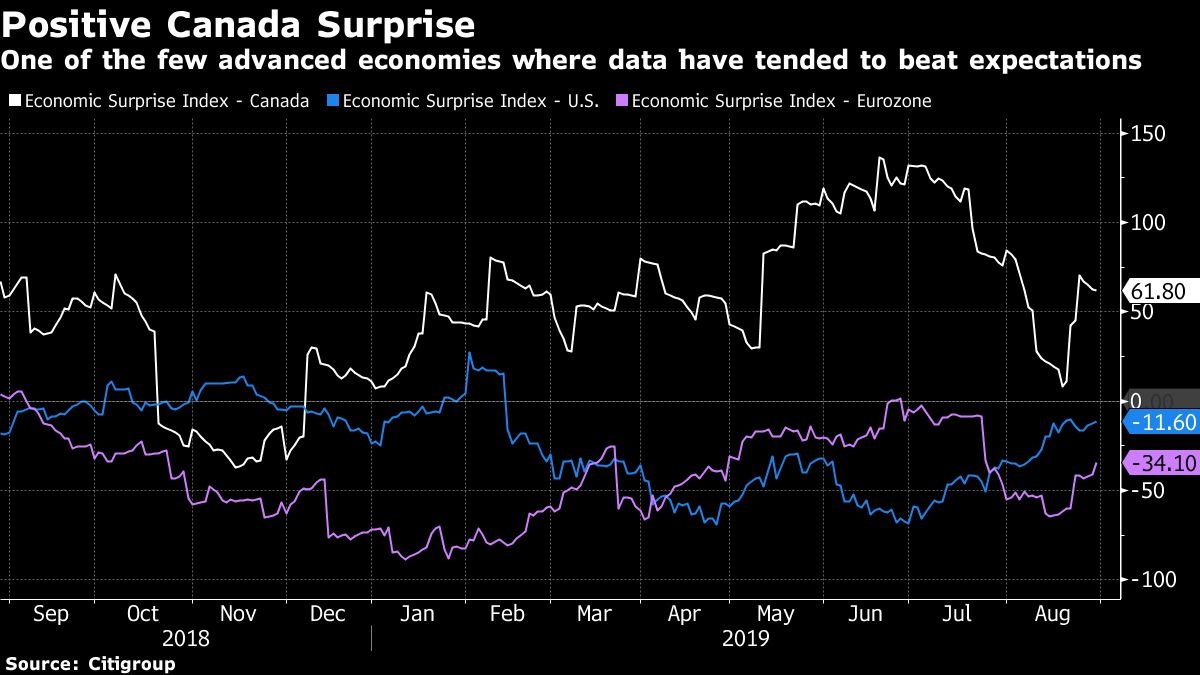

The case for cheaper money isn’t as compelling in Canada as it is elsewhere. A strong run of economic data affords policy makers opportunity to resist -- as they have so far -- the dovish turn in global policy. But escalating tensions between China and the U.S., and their spillover into Canada, are getting tougher to overlook, particularly given how they’ve already become a major reason behind global factory weakness.

“The truth of the matter is, if you go back really over the last month and a half, the domestic picture hasn’t changed in Canada,” said Mark Chandler, head of fixed-income research at Royal Bank of Canada, who sees a rate cut in January. “Trade risks have increased but we really don’t know at this stage to what degree they’ve altered the outlook for the bank.”

Complicating matters is that the Bank of Canada hasn’t made any public comments since its last rate decision on July 10. Wednesday’s decision is a statement-only affair. The next day, Deputy Governor Lawrence Schembri will give a speech in Halifax to provide more details on the central bank’s deliberations around the decision.

- Short the loonie before Bank of Canada policy shifts: Goldman

- B-20 stress tests don't need to be tweaked for 'shrewd' Canadians: Scotia CEO

- Bank of Canada rate cut coming in October amid trade woes: BMO

RELATED

Swaps trading suggests investors are fully pricing in a cut by December, with strong odds of a second by this time next year. Odds for a rate cut on Wednesday are less than 10 per cent.

Even two cuts over the next 12 months would still leave Canada with the highest policy rate among advanced economies -- raising the question of whether the domestic outlook truly justifies the northern nation’s outlier status.

While Canada’s expansion is hardly remarkable, it stands out by virtue of having largely weathered the recent global slowdown. After a sluggish start to the year, growth in Canada accelerated to a strong 3.7 per cent annualized pace in the second quarter, giving it a very decent 2.1 per cent performance for the first half.

Canada’s housing market, meanwhile, is recovering; inflation is at target; and wage gains are accelerating. The Canadian data are hardly screaming rate cut.

Nor are forecasts overly gloomy.

Economists, including those at the central bank, continue to see growth averaging more than 1.5 per cent in the foreseeable future, which outside of the U.S. is as good as it gets in the Group of Seven.

Of course, the Bank of Canada could mark down its forecasts for exports and investment, and the second-quarter GDP numbers also raised concerns about the underlying strength of consumption. But without a global recession, the base case will continue to call for half-decent growth, tempering the need for rate cuts.

Risk Management

Yet, the one thing Poloz has practiced as governor is a reluctance to put too much weight on base case projections. He adopted a risk management framework in 2013 -- well before Fed Chairman Jerome Powell -- that essentially moved the focus away from pinpoint forecasts to thinking about what could produce unexpected deviations. It’s a play-it-safe strategy.

When conditions were calling for rates to go up, risk management took the form of hyper data dependency. Policy makers were worried that more expensive credit could trigger an unwanted downturn so they were willing to go slow with hikes, waiting for the data to reaffirm their analysis.

Now, with downside risks at the forefront and conditions suggesting cuts are in order, waiting may no longer be the best type of risk management strategy. Which is why Poloz, in the middle of the oil price shock in 2015, cut interest rates at the time. He called it an insurance cut, much like Powell’s rationale for the Fed’s last move.