Apr 21, 2022

Powell hardens hawkish pivot toward half-point Fed rate hikes

, Bloomberg News

It looks like we might be getting to peak inflation: Strategist

VIDEO SIGN OUT

Federal Reserve Chair Jerome Powell outlined his most aggressive approach to taming inflation to date, potentially endorsing two or more half percentage-point interest-rate increases while describing the labor market as overheated.

“I would say that 50 basis points will be on the table for the May meeting,” Powell said at an IMF-hosted panel on Thursday in Washington that he shared with European Central Bank President Christine Lagarde and other officials. He said demand for workers is “too hot -- you know, it is unsustainably hot.”

The Fed chief is taking direct aim at strong demand that the central bank wants to cool. It’s a strategy that bears considerable risk for U.S. workers and the economy’s overall growth prospects in months ahead, as well as for the Fed itself in a year of midterm congressional elections, with inflation a major concern among ordinary Americans.

“This is going to be a very close call on whether we get a recession or not,” said Ethan Harris, head of global economics at Bank of America Securities. “They have to get monetary policy into tight territory, and they probably need to get some kind of rise in the unemployment rate.”

Powell also reinforced expectations for another half-point increase in June, by citing minutes from last month’s policy meeting that said many officials had noted “one or more” 50 basis-point hikes could be appropriate to curb the hottest inflation in four decades.

“There’s something in the idea of front-end loading” moves if appropriate, Powell said -- “so that points in the direction of 50 basis points being on the table.”

Investors are betting on half-point increases in May, June and possibly July. Rising yields in turn have unsettled the stock market, with the S&P 500 Index closing down 1.5 per cent Thursday.

Powell’s St. Louis Fed colleague James Bullard has also opened a debate about doing a more aggressive 75 basis-point increase if needed. Even normally dovish officials like San Francisco’s Mary Daly have said that a “couple” of half-point moves are likely, though she sounded wary of a larger move.

“The tactics about is it 50, is it 25, is it 75, those are things I’ll deliberate with my colleagues,” she said in an interview with Yahoo! Finance on Thursday. “But my own starting point is we don’t want to go so quickly or so abruptly that we surprise Americans and make them have to adjust quickly.”

Powell “approved a 50 basis point hike in May, but I think June is also there and maybe even more,” said Yelena Shulyatyeva, senior U.S. economist for Bloomberg Economics.

To some, it’s too little, too late. Critics say that U.S. central bankers are caught in a policy bind of their own making. Prices began to accelerate in the fourth quarter, when employers shrugged at the latest wave of the coronavirus and added more than a half-million workers each month.

Wage gains picked up and demand strengthened, broadening inflation pressures throughout the economy even as the Fed continued to add stimulus by holding rates near zero and buying bonds.

Policymakers last year wanted to avoid pre-emptive tightening, but the combination of fiscal stimulus, monetary support, and bounce-back in demand put them behind inflation pressures that were well underway.

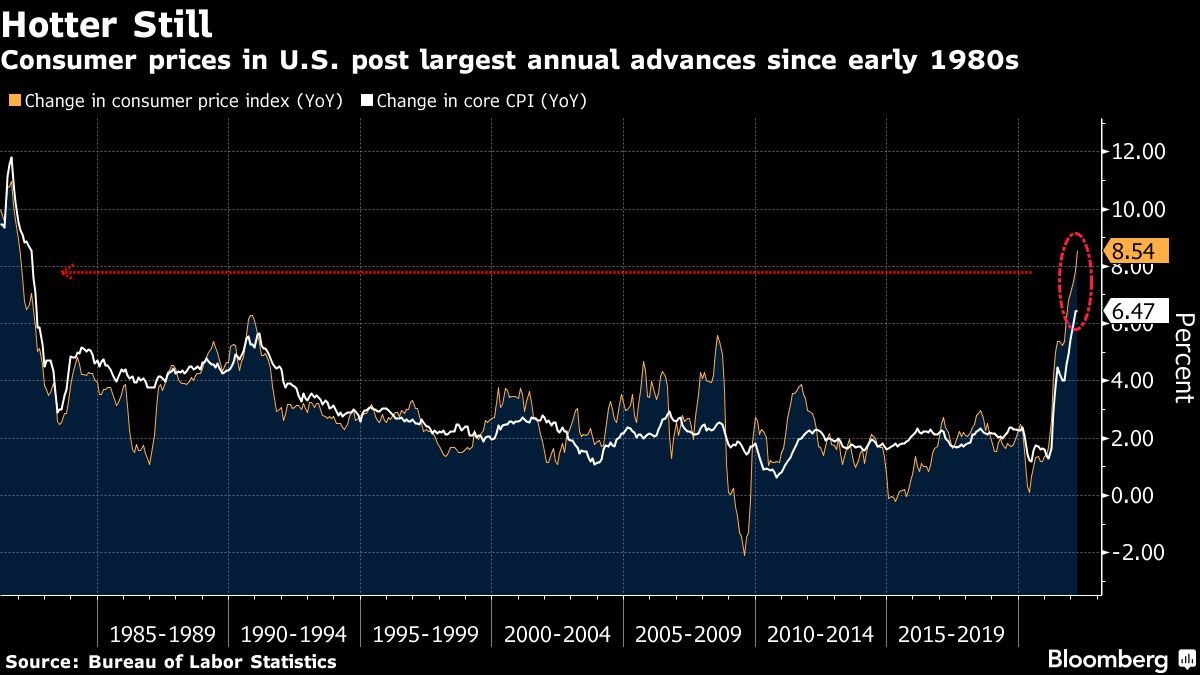

The consumer price index rose 8.5 per cent in March from a year earlier, the most since 1981; the Fed’s target is based on a separate measure known as the personal consumption expenditures price index, which rose 6.4 per cent for the year through February. Russia’s invasion of Ukraine will likely raise food and energy prices further.

CATCH UP

Now, Fed officials are scrambling to get interest rates back up to a level that doesn’t add further stimulus, and possibly push forward into restrictive territory. Powell said the Fed will no longer forecast relief from goods prices and improving supply chains, which could be an acknowledgment that pressures have also disbursed into service prices as well.

“I just don’t understand why they did this,” Harris said. “They had many chances to take the off-ramp and they never did.”

Another uncertainty in policy strategy is what happens to financial conditions when officials start running assets off their balance sheet. Fed officials have signaled this process will be announced in May, with the runoff stepping up to US$95 billion a month combined for Treasuries and mortgage-backed securities.

Shulyatyeva said there is no reliable estimate about how much tightening the runoff will add.

“They want to believe they can achieve a soft landing,” said Shulyatyeva. “It will be extremely difficult to do. Monetary policy is a very blunt tool.”