Oct 25, 2022

Musk tells debt bankers he plans to close Twitter deal on Friday

, Bloomberg News

At the end of the day, Elon Musk capitulated on Twitter deal: Bruce Croxon

VIDEO SIGN OUT

Elon Musk pledged Monday to close the acquisition of Twitter Inc. by Friday in a video conference call with bankers helping fund the deal, according to people with knowledge of the matter.

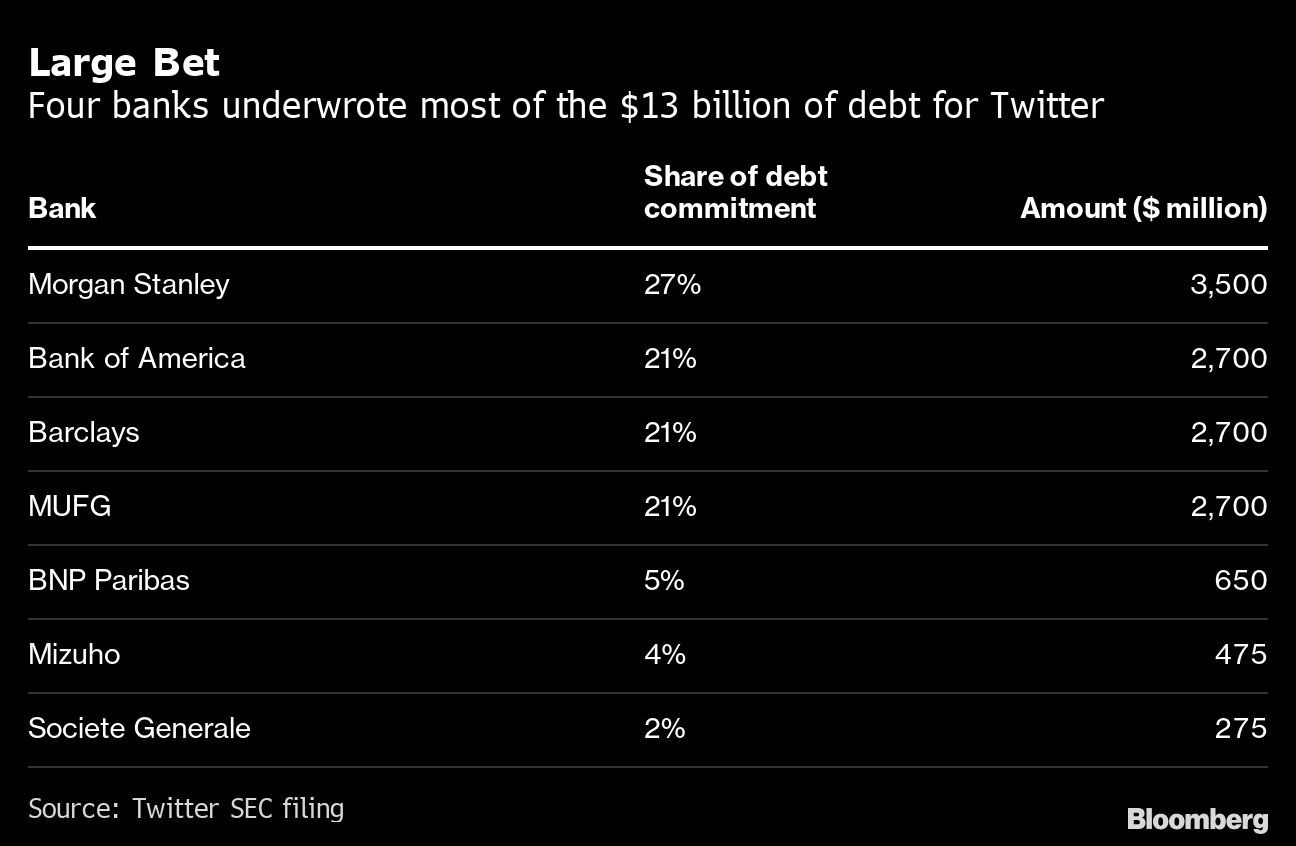

The banks, which are providing US$13 billion of debt financing, have finished putting together the final credit agreement and are in the process of signing the documentation, one of the last steps before actually sending the cash to Musk, said the people, who asked not to be named discussing a private transaction.

Twitter shares jumped on the news and traded as high as US$53.18, approaching Musk’s US$54.20 acquisition price.

The Wall Street lenders, led by Morgan Stanley, had already been preparing in recent weeks to fund the debt, Bloomberg previously reported. But nothing is ever certain with Musk, the mercurial billionaire who only weeks ago was seeking to back out of the deal. These latest developments suggest he is in the final stages of closing the transaction by a court-issued Oct. 28 deadline.

The banks are expected to receive one of the last formalities -- a borrowing notice -- on Tuesday, and the cash is expected to be held in escrow on Thursday, the people said.

Morgan Stanley and Twitter declined to comment, while representatives for Musk didn’t respond to a request seeking comment.

BACK PAIN

On the call, Musk also promised to help the banks market the debt to money managers after the deal closes, the people said.

That is key for the group of seven banks, which have been left in a lurch after Musk’s sudden reversal to go through with buying Twitter in early October. Normally the banks would offload debt commitments to money managers in the form of junk bonds and leveraged loans before a deal closes, but the compressed timeline and a global deterioration of credit conditions have forced them to keep the debt on their books.

In a normal buyout transaction, the banks, new owner, and company management would come together to hold calls with investors to sell the debt and pitch the business. But the original debt commitment letter stipulated that Musk’s side would help for up to 30 days after closing, and that Musk would participate for at most two hours in any investor meetings.

Banks are facing paper losses of roughly US$500 million on the transaction -- pain that would be realized once the debt is sold to institutional investors. The average cost of borrowing spiked this year along with accelerating inflation, recession fears, and geopolitical turmoil, well above the 11.75 per cent maximum interest rate that the banks promised Musk on the riskiest tranche of the debt, leaving them on the hook for the difference. Triple-C rated junk bonds are trading at about 15.8 per cent on average, according to Bloomberg index data.

Wall Street banks have already had to use about US$30 billion of their own cash this year to fund loans for acquisitions and buyouts that they weren’t able to offload to investors. That would swell to over US$40 billion once banks fund the Twitter deal on Friday, as expected.

Twitter’s total purchase price is US$44 billion. The banks committed to provide the debt financing in April -- when investor appetite for risky assets was more robust -- and originally hoped to sell US$6.5 billion of leveraged loans and US$6 billion of junk bonds, split equally into secured and unsecured tranches.

They also provided US$500 million of a special type of loan typically held by banks called a revolving credit facility, which Twitter will be able to borrow from and pay back until maturity.