Paul Gardner, partner and portfolio manager at Avenue Investment Management

Focus: REITS, bonds and dividend stocks

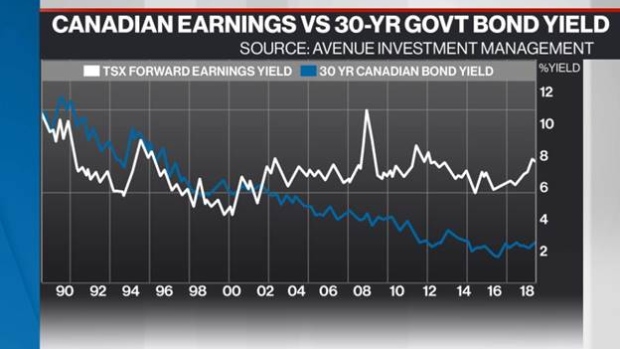

MARKET OUTLOOK

The U.S. stock market finally has corrected with all other global markets. Along with the U.S., the Canadian market is down as well. Avenue believes that the Canadian stock market is too cheap. It now trades at the low of a historical range. At a 14 times price-to-earnings, there’s opportunity for the Canadian market to outperform over the medium term. Instead of waiting for this to happen, the best way of capturing this anomaly or opportunity is to capture yield from sectors such as utilities, energy, real estate and telecom. Many of these sectors give us a rich yield of over 5 per cent. When you target these sectors or companies, the stock market doesn’t have to do much to get an acceptable 8 per cent rate of return over next few years. There is a bigger risk of a “melt-up” then a meltdown in the Canadian markets.

The bond market is more complicated. Even though there are fears of higher anticipated inflation, we don’t believe inflation will cross above 3 per cent. The Bank of Canada will give us a few more rate hikes, but overall the bond market has adjusted to slightly higher bond rates. There seems to be a “buyers’ strike” in the U.S. due to trade wars with countries that purchase billions of U.S. Treasuries. Over next few years, the market is going to have to deal with increased supply of 10- and 30-year Treasuries in the U.S. Because of large deficits in American and small deficits in Canada, U.S. rates (especially in the long end) will widen further from a lower Canadian interest rate bond curve.

TOP PICKS

WPT INDUSTRIAL REIT (WIR_u.TO)

This U.S.-focused REIT trades on the TSX. Its main assets are industrial ones in secondary American cities; its main clients are logistic companies. The new move in retail with online favours and doesn’t distract from their assets. It now trades at a 15 per cent discount to its net asset value (NAV). Recent announcements to internalize their management structure and their new relationship with a few large Canadian pension plans allows the company to be totally aligned themselves with unit holders.

YELLOW PAGES (Y.TO) CONVERTIBLE 8% 2022 BONDS

Yield is now at 9 per cent. This story is all about free cash flow and aggressive debt repayment. The new management has focused on not only its digital business, but more importantly its capital structure. The company’s outstanding debt has reduced materially. These outstanding bonds might be the only debt outstanding in a few years. The debt is mispriced for the risk taken.

BCE (BCE.TO)

Bell’s yield is close to 6 per cent. Avenue believes that Bell is the best-in-class of all the telecom plays. Even though competition is fierce in its space, we believe their “fibre to the home” solution is almost completed. Due to this, it will be able to win against the competition. Its free cash flow yield is 8 per cent. Their media assets are strong and, with interest rates settling down, we believe the sector and specifically Bell will outperform the markets over the next two years.

| DISCLOSURE | PERSONAL | FAMILY | PORTFOLIO/FUND |

|---|---|---|---|

| WIR-U | Y | Y | Y |

| Y 2022 | Y | Y | Y |

| BCE | Y | Y | Y |

PAST PICKS: SEP. 13, 2017

ALTAGAS (ALA.TO)

- Then: $27.59

- Now: $15.98

- Return: -42%

- Total return: -36%

BAYTEX (BTE.TO) 6.625% 2021

- Total return: 8%

TD BANK (TD.TO)

- Then: $67.07

- Now: $71.04

- Return: 6%

- Total return: 11%

Total return average: -6%

| DISCLOSURE | PERSONAL | FAMILY | PORTFOLIO/FUND |

|---|---|---|---|

| ALA | Y | Y | Y |

| BTE 2021 | Y | Y | Y |

| TD | Y | Y | Y |

FUND PROFILE

Avenue Equity Portfolio

Performance as of: Oct. 31, 2018

- 1 month: -0.7% fund, -0.9% index

- 1 year: 5.0% fund, 5.4% index

- 3 years: 8.8% fund, 9.5% index

INDEX: TSX.

Based on reinvested dividends.

WEBSITE: avenueinvestment.com

Advertisement