Jun 3, 2022

Lockstep stock market is forcing everyone to be a macro trader

, Bloomberg News

Market is telling us probability of recession is really high: Jeff Weniger

VIDEO SIGN OUT

Day-to-day odds-making on whether the Federal Reserve will cause a recession has become the only thing that matters in equities.

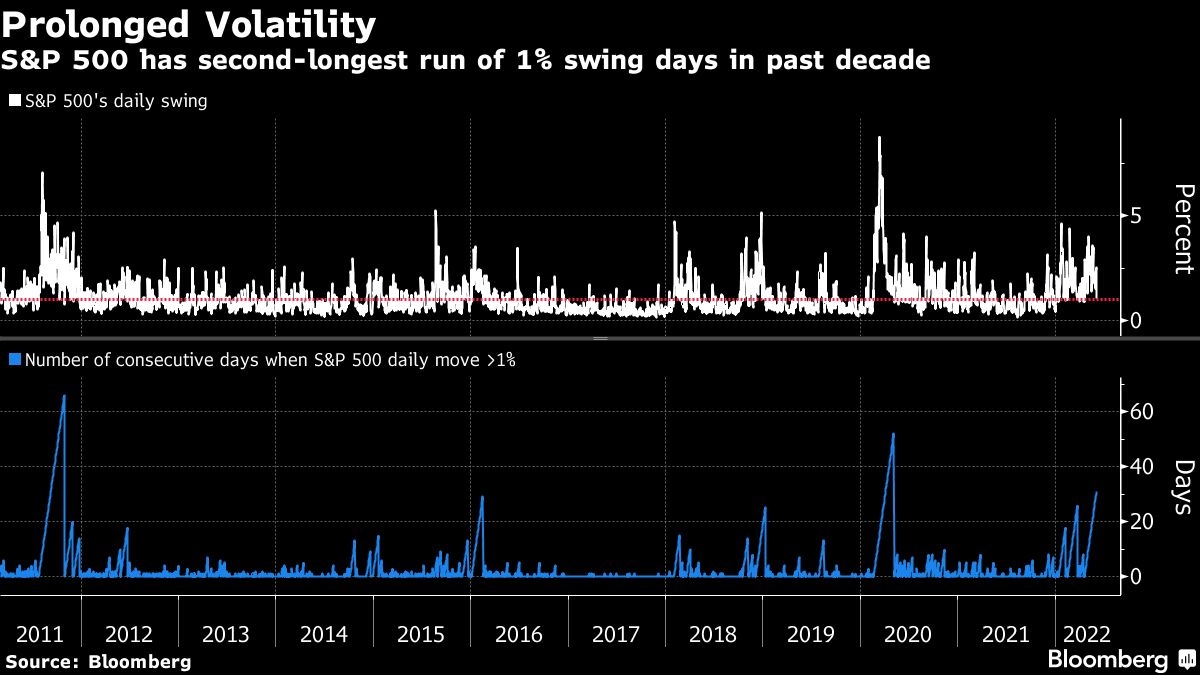

One day feast, next day famine -- obsession with a single input, the economy, has driven measures of correlation among individual stocks to the highest since the coronavirus crash. Whacked around by government data and bond yields, the S&P 500 has now posted intraday swings of 1 per cent or more in 31 straight sessions, the second-longest streak in a decade.

Burned by all the volatility, day traders have kicked the stock-picking habit. Meanwhile, hedge funds are diving into macro bets, convinced they have an edge predicting the future.

“Investors are consumed with big-picture considerations,” said Steve Sosnick, chief strategist at Interactive Brokers. “It’s just not human nature to be able to necessarily zag when everyone’s zigging -- to be thinking in terms of bottom-up clarity, when the top-down is moving around so dramatically.”

Tightening correlations go hand-in-hand with volatility and both are on the rise. May saw nearly unprecedented turmoil in stocks, with S&P 500 plunging more than 3 per cent three different times (as well as on the last day of April), the first time that’s happened since March 2020. The average close-to-close swing in the S&P 500 was 1.5 per cent, the largest in two years.

Synchronized moves theoretically create stock-picking opportunities when good companies fall as much as bad, though finding them apparently requires too strong a stomach for the retail-trader set. Last month, they sold single stocks at a rate that almost matched that seen during the bear market trough in March 2020, according to industry-wide data compiled by JPMorgan Chase & Co.

Hedge funds that make both bearish and bullish equity wagers increased their macro bets in May as the market staged a late-month rebound. Their net purchases of products such as exchange-traded funds reached the highest level since November 2020, client data compiled by Goldman Sachs Group Inc.’s prime broker show.

“They’re trying to play these macro themes,” said Steve Chiavarone, senior portfolio manager at Federated Hermes. “A lot of retail money got into this market because of a stock story or to buy a disruptor,” he added. “What they didn’t necessarily understand, because they don’t have as much experience in the market, is how the macro backdrop could change on them.”

Stocks fell for an eighth week in nine. Energy -- an outlier sector whose rally has bucked the market all year because of surging oil prices -- was the only one of 11 main industries that wasn’t flat or lower over the holiday-shortened period.

