Jul 30, 2018

Larry Berman: Why 3% growth isn't realistic

By Larry Berman

U.S. President Donald Trump’s troops were out in full force on the Sunday talk show circuit touting the four per cent GDP number that was reported for the second quarter on Friday.

U.S. Treasury Secretary Steven Mnuchin was part of that group, and told Fox News he thinks the U.S. is on track for four or five years of sustained three per cent growth.

First, the one-time items not to be repeated like the surge in soybean purchases and the tax cut induced jump in consumer spending adjusts the numbers down to the mid two-per-cent rage. Thanks to David Rosenberg, chief economist and strategist at Gluskin Sheff, for his analysis of the numbers.

The spending formula for GDP is C = Consumption + I = Investment + G = Government spending + (X = Exports – M = Imports) or net trade. Consumption is the biggest component of the economy in most developed areas these days — around 70 per cent in North America. Another way of looking at GDP it is on the income side of the ledger. How much money do we make? This includes income from work, the number of hours are we working, earnings from our investments, plus the government’s income (i.e. taxes).

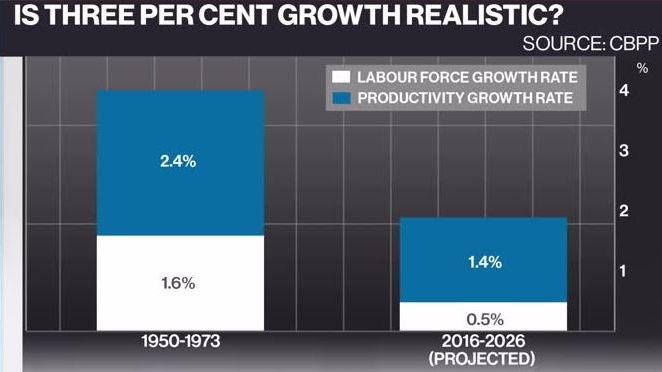

The long run rate of growth is therefore directly tied to the natural growth rate of the population. How many people are working an earning a wage and what percentage of that money they are spending? And on a real (meaning after inflation adjustments) basis, how much their work produces per unit of labour (aka productivity)?

An example of this is the recent minimum wage increases in Ontario. Incomes rise to be sure and that is a good thing, but the output per worker is actually lower per hour (a decline in productivity). Increased pay for increased production is good for productivity, but an increase in pay for the same work is not. A simple wage increase does not add to growth because there is just less profit for the business, which is the business owners’ income. I won’t debate the merits of higher minimum wages here, but suffice to say I believe there is a growing problem with to few holding most of the assets. I will surely address this in a future educational segment on the negative impact on long-term growth.

To increase real growth, we need productivity to improve. It’s generally been falling for decades and there are no shortages of studies saying that hopes for increases in productivity are dim. Some that are more optimistic are heavily biased in my opinion.

With the U.S. unemployment rate around four per cent and near generational lows, the biggest complaint from business in recent surveys are that skilled labour is hard to find. We could easily argue that productivity is likely to fall further because of a skills shortage, and population growth is still very strained by birth rate demographics and boosted by immigration levels. Boarder issues are another challenge these days too. Best case scenario is a natural growth rate around 1.5-2.0 per cent and the degree that governments can get away with running massive deficits to make up the difference.

In the U.S., the Congressional Budget Office – the group that does the official long-term forecasting of U.S. federal spending – projects 4-5 per cent annual deficits for the next decade. That suggests that when the government borrows a dollar to spend, they are getting very little bang for the buck. Spending needs to be tilted towards generating productivity if there is any hope in sustainable growth above this 1.5 to two- per-cent level. During the golden age (post WWII baby boom), the productivity growth rate was massive. When the government borrowed a dollar and spent it, it created all sorts of knock on private capital investment, which created jobs and productivity. Fixing potholes and bridges does not give you the same economic lift that it did when those roads and bridges were first built. Building walls certainly does not help.

With late-cycle inflation pressures building, we can expect the U.S. Federal Reserve (and other global central banks) to continue to raise rates and fight inflation pressures despite Trump’s displeasure. This will virtually assure a recession in the next few years, as the Fed has caused every recession post WWII.

Don’t be taken in by the growth propaganda Trump’s troops are pushing. We are in the late stages of the bull market and investors should be more cautious with their portfolios not more aggressive as a three-to-four per cent+ growth outlook would suggest.

Follow Larry Online:

Twitter: @LarryBermanETF

LinkedIn Group: ETF Capital Management

Facebook: ETF Capital Management

Web: www.etfcm.com

in New York, U.S., on Monday, Dec. 19, 2016. A cautious tone spread through financial markets as the last full trading week in 2016 began. , Bloomberg News")