Apr 8, 2020

Millennials feel financial sting of not one, but two economic crises

, Bloomberg News

Aviv Russ feels like the cards have been stacked against his generation -- and he’s not wrong.

Russ is a millennial, the infamous cohort of people born between 1981 and 1996. He graduated from Boston-based Emerson College in 2009, just as the Great Recession gutted the jobs market for years.

He spent his first few years after school fighting for low-paid work as a production assistant. His mentors told him, “‘Dude, you missed the good years by like five years,’” he said.

Shallow or Deep?

A decade later, just as he had built up savings and was preparing to buy a house, the 31-year-old is out of a job again. The coronavirus outbreak has dried up production gigs in Hollywood, where he works.

No age group will escape the pain of the current economic slowdown, but millennials were already on more precarious financial footing than their elders. They left college with unprecedented levels of student debt and missed out on crucial years of wage growth because of the 2008 downturn.

Compared to other groups at the same point in their lives, people in their 20s and 30s have relatively low levels of home ownership, net worth and real income, according to a 2018 Federal Reserve Board of Governors paper.

“They’re walking a tight rope and there are cliffs on either side,” said Kathryn Edwards, a labor economist at the Rand Corporation. “It’s hard to imagine someone making it through both of these recessions in this age group really unscathed.”

Economic downturns are inevitable, but they’re not usually so severe. And once-in-a-generation recessions don’t tend to occur just a decade apart.

For millennials, the timing of these events has been particularly damaging. People who enter a labor market with high unemployment typically see a 10 per cent hit to income in the first year, with the effect averaging out to a 1.8 per cent reduction in yearly earnings over 10 years, according economists at Yale and the University of Rochester. They also found the impact of the Great Recession on wages to have been “much larger” than previous downturns.

Losing Out?

Because an economic crisis hampers job mobility, the effects of one early on in a person’s professional life can last for the next 20 years, research from Carnegie Mellon economics professor Shu Lin Wee has found.

This phenomenon isn’t confined to the U.S. In Britain, between 2006 and 2014 real earnings fell twice as fast for people under 30 than for those in their 50s, according to the Resolution Foundation.

Meanwhile in Italy, the epicenter of the virus outbreak in Europe, just 24 per cent of houses and land are owned by the young, while the risk of poverty is twice as high among those under the age of 40 than those over 65, according to a study by business association Confindustria.

Other generations will experience their own flavor of economic fallout from coronavirus. The oldest members of Generation Z are graduating into a world of city-wide lockdowns, as countries try to curb the spread of a global pandemic.

Baby Boomers in the U.S. have now suffered successive blows to their retirement portfolios because of market routs. Those are the lucky ones: Almost half of U.S. households 55 and older have nothing saved for retirement. Millions of people of all ages are now unemployed and the International Labor Organization finds over a billion people at high risk of a pay cut or losing their jobs.

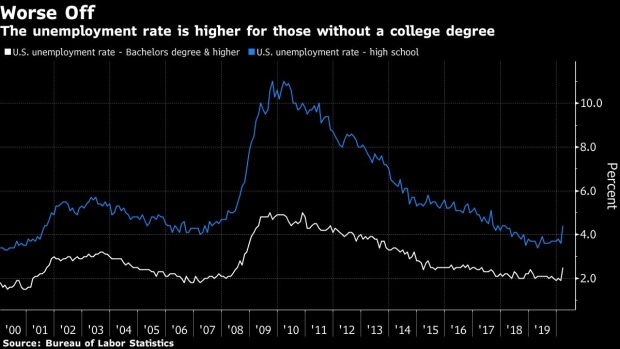

“I worry about the younger guys more,” said Harry Holzer, a professor of public policy at Georgetown University. They’re more likely to get laid off than those more senior, he said, adding, “I worry even more about the people without college diplomas.”

While white collar workers can work from home, sectors largely filled by people without college degrees, such as retail, food services, hospitality and construction have already seen major job losses because of the pandemic.

One such person is Denzel Buie, a 25-year-old glazier living in Philadelphia with his fiance and his three-year-old daughter. He was laid off a few weeks ago. Buie had health care through his employer and now worries that if he gets sick, he won’t be able to afford a hospital visit.

“It makes you feel vulnerable because sooner or later resources that you had built up [are] going to run out,” he said.

As for those in white-collar professions, Chip Espinoza, dean of strategy and innovation at Vanguard University, fears people in their 30s will once again get stymied in career advancement because another recession means Boomers won’t retire on schedule.

“You’re really looking at a workforce that is going to continue to age and continue to create challenges for younger generations in their upward mobility,” he said. Millennials “will have to rent longer, co-habitate longer, and stay in starter homes longer.”

Already millennials, because of their debt burdens and a pricy housing market, had been slow to dive into home ownership, a key way to build wealth. People like Michael Baum, who did manage to buy, fear they made their purchases at the exact wrong moment.

Just two weeks ago, Baum, a 33-year-old special needs teacher, moved into a new house purchased using money from his wedding and family savings in Plano, Illinois. While he still has work, his wife recently lost her customer service job in retail. They not only have a mortgage, but her student loans to pay off still.

“It could be a problem if the unemployment stops,” he said.

-With assistance from Lucy Meakin and Flavia Rotondi.