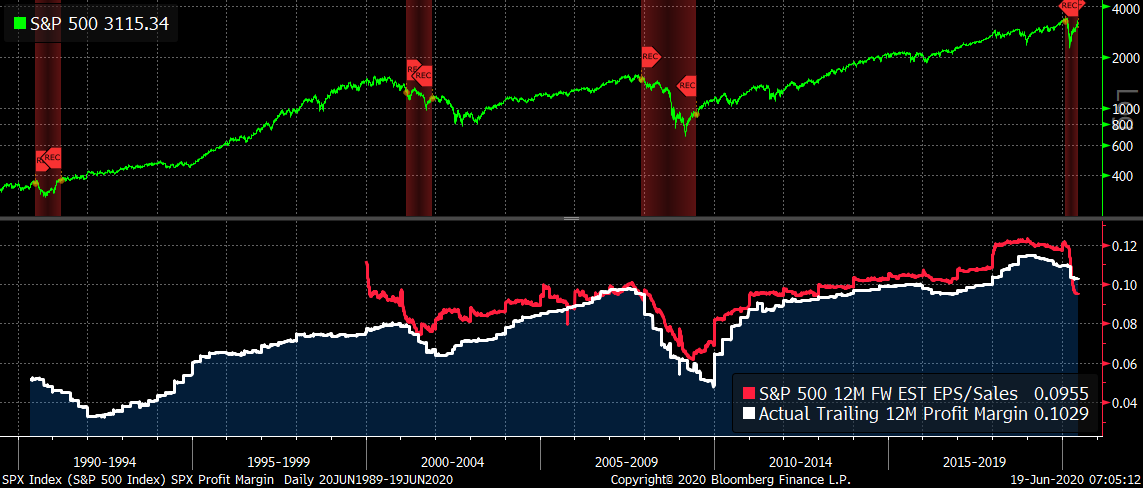

It’s important to understand what happens to profit margins in a recession. And make no mistake, we are very early in the recession that will most likely last well into 2021 in a best-case scenario. The hope for recovery based on record amounts of liquidity has merit, but it’s the very best-case scenario, not the most likely.

Make no mistake, should the Democrats control the White House in 2021, we will see U.S. President Donald Trump’s tax cuts unwound and profit margins will fall further. Margins are always stressed well through a recession. To think that the worst recession since the Great Depression will not have a negative impact is naïve, and to think it will only last a few months is naive.

The current market is priced for a Trump White House, more stimulus spending, and still-massive central bank money printing. Government largesse will continue, to be sure, but the bet is over how much that massive bridge-loan and accompanying speculation (at the cost of higher future taxes) will stack up against the real economy.

I get the “Don’t fight the Fed” mantra… historically, it has made sense. I’m not trying to fight the Fed. I try not to get caught up in the daily noise of the market and focus on big picture themes and trends.

But, we are now at a point where central bank money-printing is controlling free market price-discovery and that is telling me the system is fragile and failing. It’s not a reason to make big bets of be bullish about the economy or outlook. The markets can move higher, but it’s speculative in the face of major policy uncertainty, and not driven by fundamental value.

By several metrics, markets are ridiculously expensive. The Shiller CAPE (cyclically-adjusted P/E) tells me the forward-based returns for U.S. large caps over the next decade will be less than one per cent annualized after inflation, and that’s about as bad as it gets.

Here is a great reference from Research Affiliates on the returns you can expect from your asset allocation over the next decade. The firm’s historical modelling has been very good for decades. But my favourite measure of valuation is enterprise value-to-EBITDA because it takes the whole capital structure (debt plus equity, minus cash) outstanding and weighs it against how much earnings it generates. If profit margins are heading lower, as recessions historically portend, then profitability is going in the wrong direction, and the speculative central bank froth is more hope than reality.

If you want to bet on the Fed and other central banks controlling the system, go for it. But, if you care about big picture fundamentals, you have to understand that being aggressive at these levels is fundamentally a bad bet and far more speculative. For me, it’s always about investing with the highest-probability outcome.

Sign up for my monthly Berman’s Call webinar next Thursday night 7 p.m. ET here and follow me on my new YouTube Channel.

Follow Larry online:

Twitter: @LarryBermanETF

YouTube: Larry Berman Official

LinkedIn Group: ETF Capital Management

Facebook: ETF Capital Management

Web: www.etfcm.com

Advertisement