Oct 18, 2018

Loonie bulls undeterred by plummeting price of Canadian crude

, Bloomberg News

There’s a lot more to Canada’s dollar than just oil these days.

The industry is less critical than it once was to the nation’s prospects, enabling some Canadian dollar bulls to look past the recent slide in domestic crude prices and focus instead on the outlook for economic growth and the prospect of higher interest rates.

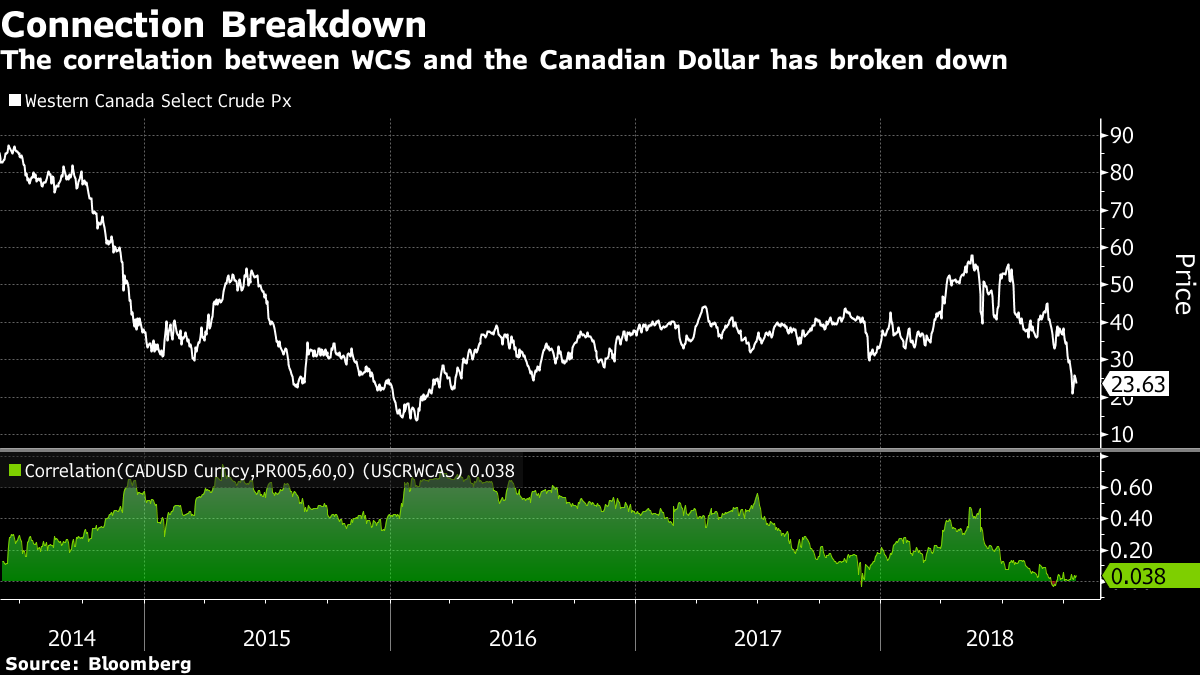

The price of Western Canada Select, or WCS, a local blend that represents about half the country’s crude exports, has plummeted even as global benchmarks such as West Texas Intermediate have risen. Yet analysts continue to predict gains for the loonie, with the median forecast in a Bloomberg survey showing it appreciating to $1.25 per dollar by the end of next year from current levels around $1.30.

“Good economic conditions in Canada are leading toward ongoing tightening by the Bank of Canada,” said Greg Anderson, head of foreign-exchange strategy at Bank of Montreal, who expects the Canadian dollar to strengthen to about $1.27 over the next three months.

While the price of WCS is trading close to its widest discount to WTI on record, the world’s 11th largest economy is running near its potential and the unemployment rate has fallen to around 5.9 per cent as other sectors such as technology boom. Businesses see their sales outlook improving, according to Bank of Canada’s survey conducted last month. And that was even before the country cemented a deal on the North American Free Trade Agreement, which had been a source of considerable uncertainty.

Rate Hikes

The fixed-income market is currently pricing in about four increases over the coming year for the BOC’s benchmark, which currently stands at 1.5 per cent. The odds of an increase at next week’s meeting have climbed to around 84 per cent and economists surveyed by Bloomberg predict it will rise to 1.75 per cent, the highest in a decade.

Oil prices are no longer a good proxy for Canadian currency trends, in part because the local energy sector isn’t receiving the kinds of foreign investment it used to, according to Bank of Montreal’s Anderson. Government data show that oil and gas accounts for around 15 per cent of the foreign stock of investments in Canada. That’s down from about 17 per cent in 2014, before a decline in oil prices triggered a swath of restructuring across the industry.

The correlation between the loonie and WCS was strong as recently as 2016, before falling off, according to data compiled by Bloomberg. The correlation was strong even for most of 2015 as well, when a sharp decline of oil prices triggered an outflow of investment in Canadian energy industry.

That said, energy products -- including oil -- do still account for a significant chunk of the nation’s exports, so it certainly can’t be ignored by the nation’s central bankers. It’s something that the Bank of Canada may point as a reason to insist on pursuing a gradual tightening path, according to Andrew Kelvin, senior Canada rates strategist at TD Securities.

There is also potential for energy to recover some of its influence on the currency further down the track with the development of a $40 billion liquified natural gas project on the coast of British Columbia. But cash is unlikely to flow from that for quite some time and it’s largely irrelevant for the loonie at the moment, according to Darcy Briggs, a Calgary-based portfolio manager at Franklin Bissett Investment Management, which has around $6 billion in fixed-income assets.

With the new North American free trade agreement pending ratification, and the Bank of Canada’s rate hike path priced-in, some strategists are watching Canada’s terms of trade. For example, lumber has slid by nearly half since a May peak, and that can weigh on the loonie, said Shaun Osborne, chief foreign-exchange strategist at Bank of Nova Scotia.

“It’s not just Canadian oil prices that have declined, quite a few relevant Canadian commodities have as well.” said Osborne. “And that has a long-run impact on the value of the Canadian dollar.”