Honeywell International Inc.’s aerospace and energy businesses continue to struggle with fallout from the pandemic, outweighing surging demand for warehouse automation and healthier buildings. The shares fell.

Honeywell’s two largest businesses are “trending toward the low end” of its 2021 forecast, according to an earnings presentation. Oil and gas companies have delayed investment projects and airlines still are flying less than they did before COVID-19 crushed global travel.

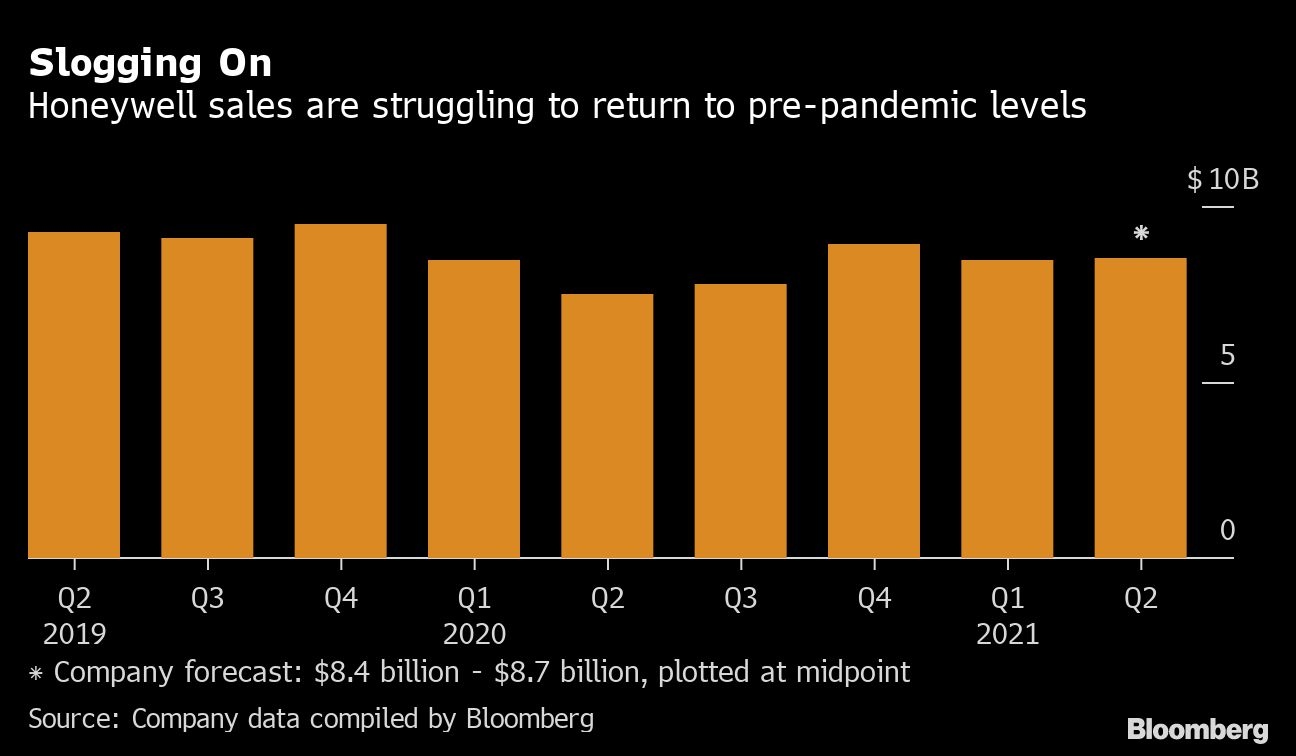

Still, overall organic sales, which strip out the impact of acquisitions and currency fluctuations, are likely to rise as much as 5 per cent this year, the company said in a statement Friday. That’s a percentage point higher than the company’s January forecast. First-quarter results topped analysts’ estimates.

“We are seeing promising signs of a rapid recovery in some of our markets,” Chief Executive Officer Darius Adamczyk said in the statement.

The stock fell 2.6 per cent to US$223.32 at 9:46 a.m. in New York. The shares had climbed 7.8 per cent this year through Thursday, while the Dow Jones Industrial Average advanced 10 per cent.

Honeywell has slashed costs during the pandemic and jumped on opportunities like churning out more N95 masks, attempting to ride out tumbling demand from energy and aerospace customers. The company expects enough of a rebound in those two industries, plus demand for warehouse equipment driven by e-commerce, to boost results for the whole year.

Sales plummeted 22 per cent at the aerospace unit and dropped 2.1 per cent for Honeywell’s performance-materials and technologies division, which sells to energy companies. Revenue for the division that makes warehouse automation systems and personal protection gear jumped 49 per cent, though that’s a much smaller and lower-margin business.

Adjusted earnings dropped to US$1.92. Analysts had expected US$1.80, based on the average of estimates compiled by Bloomberg. Revenue was essentially flat at US$8.45 billion, while analysts had anticipated US$8.09 billion.

The Charlotte, North Carolina-based company raised the lower end of its full-year profit forecast to US$7.75 a share from US$7.60. The high end remains at US$8 a share.

Advertisement