Nov 1, 2018

October proves to be rare good month for both gold and U.S. dollar

, Bloomberg News

Normally, investors wanting to guess which way gold is headed look to the U.S. dollar.

When the greenback goes up, the precious metal almost always goes down. Few assets have a stronger inverse correlation to the Bloomberg Dollar Spot Index, with gold favored as a hedge against the world’s reserve currency.

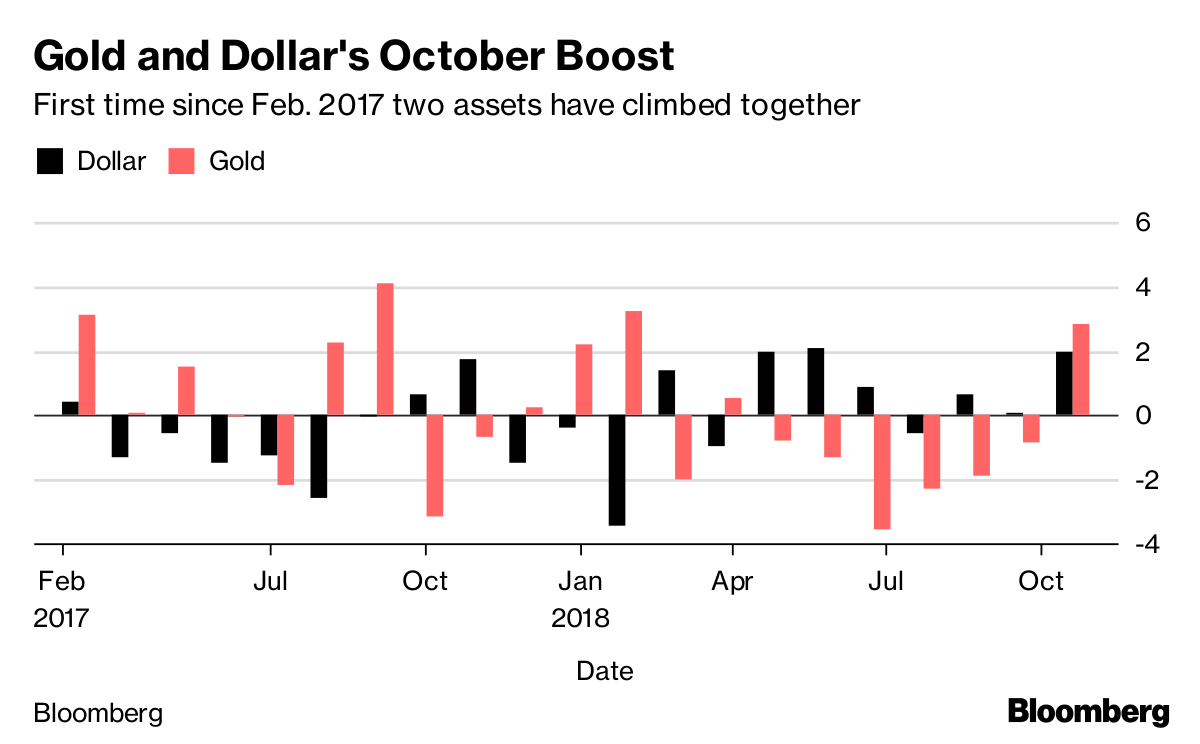

But that’s not what happened in October, a month when both assets gained ground for the first time in 20 months.

The change has been driven by last month’s rout in emerging market equities, and particularly in China, which has seen investors seek out haven assets. At the same time, the strength of the U.S. economy is benefiting the dollar.

The inverse relationship between gold and the dollar could continue to break down, said Michael McCarthy, chief market strategist for Asia Pacific at CMC Markets in Sydney. Concerns about rising inflation and the outcome of the midterm Congressional elections could drive gold higher.

“We’re likely to see both a rising U.S. dollar and a rising gold price at least into next Tuesday night,” McCarthy said by phone. The midterms are “a potential game-changer. Predicting beyond that at the moment is very difficult.”

The Bloomberg Dollar Spot Index rose 2.3 percent in October to the highest in 17 months, while gold gained 2 percent, the most since January. The metal advanced 0.8 percent to $1,224.64 an ounce at 10:04 a.m. in London.

Risk Aversion

Gold’s gains owe “mostly to the recent de-risking in equity markets that we view as a correction rather than being in the throes of a bear market,” Harry Tchilinguirian, head of commodity-markets strategy at BNP Paribas SA, said by email. While the bank raised its forecasts for gold, it still sees it declining, from an average $1,260 an ounce in 2018 to $1,145 in 2019.

“Risk aversion has crept back in as we’ve seen declines in emerging markets around the world and now Asian markets following,” said Mark O’Byrne, Dublin-based executive director at brokerage Goldcore Ltd. “Fund managers are rebalancing after a very good run on the stock market, taking chips off the table and putting money into gold and cash, hence why the dollar has also risen.”

The inverse correlation on a 120-day basis has been narrowing since June, with the trend accelerating in October. It has gone from as strong as minus 0.75 to less than minus 0.55. A reading of minus 1 means the two are always moving in the opposite direction.

Gold typically acts as a hedge not only against the dollar, but against fiat currencies in general. That the metal is priced in dollars further strengthens the connection.

The reverse correlation faltered in June 2016, after the Brexit vote, and broke down completely during the early stages of the Greek debt crisis in 2010. When things are going badly everywhere else in the world, the dollar and gold act as a haven simultaneously.

Gold and the dollar may continue to rise in tandem in the short term, “but I’d be amazed if that continues into 2019,” said O’Byrne. U.S. policymakers won’t want the currency to go much higher, whereas gold demand is just starting to come back. “So although I wouldn’t want to bet against the dollar in the short-term, longer term it looks very positive for gold.”