As we approach seeing the results of the second-quarter turmoil for global equity markets, the biggest impact could be seen from currency movements.

The U.S. dollar depreciated about 6.8 per cent in the quarter and about 11 per cent year to date compared to the trade-weighted dollar index.

But over the past decade, the U.S. dollar has been about five per cent stronger on average and about unchanged from end to end. For all the wrangling about trade deficits and being treated unfairly, the currency impact and discussion about dollar depreciation seems to be more noise than fact.

The U.S. dollar has mostly free floated versus the developed world in a relatively tight range and over the period is close to where it was when gold lost its peg as the Bretton Woods agreement was broken.

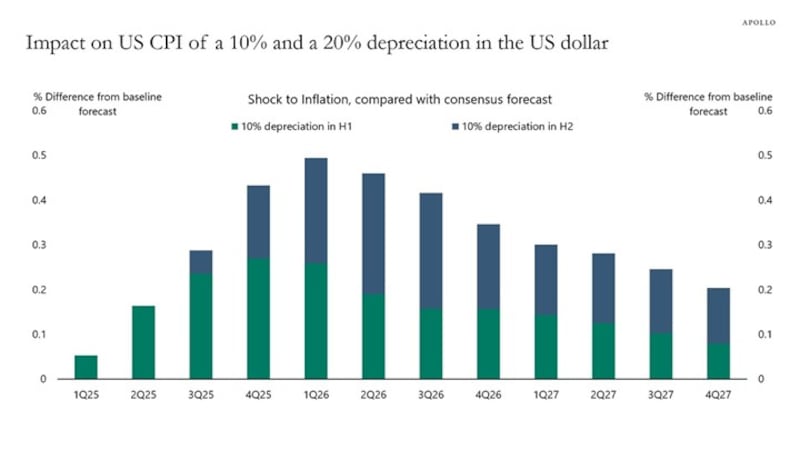

Periodic and sharp moves do impact trade, costs and inflation. It’s estimated that the recent 11 per cent move year to date could have a 0.3 per cent impact on increasing the U.S. consumer price index in the coming months, according to the model that Apollo’s chief economist Torsten Slok runs.

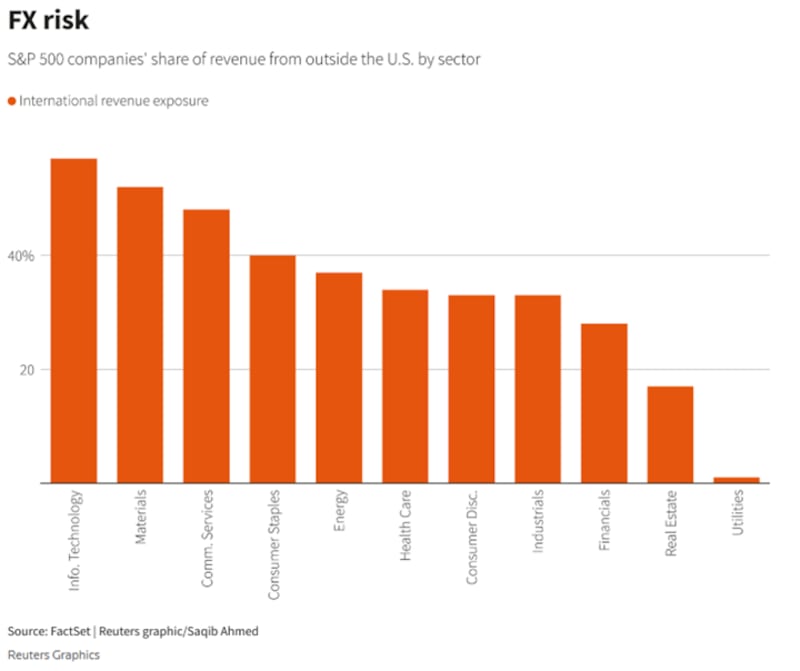

On the positive side, revenue earned by S&P 500 companies can add about three per cent of earnings on a 10 per cent move. This will be something to watch this earnings period to see how much impact companies are reporting.

Earnings expectations for the next year are expected to be about 6.5 per cent, which is possible if the tariff impact is negligible in a nominal five per cent U.S. gross domestic product scenario for the next year. Where things go bad is if the economy falters, as U.S. equity markets, after the recent move back to all-time highs, are priced for perfection.

Follow Larry

YouTube: LarryBermanOfficial

LinkedIn: LarryBerman