Oct 6, 2017

Personal Investor: Have you outgrown your mutual funds?

By Dale Jackson

Most Canadians save for retirement through mutual funds. It’s not the ideal way to grow your money but for investors with modest savings who want professional management and diversification, it’s one of the few alternatives.

Fees are based on the amount invested. Some can be higher than 2.5 per cent each year. That’s $500 for a meagre $20,000 but that fee balloons to $5,000 when the portfolio grows to $200,000 and $12,500 on $500,000. That’s money that could be growing over time.

In addition, mutual funds are generic. They don’t consider your personal goals, risk tolerance or time to retirement.

As your savings grow, so do your options. Unsurprisingly, the best financial advice in this world goes to those with the most money. A smaller portion of a bigger portfolio can be well worth their while. Many high-net worth advisors who work on flat fees, commissions, hourly rates or a mix, can keep fees low.

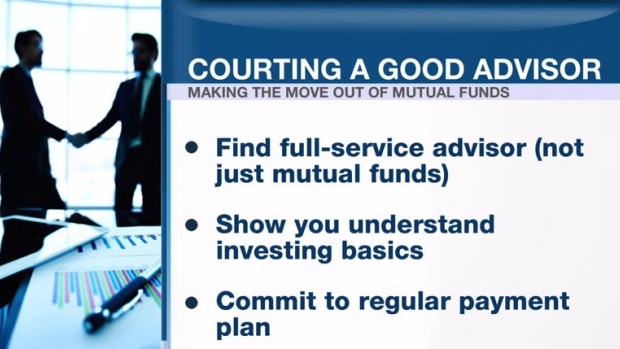

Here are three tips on how modest-net worth mutual fund investors can get the attention of good advisors:

- Be sure your advisor is full-service and not restricted to mutual funds. A full-service advisor can help determine when and how to move into direct investments.

- Understand the basics of investing and show a willingness to learn. Time is money and an advisor needs to know you understand the strategy and risks involved.

- Commit to a regular contribution plan. Nothing says you’re in it for the long run like cold, hard cash on a regular basis. While you may be low-net worth now, a good advisor will recognize high-net worth potential.