Friday’s data on a strengthening labor market sparked a selloff across stocks and bonds amid concern that the Fed would need to speed up its inflation-fighting campaign to slow growth. A day earlier, equities rallied when a hiring report trailed estimates. Meanwhile, warnings of an economic downturn are getting louder among corporate executives.

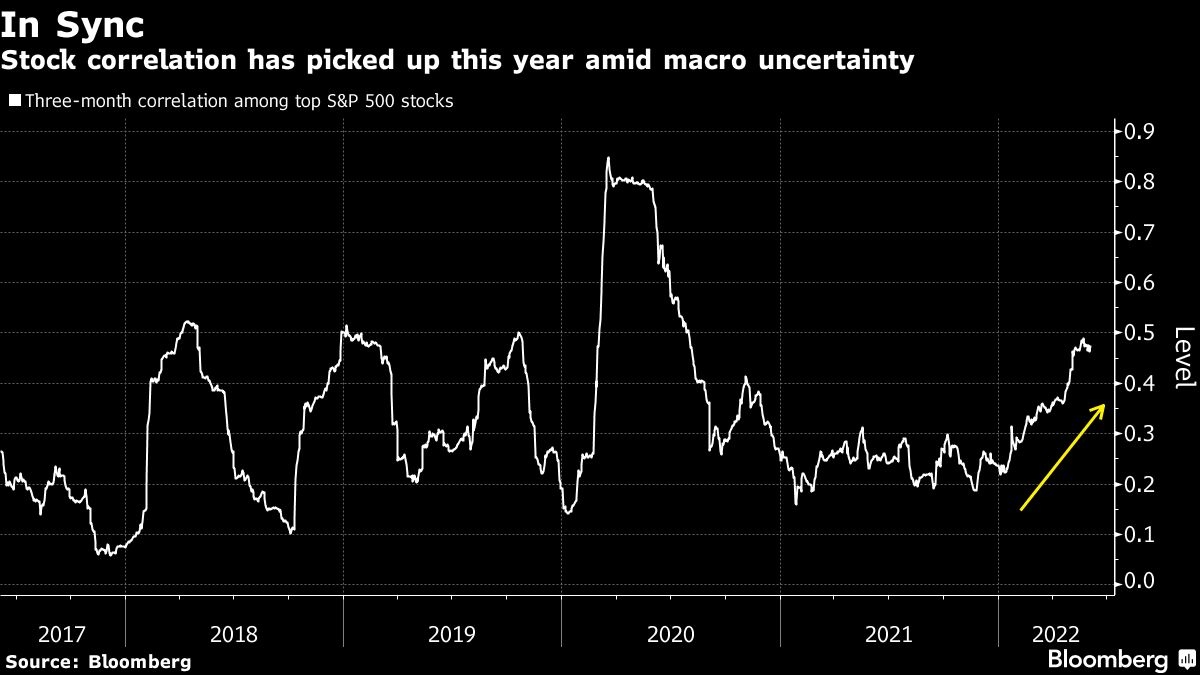

Thanks to energy, performance dispersion among sectors has widened by some measures to one of the largest gaps on record. Yet underneath is a growing tendency for shares to move together. Three-month correlation among the top stocks in the S&P 500 has increased to 0.47 from 0.37 in early April, when the reporting season started. (A reading of 1 means they’re moving in unison.) The recent increase is a departure from the past, when individual stocks tended to chart their own course during earnings season.

Thursday was an example. Microsoft Corp. initially fell after cutting guidance. But with weaker-than-expected data on private hiring and factory orders signaling a slowdown, hope surfacing for a China reopening, and OPEC+ agreeing to increase the size of its oil-supply hikes, macro considerations prevailed and both the software maker and the Nasdaq 100 ended higher.

The market is moving so swiftly, often in opposite directions, that many investors have shortened their investment horizon to avoid being caught wrong-footed. Tom Lee, co-founder of Fundstrat Global Advisors, says one of his clients is scared enough about shifting economic tides that his book becomes nearly flat at the close of every trading day.

“In conversation after conversation, investors describe the current macro environment as one of the most uncertain they have ever seen,” Lee wrote in a note. “The macro outlook changes so dramatically given the extreme data dependence, and in turn, whipsawing market views on Fed policy.”

Even pros at the same firm can’t agree on the market and economic outlook. While JPMorgan Chief Executive Officer Jamie Dimon warned about an economic “hurricane,” the firm’s strategist Marko Kolanovic said the economy will be able to avoid a recession, helping propel a recovery in stocks later this year. At Citigroup Inc., a similar clash played out.

Amid the uncertainty over the path of the Fed’s money tightening and its impact on the economy, investors see a range-bound market. In recent client surveys, 22V Research found that the majority of respondents said, barring any new shocks, they would sell stocks once the S&P 500 rises to a range of 4,200 to 4,350, and turn buyers when the index falls to 3,600. That’s an upside of as much as 6 per cent from Friday’s close of about 4,110, and a decline of more than 12 per cent.

“They key headwinds are all macro ones, and short-term trading is driving the tape,” said Michael O’Rourke, chief market strategist at Jonestrading. “The thinking is, if we could get another leg lower because something goes wrong on the macro front, I’d rather wait for that and buy at a cheaper price.”