Oct 14, 2022

Oil posts weekly loss as slowdown fears dim demand outlook

, Bloomberg News

It's surprising that oil hasn't dropped more: Bill O'Grady

VIDEO SIGN OUT

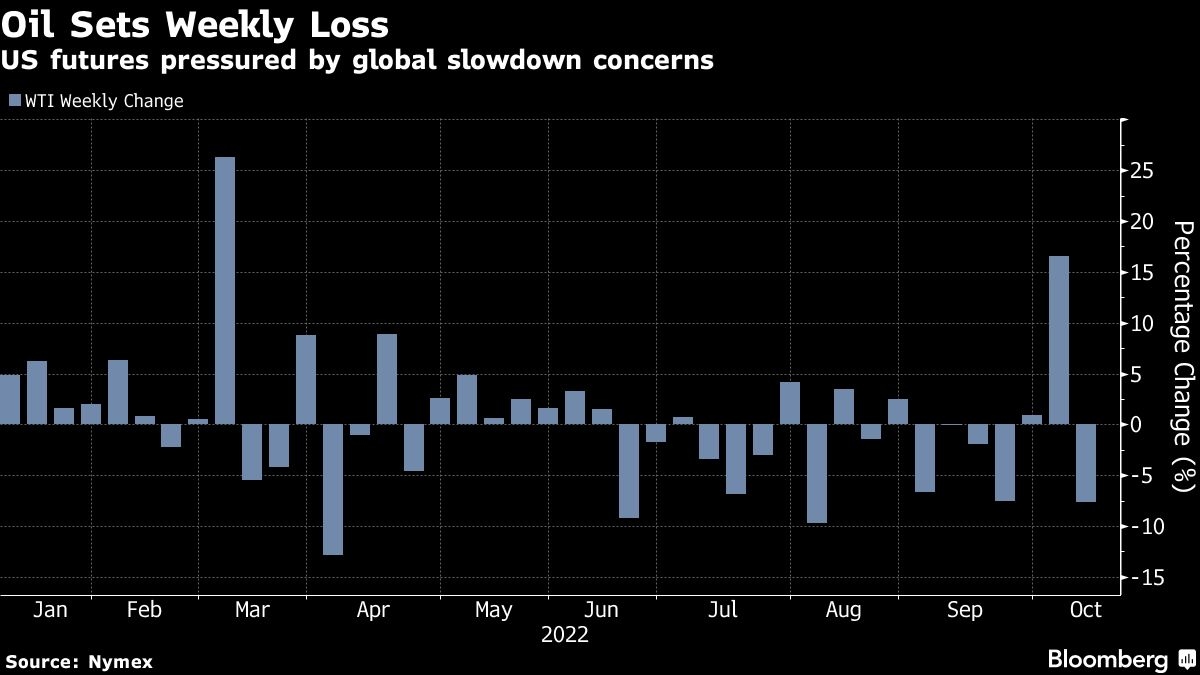

Oil posted a weekly loss as inflation-fighting measures and muted Chinese demand soured the market’s outlook, blunting some of the sting from OPEC’s upcoming supply curtailments.

West Texas Intermediate futures settled below US$86 a barrel, falling 7.6 per cent this week. A measure of U.S. inflation jumped to a 40-year high last month, spurring expectations that the Federal Reserve will have to continue hiking interest rates that could slow growth and potentially hit energy consumption.

Prices this week shed some of the gains spurred by the Organization of Petroleum Exporting Countries and its allies’ decision to sharply reduce output in November. Crude has also struggled as demand in China, the largest importer, remains subdued with the government pressing on with its Covid-Zero policy. The country’s critical twice-a-decade Communist Party Congress opens this weekend.

“All the major crude demand stories are turning very bearish for crude,” said Ed Moya, senior market analyst at Oanda. “So far earnings season and inflation expectations support the idea that the Fed will have to continue tightening until they send the economy into a recession.”

Though oil has eased, key timespreads are indicating scarce supply in the market. Diesel, used by truck and shippers to transport goods, has surged at a time when inflation is already running high. The International Energy Agency has warned that the OPEC+ cuts could tip the global economy into recession, and the U.S. has rebuked Saudi Arabia for the decision. President Joe Biden said he’d announce new actions next week to combat high U.S. gasoline prices.

“After last week’s run up, it feels like oil prices have been plagued with a sell-the-news trade this week,” said Stacey Morris, head of energy research at VettaFi. “Recession concerns and the related demand impact are going to remain in focus now that there is a little more clarity on supply following the OPEC+ meeting.”

Prices:

- WTI for November delivery fell US$3.50 to settle at US$85.61 a barrel in New York.

- Brent for December dropped US$2.94 at US$91.63 a barrel.

There are signs that trading activity is picking up after months in the doldrums. Brent open interest climbed to its highest level since March this week, while there has also been a flurry of bullish option flows and the start of Mexico’s secretive annual oil hedge.