Jun 7, 2023

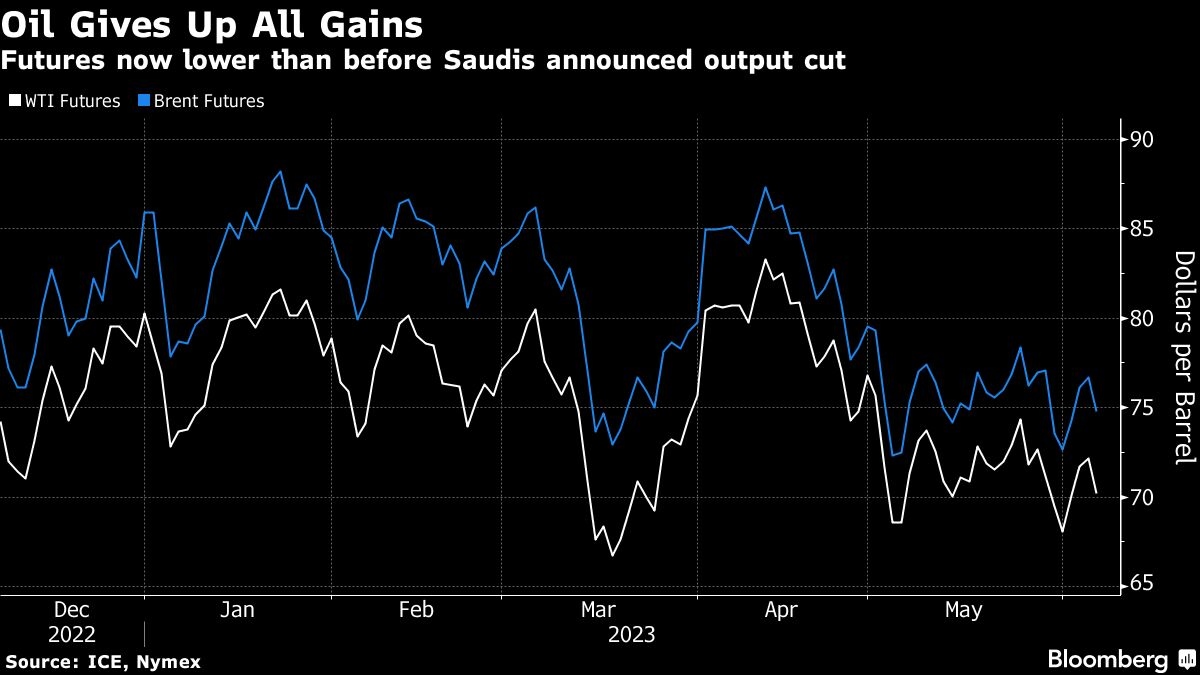

Oil erases all gains that followed Saudi-led production cut

, Bloomberg News

Russia is the wild card keeping oil prices down: Portfolio manager Jack Janasiewicz

VIDEO SIGN OUT

Oil erased all the gains that followed Saudi Arabia's surprise weekend pledge for extra supply cuts.

West Texas Intermediate dipped below US$71 a barrel on Tuesday, down by about US$1 from Friday's close. The drop comes after Monday's short-lived surge following the tense OPEC+ meeting and Saudi announcement. The kingdom also raised its crude prices for July.

Saudi Arabia pledged to do “whatever is necessary” to stabilize the market with concerns over the demand outlook, especially from China, weighing on prices in recent weeks. Oil tumbled 11 per cent last month, in part due to resilient Russian output, despite the OPEC+ producer saying earlier this year it would reduce supply.

“The Saudis undoubtedly believed a unilateral cut of one million would give prices a boost,” said Ole Hansen, head of commodity strategy at Saxo Bank A/S. “The 10 per cent production cut would need an US$8 higher price to keep revenues stable, and that is clearly not happening. But considering the higher fuel burn inside the kingdom during the next couple of months, exports will be lower.”

Saudi Arabia followed its move to cut output in July with an increase to its crude prices for the same month. That's pushing some Asian refiners to consider buying more crude from other suppliers including Russia.

WTI oil prices have also fallen further down the futures curve, with prices for December 2023 and 2024 lower than Friday's close.

“Demand is looking weaker and non-OPEC supply stronger by year-end than many analysts had forecast,” Citigroup Inc. analysts said in a note. The bank's view is now “even more bearish demand for 2H '23 than it was at the start of the year. This is particularly true for China, and not only in oil but across commodities.”

Prices:

- WTI for July delivery fell two per cent to US$70.73 a barrel as of 11:16 a.m. in London.

- Brent for August settlement slipped 1.9 per cent to US$75.27 a barrel.