Who knew the unsexy work of disciplined inventory and expense management could get Wall Street this excited?

Or, at least that’s what I think is driving a Thursday morning surge in shares of Nordstrom Inc., which reported second-quarter earnings late Wednesday. The retailer beat analysts’ earnings per share estimates, an outcome it chalked up to deft expense control. But, to my mind, practically everything else about this report is worrisome for Nordstrom, and indicates that something has seriously gone off track recently for this company.

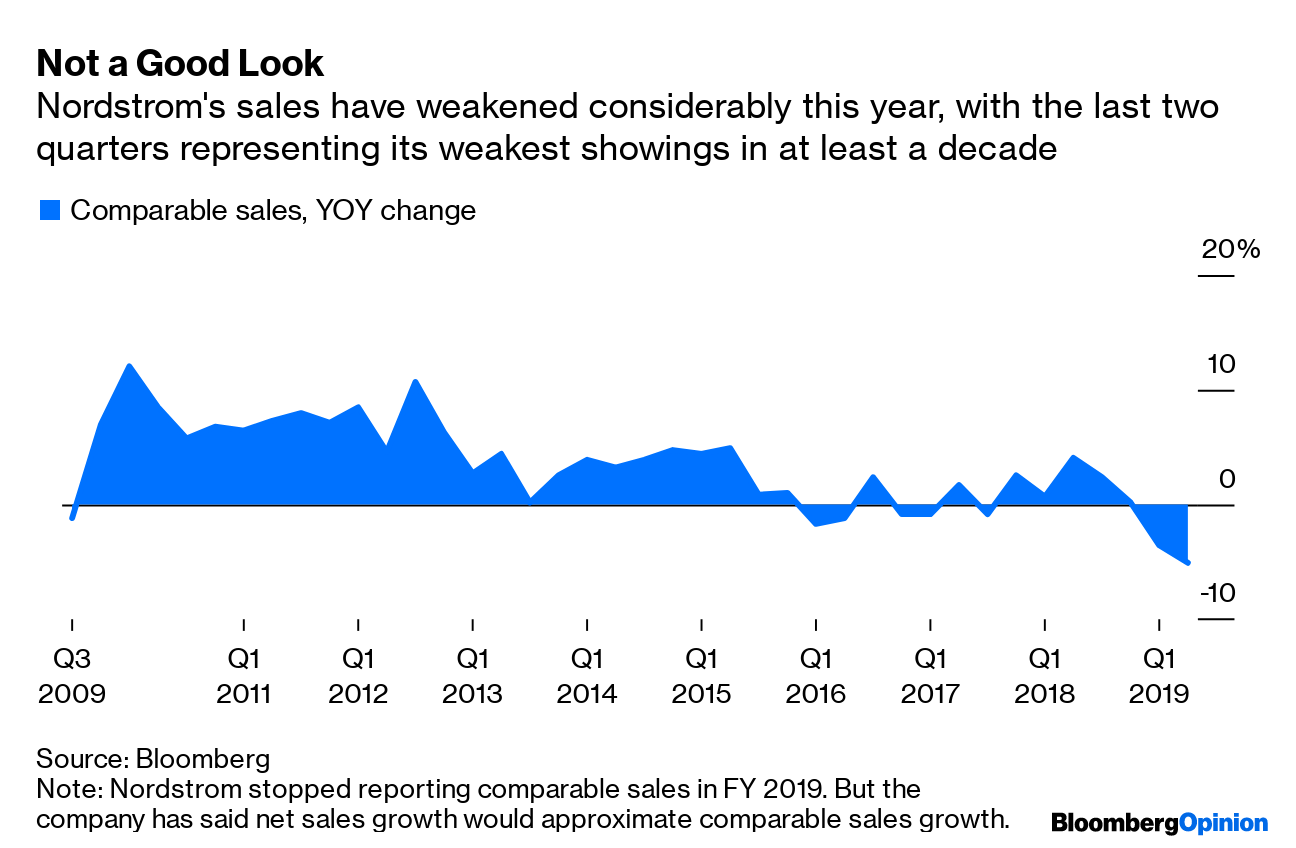

Nordstrom said net sales fell 5.1 per cent from a year earlier in the quarter. The company no longer reports comparable sales, a measure that typically captures sales at stores open more than a year and online sales, and is considered a key benchmark of retailer health. It said when it announced that decision that net sales in fiscal 2019 would effectively approximate comparable sales. So, if we assume that to be true, Nordstrom effectively just had its worst results in at least decade on this metric. The first quarter was the second-worst.

It’s not like one of its major lines of business provided reason to dismiss troubles at the other. Net sales plunged 6.5 per cent in the full-price division, an especially bad result when you consider Nordstrom held a major promotional event in the quarter, its Anniversary Sale, which is traditionally an important driver of annual revenue. TJX Cos. managed to deliver positive comparable sales in the second quarter in its division that includes off-price wunderkinds Marshalls and T.J. Maxx, and yet Nordstrom Rack, a direct competitor, saw net sales fall 1.9% from a year earlier.

Adding to the gloom, Nordstrom’s e-commerce sales rose just four per cent in the second quarter. I realize that the company has a relatively mature online business for a legacy brick-and-mortar retailer, drawing 30 per cent of its overall sales from e-commerce. However, this is a significant downshift from the rate of growth the company had been recording in this channel.

The bleak news doesn’t stop there: Nordstrom reduced the top end of its annual earnings guidance. Also, its previous outlook for net sales was a range of flat to a two-per-cent decline; it is now just for an approximately two-per-cent decrease. Achieving even this dimmer outlook will require a pretty speedy change in momentum from the first half of the year, and I’m not sure executives have adequately explained how they can turn on a dime and pull that off.

All of this is what leaves me perplexed as to why this report would do anything but make investors squeamish about Nordstrom’s prospects.

I’ve long thought of Nordstrom as something of a unique retailing species. While it is technically a department-store operator, I’ve resisted thinking of it as such, because it has largely avoided all the typical problems we associate with that troubled format. But earnings results like these are making me reconsider whether it is really different enough to withstand the relentless pressure facing the category.

These numbers make it harder to ignore stumbles by this company that might once easily have been overlooked. In the first quarter, Nordstrom erred with a change to its loyalty program that it believes kept shoppers away from its stores. In the second quarter, sales at its Anniversary Sale were soft, which co-President Erik Nordstrom told investors was in part because “We simply ran-out of our top items.” These missteps don’t exactly show the company to be in top form.

I don’t think Nordstrom’s situation is hopeless. With less than 140 full-price stores, I’ve noted many times that Nordstrom is fortunate to not have a bloated store portfolio — unlike Macy’s Inc., J.C. Penney Co. and Kohl’s Corp. Its locations don’t tend to be in the dumpy malls that are turning into shopping ghost towns, and I see promise in its tiny-format Nordstrom Local concept. But its results so far this year suggest these factors might not be sufficient protection from the curse that is being a department store in 2019.

Advertisement