Ray Dalio has recently put out some research on the rise and fall of reserve currency status. What caught my eye is the current battle between China and the U.S. for leadership in 5G and technology in general and the recent narrative around the U.S. weakness.

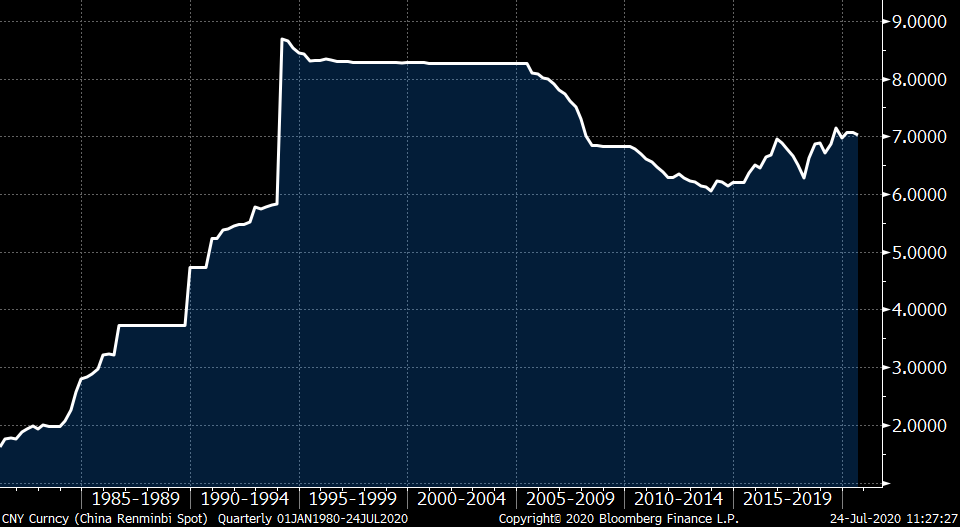

From the perspective of China, their currency is massively undervalued using the Big Mac Index, which equates the purchasing power of the famous burger adjusted for exchange rates. The U.S. dollar is far more balanced against Europe, Canada and most of the developed world on a purchasing power parity (PPP) basis.

Perspective is everything, though, and the narrative that the U.S. dollar is expensive may only be applicable from a trading perspective to China, South Korea and Japan.

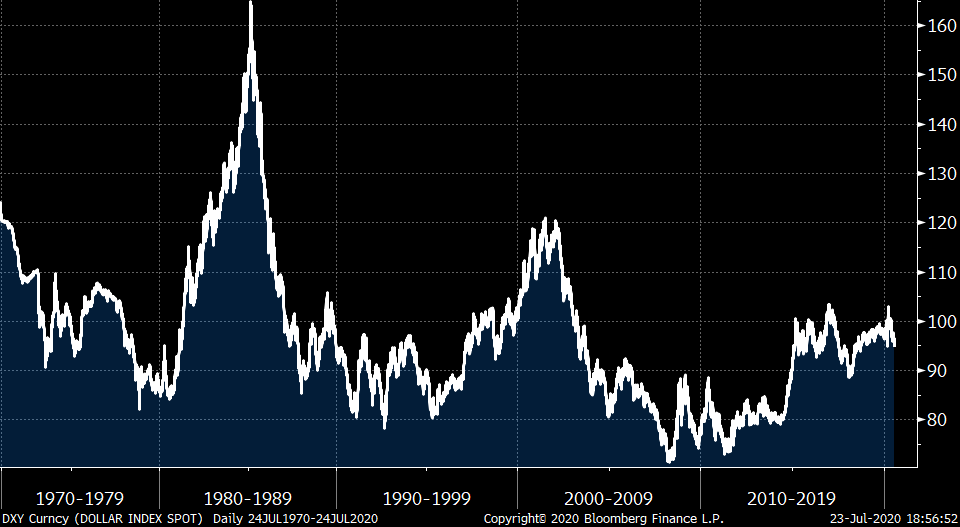

In 1985 the Plaza Accord was an agreed to by the G7 countries, finding that the greenback was too strong. A look at the long term chart of the U.S. dollar against its trading partners in the developed world really shows it is not at all expensive.

But now the benchmark is China.

When the euro was adopted in 1999, its value versus the dollar was about one per cent off from where it is today. On a PPP basis, there is no big imbalance there.

In the early 2000s, the tech bubble first attracted money to the U.S. market and then stayed there in U.S. Treasuries. Then the bubble broke. This was the last time the U.S. dollar was very strong in comparison to Europe’s currency. At the trough of the 2009 financial crisis, the U.S. dollar became very cheap to Europe. But, as growth troubles have hit Europe over the past decade, and shifted towards negative rates, the U.S. dollar has moved closer to the long term average.

Since the world came off the gold standard in 1971, the average U.S. dollar index has been at about the 100 level. We are currently less than five per cent from the 50-year average and have been there for several years.

The Canadian dollar, meanwhile, is currently caught up in the sentiment around the weak U.S. dollar, but it’s losing against the euro, yen, and British pound, and it should be weaker. I say that not so much on a PPP basis, but on weak fiscal positioning relative to the U.S. dollar. This suggests that it’s not a strong new view on Canada, but a flow that the loonie gets caught up in.

Dalio’s work also examines the rise and fall of global leadership, and finds that the battle with China is just beginning. China is the challenger for reserve currency status for the foreseeable future.

It’s certainly not Europe, though there is some excitement around common EU bonds now. How long will the German and Dutch tax-payers will supplement the Italian tax-payer? Not long—perhaps a few years, but the next stress to the region will almost certainly break the bond (so to speak). Unless of course, central banks are just going to print money and we are in the early phases of changing the way we think about the cost of money, interest rates and inflation. In which case, buy gold in whatever currency you can as they will all be devalued relative to gold.

For now, and until China fully opens its economy, we should see more of a de-globalization, where China gains more within their region of the world and takes on the status of a more localized reserve currency.

The big thing for the U.S. is to not damage ties to the euro bloc. If they start trading in yuan, the greenback’s reserve status is in trouble. These issues are measured in decades so it’s not something to trade off of or base any portfolio decisions on, but this is a major theme globally and likely has more of a negative impact on growth and inflation trends.

Follow Larry online:

Twitter: @LarryBermanETF

YouTube: Larry Berman Official

LinkedIn Group: ETF Capital Management

Facebook: ETF Capital Management

Web: www.etfcm.com

Advertisement