Sep 6, 2017

Personal Investor: RESPs are a smart way to save for college or university

By Dale Jackson

Here’s a sobering lesson for students attending college and university this fall. According to the Government of Canada, the average cost of a four-year program has risen to $66,000. That includes tuition, books, supplies, student fees, transportation, food & housing and other expenses.

It’s no wonder young Canadians are carrying record student debt just as they begin their adult lives.

Post-secondary school costs are expected to keep rising, but there is a federal government program that can help relieve the financial burden when their children go off to school.

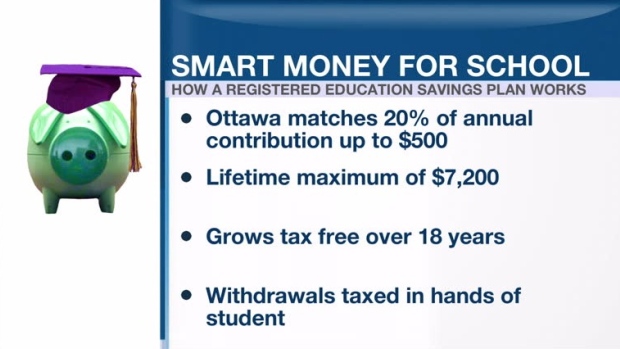

The registered education savings plan, or RESP, matches the annual contributions of one parent by 20 per cent up to $500, to a lifetime maximum of $7,200.

To maximize the full government grant, the parent needs to cough up an average of $2,500 each year.

Unlike registered retirement savings plans (RRSPs), which have decades to grow, RESPs only have an 18-year time horizon (or less). That means the money in the plan needs to be invested for a shorter period of time, to be withdrawn over a short period of time. There are investment products that suit RESPs, so it might be best to speak with a qualified advisor.

The contributions and grants grow tax-free while in the RESP, but unlike an RRSP they can’t be deducted against the parent’s income. Instead, it is taxed when withdrawn in the hands of the low-income student.

If a child decides not to continue after high school or if too much money is accumulated, you will have to pay tax on the money earned in the plan as interest. This money is called "accumulated income". It will be taxed at the parent’s regular income tax level, plus an additional 20 per cent.

The money that the parent puts into the RESP is returned.

The Canada Education Savings Grant can be shared with a brother or sister if they have grant room available -otherwise, the grant must be returned to the Government of Canada.

There is a lifetime limit of $50,000 for each child. It may not cover the total cost of a decent education, but it’s a good start.