Aug 9, 2021

Larry Berman: Will bearish seasonal patterns impact timing of monetary and fiscal policies?

By Larry Berman

Larry Berman: Seasonal patterns are most powerful in markets when you have a fundamental catalyst

VIDEO SIGN OUT

The Fed is inching closer to reducing stimulus (debt monetization). Congress is getting antsy about all the spending, but knows that an infrastructure bill is needed. The progressive Left in the House wants even more. Deficits going forward will be north of one trillion annually (five per cent of GDP) based on estimates from the Congressional Budget Office (CBO). Who is going to buy all those bonds if the Fed starts to taper? Bonds will clear market demand with higher yields or a weaker currency, so it becomes far more attractive for foreign investors if the Fed is pulling back. The Fed has bought most of the new issuance in recent years. This chart shows the size of the Fed balance sheet relative to the U.S. economy. They were able to reduce the size a bit as they were tightening in 2017-2018, but then the stock market revolted.

So far, equity markets do not care at all with earnings expectations growing rapidly. At the start of the year, the S&P 500 was expecting about $164 for 2021, that number is now almost $200. The expectation for 2022 is over $218. At a still high 20x multiple, targets of 4000 (2021) and 4360 (2022) are in the rear-view mirror. Earnings are the driving factor and we have not seen a five per cent drawdown in U.S. equities since February/March, the last time seasonal factors were most negative.

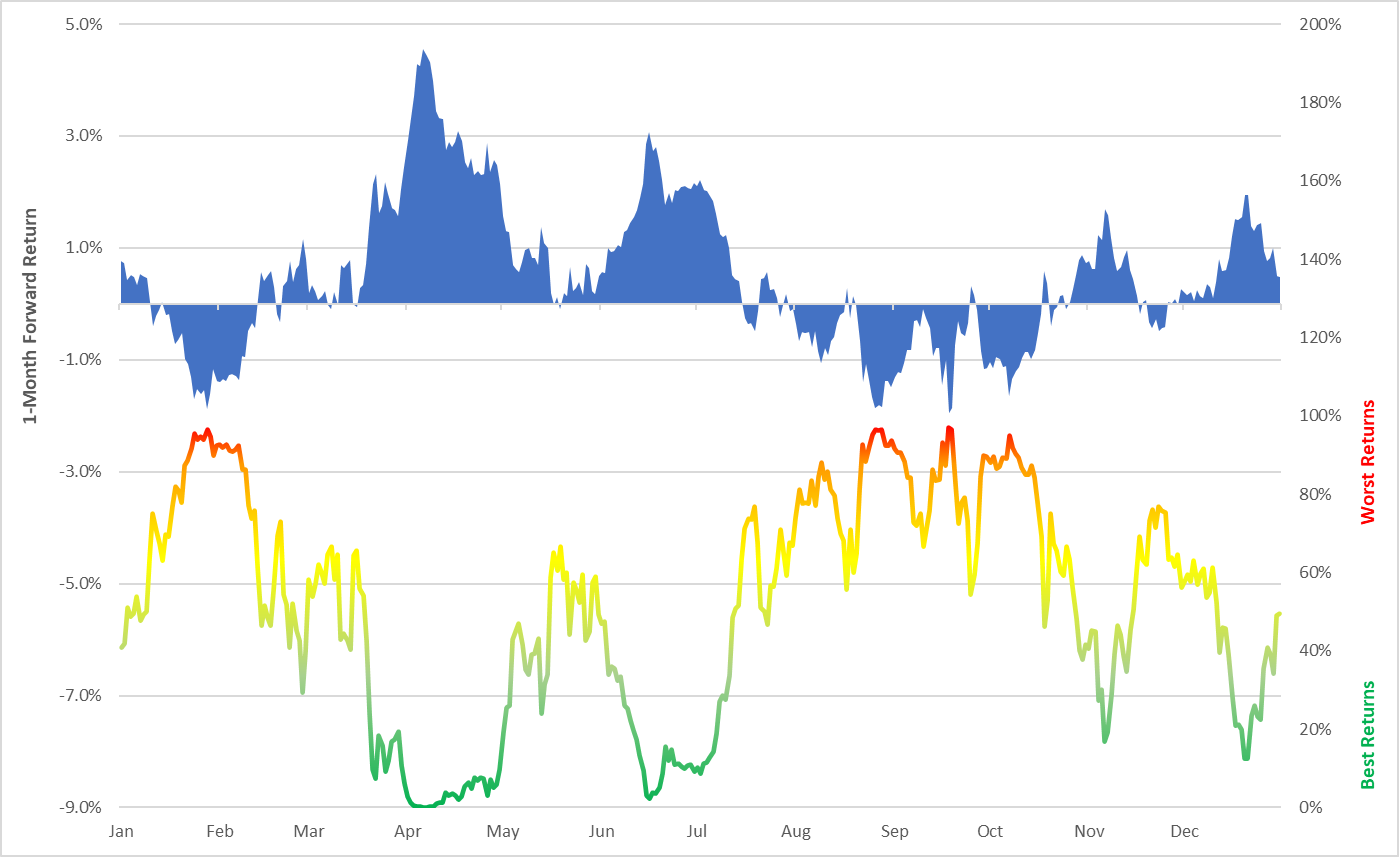

Seasonal patterns are strong influences a few times per year. The biggest is the late summer period when following a strong summer. This year, that seasonal pattern has been highly correlated with market behaviour. Since 1928, the seasonal pattern in the first year of a presidential cycle is particularly weak for the next few months. Our chart shows the average one-month forward returns (blue line) and the risk levels in the lower chart. The seasonal patterns do not turn positive again until November.

It is impossible to say how impactful these influences will be. We do know that this has been a stimulus and liquidity driven market. When the driving factors start to change, risk factors go up. Earnings have been good, but we expect a modest cooling in the coming months.

Monetary and fiscal policies do matter as they drive earnings. But a market priced for perfection and a Goldilocks outcome is subject to disappointment. This is not an end of cycle bear market risk, a five-10 per cent correction at this point would be healthier than a continuation of the liquidity bubble that has been driving asset prices.

Follow Larry online:

Twitter: @LarryBermanETF

YouTube: Larry Berman Official

LinkedIn Group: ETF Capital Management

Facebook: ETF Capital Management

Web: www.etfcm.com

in New York, U.S., on Thursday, Dec. 27, 2018. Volatility returned to U.S. markets, with stocks tumbling back toward a bear market after the biggest rally in nearly a decade evaporates. Photographer: John Taggart/Bloomberg, Bloomberg")