Vietnam’s Vingroup JSC founder Pham Nhat Vuong provided his strongest backing yet for the company’s electric vehicle unit VinFast Auto Ltd., announcing he plans to inject at least another $1 billion of his personal wealth to back its global expansion.

Initial data on US gross domestic product for the first quarter of 2024 is set to confirm an ongoing economic boom amid a tailwind from surging immigration.

Investors are looking for the next policy domino to fall in Asia amid an escalating campaign against a resurgent dollar, after Indonesia used a surprise interest rate hike to defend the rupiah.

Analysts upgraded their forecast for China’s growth this year after a better-than-expected performance in the first quarter — but they see more signs that the world’s second-biggest economy will struggle to escape from deflationary pressures.

Mortgage stress tests to reduce housing activity to 'unnecessary degree': Study

Shane McNeil, BNN Bloomberg

Mortgages

, The Canadian Press

OSFI’s incoming B-20 underwriting guidelines in 2018 are set to affect already-gun-shy first-time buyers, according to a study released Tuesday.

According Mortgage Professionals Canada’s “Annual State of the Residential Mortgage Market in Canada”, stress-testing of mortgages will prevent an estimated 6-7.5 per cent of Canadians from achieving housing goals, even if those goals appear “reasonable” and “responsible.”

“As a result of the policies’ excessive stringency (using interest rates that are too high), housing activity will be reduced to an unnecessary degree,” the report states.

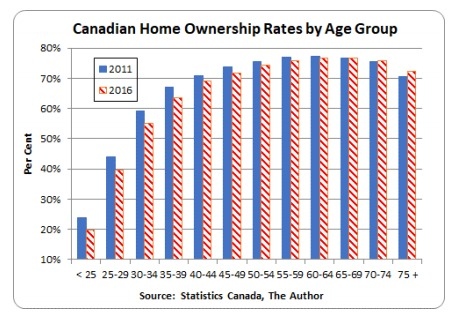

“The homeownership rate in Canada has fallen, as young, middle-class Canadians have found it increasingly difficult to make first-time purchases,” the study’s author and MPC chief economist Will Dunning said in a statement. “With the recent further tightening of mortgage rules, ownership challenges have been intensified, and the ownership rate is very likely to fall further.”

Image courtesy of Mortgage Professionals Canada

The study also estimates that 200,000 Canadian families will fail the new uninsured stress tests by the time Canada next heads to the polls for an election.

However, the study also found that Canadians still see homeownership – and the debt that comes with it – as a good investment.

While total debt among homeowners is rapidly expanding, the level of regret experienced among homeowners is on the decline, which MPC says can be attributed to higher equity ratios. The group also found that regret over homeownership diminishes as the buyers get used to, and begin to repay, that debt.

“During the past decade, some commentators have taken a negative outlook of the housing market. Yet, Canadians have consistently shown confidence in residential real estate,” MPC President and CEO Paul Taylor said in a statement. “These surveys have told us repeatedly that Canadians are happy with the real estate decisions they have made.”

On a scale of one-to-10 Canadians averaged a 3.67 when asked to react to the statement “I regret taking on the size of my mortgage.” While this is up from the 3.60 score in 2016, it is down substantially from the 2010-2014 scores that ranged from 3.82 to 4.04.