The dollar-funding squeeze, which rocked short-term interest rate markets this week, may deepen further with the end of the quarter approaching.

Banks are just about to start their usual pattern of cutting back on providing liquidity to close books and meet regulatory requirements. And next week, there’s another round of Treasury auctions that could leave markets net short of another US$45 billion in cash.

That may explain why stress is showing up in bill sales and currency markets even after the Federal Reserve conducted three overnight repurchase operations, with a fourth to come on Friday, to ease a liquidity shortage.

Thursday’s Treasury bill sale flopped as investors demanded extra yield to be rewarded for tying up cash. The securities slid ahead of the sale and the average yield was awarded five basis points higher than pre-auction indicated.

Meanwhile, the costs of borrowing dollars in funding markets is still elevated. In currency swap markets, handing over yen in return for dollars for one week -- a time period which covers the crucial month end -- now costs you the equivalent of 2.4 per cent on an annualized basis. It was just 0.2 per cent a week ago.

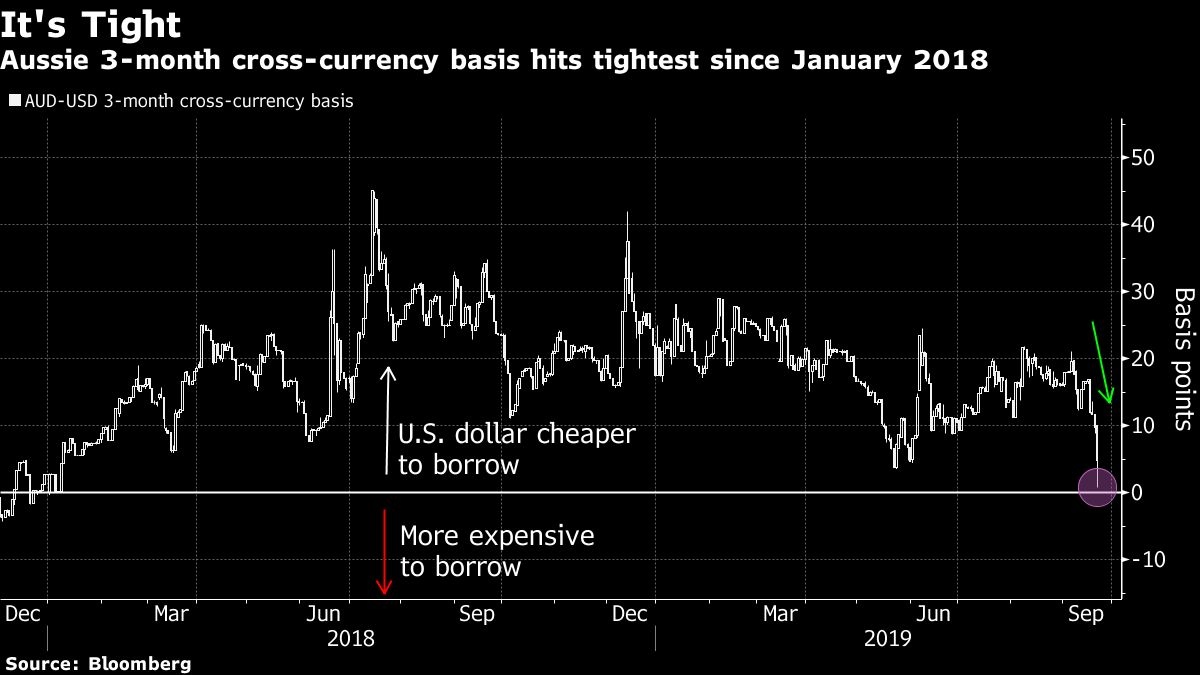

The same is true in cross-currency basis -- where banks and financial institutions can swap floating-rate payments in different currencies -- with the premium for the Australian dollar over its U.S. counterpart collapsing by the most in eight years during Asian trading hours on Friday.

Finally, the spread between U.S. Treasuries and interest rate swaps reached a record low Wednesday. That’s an indication that traders are getting anxious about what level they can finance borrowing bonds, and are starting to use swaps instead.

“With balance sheet constraints unaddressed, and possibly intensifying into year-end, we expect little relief for front-end swap spread,” Barclays Plc strategist Amrut Nashikkar wrote in a client note. Investors can expect swap spreads to remain under pressure, particularly further along the curve, which are more susceptible to limited balance-sheet capacity, he added.

Advertisement