May 15, 2023

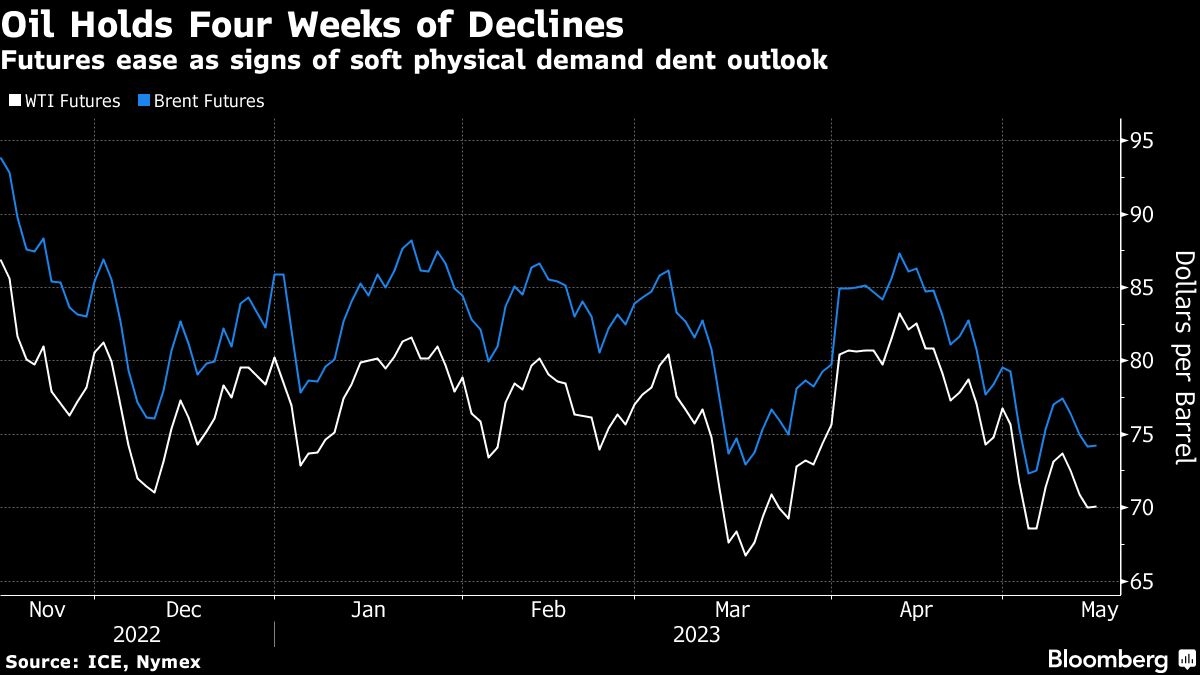

Oil holds fourth weekly decline as concerns over demand linger

, Bloomberg News

Global energy prices may struggle but Canadian oil will do well: Energy strategist

VIDEO SIGN OUT

Oil held a fourth weekly drop as concerns over the U.S. economy and China's slower-than-expected recovery weighed on the outlook.

West Texas Intermediate futures traded near US$70 a barrel after the longest run of weekly losses since September. Negotiations are continuing to avert a US default related to the debt ceiling, with Treasury Secretary Janet Yellen warning that the department could run out of money as soon as June 1.

Oil is down 13 per cent for the year as fears over a possible U.S. recession outweigh supply cuts pledged by OPEC+. Demand for physical barrels also appears weak, while refinery margins — the profits that refiners make from processing crude into petroleum products like diesel and gasoline — remain low.

Hedge funds and money managers have amassed the largest short position in global benchmark Brent since July 2021, although speculators are less bearish on U.S. crude. Investors will be watching key economic data from China this week for clues on the pace of the nation's recovery, as well as a monthly report from the International Energy Agency due Tuesday.

“Sentiment in the oil market remains negative with an uncertain demand outlook and concerns over the U.S. debt ceiling,” said Warren Patterson, head of commodities strategy for ING Groep NV. “The market will likely be looking out for any potential demand revisions in the IEA's monthly market report.”

Prices:

- WTI for June delivery was steady at US$69.97 a barrel at 7:35 a.m. in London.

- Futures dipped by as much as 0.9 per cent earlier.

- Brent for July settlement dipped 0.1 per cent at US$74.06 a barrel.