Jan 23, 2017

Larry Berman: Reducing portfolio risk with Smart Factor Index ETFs

By Larry Berman

For the sixth year, I’m attending the www.ETF.com Inside ETFs conference in Fort Lauderdale, Fla. This is increasingly the best ETF conference going. One of the best presentations each year comes from the work done by Research Affiliates. We have had them on the show several years ago. I’m sharing some of their best research with BNN viewers today and on my current roadshow.

Over the past few months, we have had several ETF providers on the show talking about all these smart index factors they use to create smarter index ETFs.

Today I want to bring it all together in context of a portfolio and why using these ETFs can help you reduce risk and add to returns. Diversifying portfolios across different styles of smart indexes can adds significate benefits. As they say, diversification is your only free lunch.

Research Affiliates did a 40-year study on factor index excess return versus the traditional market cap index approach. The results are impressive from a return and risk perspective, but one needs to understand a little bit of math.

Individually, the factors deliver an average of 2.4 per cent excess returns and have an average risk factor (standard deviation) of 12 per cent as we see in the graphic. The Sharpe Ratio, which I have discussed in the past, is a key measure of risk-adjusted returns.

While the alpha (outperformance) of smarter index and factor strategies are great, the best part of using these indexes is that the path of returns amongst the factors tend to have very low correlations with each other. When they are combined in an equal weighted portfolio, we can significantly reduce overall volatility in portfolios and improve our risk-adjusted return.

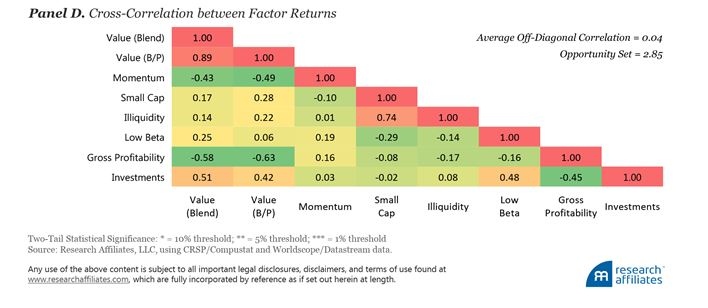

The graph shows the cross-correlation of factor returns. The low correlations between all the factors means they go up and down in price very differently. For example, Momentum and Value have highly negative correlations over long periods of time, which means we can build portfolio diversification. Lower risk and higher returns (Sharpe Ratio) is the key input into the Sleep-at-Night portfolio approach I use.

For those of you that like to get down and dirty and really understand the meat, here is a link to the full report on the Research Affiliates website.

I love the idea of using smart indexing strategies to add returns and lower volatility in portfolios. Learn how to use techniques like this and how to be a smarter investor in our 7th season across Canada speaking tour. Free registration at www.etfcm.com. Help us raise money to fight Cancer and Alzheimer’s by making a voluntary donation with your registration. Over the past few years, Berman’s Call roadshows have raised over $200,000 for charity thanks to BNN viewers and our sponsors.