Sep 12, 2022

Larry Berman: The need for alternative portfolio solutions and the inflation stress on yields

By Larry Berman

Larry Berman's Educational Segment

VIDEO SIGN OUT

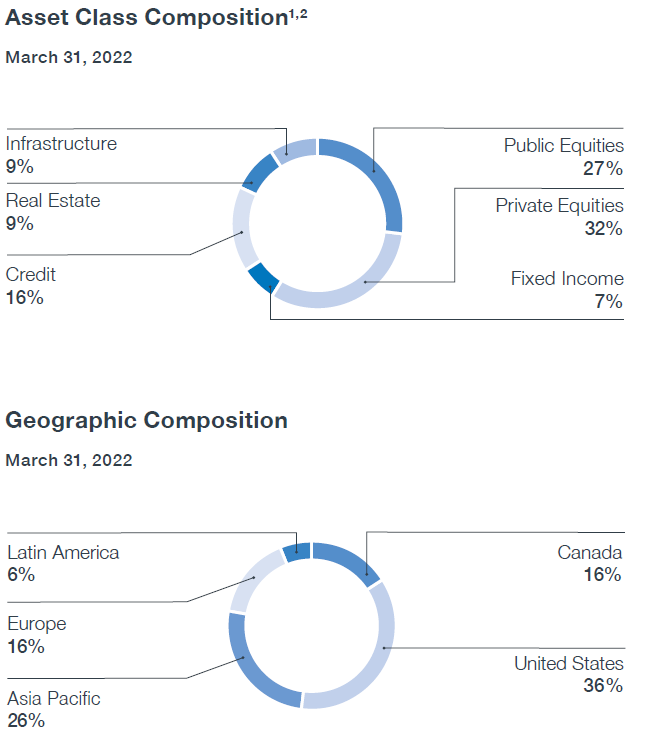

We were asked recently on social media if balanced ETFs like HBAL, VBAL, XBAL, ZBAL are good for passive investors. The answer is yes. They do a good job at what they are designed to do. But in order to deliver goals for your retirement savings, the answer might be no! There is a growing need for alternative income and yield sources to meet these goals. Have a look at what Canada Pension Plan (CPP) is doing with our retirement portfolios. Public market exposure makes up less than half our retirement savings and only 16 per cent is in Canada.

The traditional 60:40 balanced portfolio is linked to the idea of risk premiums. Slowing growth and high inflation is a bad combination for risk premiums. It’s not surprising that this is the worst year for balanced portfolios in decades. The good news is that Canada’s Pension Plan is ahead of the curve. The bad news is that your self-directed plans probably are not. The bond market charts suggest it might get worse before it gets better. Long-term U.S. treasuries are at a key inflation point.

Equity Risk Premium is the difference between returns on equity/individual stocks and the risk-free rate of return. The risk-free rate of return can be benchmarked to longer-term government bonds, assuming zero default risk by the government. Usually, equity valuations are linked to movements in longer-term rates, but not always.

The chart of 30-year treasury yields shows that the 3.50 per cent area has been a key inflation point for most of the past decade. A break here suggests a move towards four per cent. A simple look at the chart suggests persistent inflation could push long bond yields closer to five per cent. This would significantly stress equity risk premiums at a time where growth and inflation are a headwind to margins. While we do not see the latter happening, the risk is worth considering. You may have heard in recent years, yields are low so equities can trade at higher valuations. What if yields are going to move higher under the weight of inflation and the U.S. Fed unwinding its asset purchases?

We are focusing in on 2013, because that was the last time that U.S. long bonds were above current yields. In 2013, we had an unusual combination of rising bond yields (taper tantum), falling forward equity earnings expectations (this is just the beginning), and massively expanding stock multiples (unlikely we see this now). That was a very difficult market to understand, but we were still recovering from the global financial crisis, and sentiment was generally more positive, and the starting P/E was 13 going to 16, not 22 going to 16. The missing ingredient was the rate of inflation and the rapidly tightening financial conditions.

While we are expecting EPS outlooks to weaken over the next year or so, we doubt that equity markets can rally like they did in 2013. Normally when we look back in time to see what happened when, we gain some insight. This time, it’s far more challenging.

What’s different this time? For the central banks of the world to contain inflation, they lack the ability to stimulate (pivot to rate cuts) risking the mistake of the 1970’s when the U.S. Fed eased and inflation shot significantly higher. Enter the period of higher for longer that the U.S. Fed has adopted in the now infamous Jackson Hole declaration and in subsequent FOMC member speeches. Governments also have a fiscal challenge in terms of budget stimulus (perhaps with the exception of China) to help the economy. In other words, what exists today are far more headwinds than tailwinds, which suggests that while we will see these periodic periods of market stress relief, we do not yet see a path to launch a new bull market.

My point in all of this is that navigating the traditional 60:40 portfolio risk in the coming years will likely be tough. Will bonds break or won’t they? What will equity risk premiums do to the multiple? I think Canadians should consider what CPPIB is doing with our retirement savings and diversify into alternative investments (and I do not mean Crypto) too.

These can include option based ETF solutions, but there is so much more. The challenge is that many of these private asset classes are not available to the average investor. Come out to my keynote at the Toronto Money Show on Sept 17th and hear a bit about how we are doing it.

Follow Larry online:

Twitter: @LarryBermanETF

YouTube: Larry Berman Official

LinkedIn Group: ETF Capital Management

Facebook: ETF Capital Management

Web: www.etfcm.com