Jul 25, 2022

Q2 earnings growth expectations ok, but breadth of earnings is weak: Larry Berman

By Larry Berman

Larry Berman's Educational Segment

VIDEO SIGN OUT

The headline number is very misleading. It makes it look like all is fine. A peak inside suggests that the data is still very skewed from COVID impacts to sectors. Sectors that were boosted by massive stimulus now gone, and sectors that are reopening versus a year ago. If we exclude the 243.7 per cent earnings per share (EPS) gain in the energy sector that represents only 4.11 per cent of the S&P 500, overall earnings are down 3.22 per cent.

Excluding the 10.7 per cent financials EPS is growing at 12.67 per cent and excluding the biggest sector weight of 27.6 per cent in technology, EPS are up only 6.41 per cent. Retail stocks have seen earnings fall almost 33 per cent with most financials like banks (-26 per cent) and insurance (-30 per cent) weighing the most. Industrials got a big boost from transports (re-opening) by 129 per cent. Within technology, the consumer sensitive hardware sector is down 11 per cent while productivity enhancing software (6.4 per cent) and semiconductors (10.9 per cent) have good gains.

The following table was compiled by Bloomberg Intelligence after earnings on July 22:

Reported/Estimates 106/393

Forecast EPS($)** 56.03

- S&P 500 Index 5.53%

- S&P 500 Ex-Financials 12.67%

- S&P 500 Ex-Energy -3.22%

- S&P 500 Ex-Technology 6.41%

Sector year-over-year

- Consumer Discretionary -9.4%

- Consumer Staples -1.0%

- Energy 243.7%

- Financials -23.8%

- Real Estate 9.0%

- Health Care 2.1%

- Industrials 26.3%

- Information Technology 2.2%

- Materials 13.0%

- Communication Services -7.2%

- Utilities -3.4%

When we look at the headline chart on forward based EPS the trend looks fine. Keep in mind, sector numbers can be very seasonal, especially retailers, so it’s not as dire as it looks, but the breadth trends are weak. The nominal economy (before inflation) is growing at double digits, so revenues are high while companies are doing good so far managing costs.

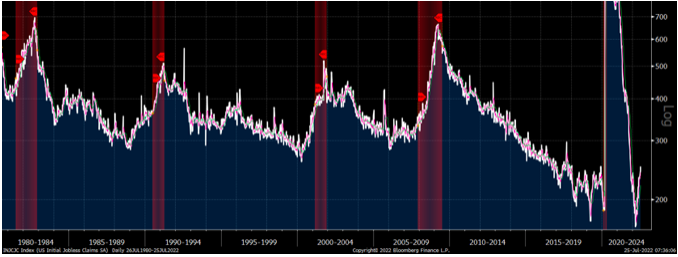

The next leg of cost reductions are jobs and we are starting to see companies talk about freezing hiring plans. The weekly unemployment claims are ticking higher, but with the four week average under 250,000, it is in moderate economic expansion ranges. If it were to rise in the coming month towards 300,000, that would translate into overall job losses for the economy and confirm a full-on NABE recession call is coming. The chart shows weekly jobless claims. In past recessions (excluding the COVID shock), we need to see the turn higher from 300,000 or more weekly claims to begin to see net job losses. Given that the size of the labor force is significantly higher today (158 million) than in past decades (100 million in 1980), we could argue that number may be higher today. We need to see more cyclical layoffs to have a material downtick in the economy than the supply side inventory issues that are currently causing two quarters of negative GDP. On Thursday this week we will see the first estimate of Q2 GDP and it will be weak but expected to still be positive. It’s consumption that makes up 70 per cent of the economy. While we are hearing that consumers are substituting for lower quality goods with consumer confidence running at multi-decade lows, they are still working.

I’m not saying the economy is strong by any stretch, but when we look at earnings and what supports markets, jobs are a major driver. For the markets to take another notch lower, Main Street needs to be in a recession. This view does support the notion that the demand side of inflation drivers may have peaked and monetary policy will not fix the supply side issues. Inflation has likely peaked, but may not cool as much as some have hoped. This week’s FOMC will likely deliver a 75 basis point rate hike with one or more 50 bps hikes before we see a pause. The late August Jackson Hole conference may be the point where the FOMC hints at a pause in rate hikes. It’s all data dependent.

Follow Larry online:

Twitter: @LarryBermanETF

YouTube: Larry Berman Official

LinkedIn Group: ETF Capital Management

Facebook: ETF Capital Management

Web: www.etfcm.com