Jan 27, 2022

Oil rally pauses as risk-off sentiment drags broader markets

, Bloomberg News

We are in a global oil supply deficit that will get worse before it gets better: Global energy economist

VIDEO SIGN OUT

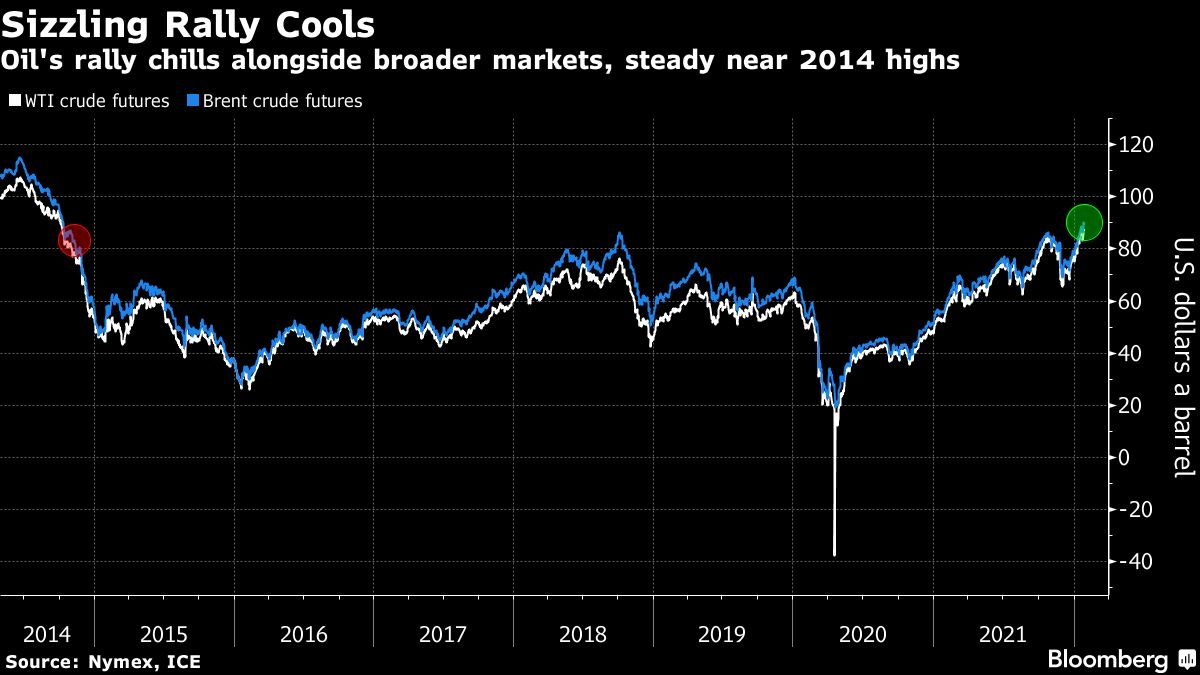

Oil fell from a fresh seven-year high as equities wavered and the dollar’s strength weighed on the commodity.

Futures in New York slipped 0.9 per cent. Oil has rallied most of this week with physical supplies appearing extremely tight. Key swaps tied to the North Sea market are trading at their firmest since 2019, while timespreads are trading at their strongest level since November. Despite the underlying strength, the market wasn’t immune to the whipsaw movements buffeting most major assets.

“This afternoon’s oil weakness was primarily a function of a soaring U.S. dollar that the oil market could no longer ignore,” said Ryan Fitzmaurice, a commodities strategist at Rabobank. But as it stands, fundamentals in oil balances are tight, so even a small escalation in the Ukraine/Russia conflict could result in an oil supply shock for Europe, he added.

Traders are tracking events in Ukraine on concern that Russia may launch an invasion after massing thousands of troops on the border, potentially disrupting energy supplies. Moscow has denied it plans to invade, but Citigroup Inc. said a rise in crude volatility is a sign that the market is pricing in an increased political risk premium, potentially of at least US$5 a barrel.

Oil has rallied in the opening weeks of 2022 on the continued recovery in energy consumption from the ravages of the coronavirus pandemic. With global demand coming in stronger than expected and growing concerns about how much further producers will ramp up output, stockpiles at some key hubs have been waning early in the year. The rally in crude prices is coming as the global economy contends with rampant inflation.

Meanwhile, inventories at the key U.S. storage hub at Cushing fell again last week to hit the lowest level for this time of year in a decade. At the same time weekly oil product consumption is at its highest level for the time of year in at least 30 years, driven in part by a spate of cold weather in the U.S.

Prices

- WTI for March delivery fell 74 cents to settle at US$86.61 a barrel in New York

- Brent for March settlement dipped 62 cents to US$89.34 a barrel

As supplies remain constrained, market participants will focus their attention on the OPEC+ meeting set for next week. The coalition, which includes Russia, will get a chance to weigh in next week when they meet Feb. 2. The Organization of Petroleum Exporting Countries and its allies will probably rubber-stamp a hike of 400,000 barrels a day for March, according to delegates.

“OPEC+ underperformance and inaction support elevated oil prices as the group has underdelivered against its stated production targets by hundreds of thousands of barrels and has committed to a passive role in the conversation despite external pressure, primarily from the U.S., to increase production and ease fuel prices,” said Louise Dickson, senior oil markets analyst at Rystad Energy.

Related coverage:

- U.S. natural gas futures suddenly spiked the most on record Thursday afternoon, a sharp move that could be a sign of bearish wagers being squeezed out of the market.

- U.S. shale executives have finally achieved something that eluded the industry for more than a decade: the ability to turn over billions of dollars in dividends to shareholders while at the same time boosting production to tap into surging global oil demand.

- A slump in global diesel stockpiles has left the market vulnerable to price spikes. In Europe, the continent’s largest oil refinery is starting work that will curb its output. At the same time, U.S. refiners are prioritizing making gasoline, further eroding supply. And in Asia, China has cut its fuel export quota.