Oct 29, 2018

Larry Berman: What the eurodollar curve tells us about future rates

By Larry Berman

When the market speaks it makes sense to listen.

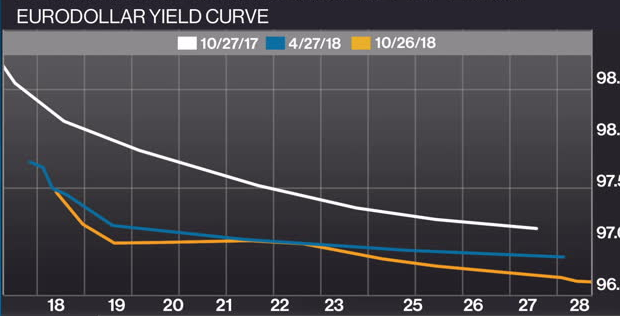

Our chart this week looks at the changes in the eurodollar yield curve over the past year. Eurodollar futures are the backbone of the global banking system. They reflect the expectations for (LIBOR) funding rates for the next decade. For example, the two-year interest rate is made up of a series of eight quarters of three-month rates. Welcome to the swap market, the largest derivatives market in the world, and the lifeblood of the banking world. Banks generally borrow short and lend long for their funding books. When the yield curve inverts, banks struggle to make money lending and credit contracts. In modern times, it’s the core of the economic engine, the credit cycle is the biggest driver of economic growth and contraction.

In the past few months, we have started to see the curve invert around December 2019 at a rate of about 3.20 per cent meaning about two or three rate hikes over the next year. And while the back months still point to higher rates, they are at 3.5 per cent all the way out to 2028. Historically, an inversion in the swap market curve like this is a good proxy for when the recession could hit. We need to watch the behaviour of floating rates around this key inflection point for a sign that they will be pricing in the next easing cycle. We are not anywhere close to that yet.

It looks like 2020 is where consensus is building for the next recession and based on recent earnings reports, we should expect to see some pressure build on forward earnings estimates. Current estimates for the S&P 500 area bit below 180 for the end of 2019 and a ridiculous 197 for the end of 2020.

If 2020 is a recession year, and it’s a bit worse than average (it could be far worse than average), earnings for 2020 will fall about 25 per cent. So the 180 for 2019 turns into about 130-135 for 2020. The range of forward price to earnings ratio in a recession is between 11-14 with an average around 13 which gives us a downside target for the S&P 500 around 130 eps x 13x = 1690, but it could be as low as 1430. The previous highs in the 1500s from 2000 and 2007 could offer some support.

Interest rate markets and the yield curve are our best forecasting tools for timing of a recession, but none of this is absolute. Historically, the S&P 500 falls about 30 per cent in a recession and could easily be 50 per cent. Some mitigating factors will be policy response as it often is. A Democratic House of Representatives could see a massive spending bill for infrastructure in 2020 pushing a technical recession out further, but not eliminate it.

I expect equity markets will stabilize this week and have a bounce back rally into yearend. If we can’t make a new high in the S&P 500 by the end of Q1, it will be a confirmation that the recession is lurking and we should get ready for a bad 10-18 months of equity markets. For now, we are cautious tactical dip buyers.

Our fall roadshow dates are out. Come out and find out How to profit while protecting in the longest bull market of all-time where I will look at some of my top sector ETF picks for the next few years and teach you how to build balanced portfolios using less risky options strategies that will work better in the next few years. Register free at www.etfcm.com and as always we ask for volunteer donations to one of our two favourite charities. Children’s cancer research at the Sick Kids Hospital and Alzheimer’s and dementia research at the Baycrest Hospital.

Toronto - Etobicoke - Saturday November 3, 2018

Halifax - Wednesday November 7, 2018

Montreal - Laval - Thursday November 8, 2018

Ottawa - Saturday November 10, 2018

London - Tuesday November 13, 2018

Toronto - Markham - Saturday November 24, 2018

Victoria - Wednesday November 28, 2018

Vancouver - Saturday December 1, 2018

Follow Larry Online:

Twitter: @LarryBermanETF

LinkedIn Group: ETF Capital Management

Facebook: ETF Capital Management

Web: www.etfcm.com