Ryan Bushell, President of Newhaven Asset Management

Focus: Canadian dividend stocks

MARKET OUTLOOK

A strong first quarter has seemingly washed away the sour stretch of investment performance from the end of last year. Portfolios have recovered to levels near the all-time highs seen last August and the pressing question is: What’s next?

Last quarter I wrote that the average market performance in the year following a down year was a 17 per cent move higher. I had expected a rebound in 2019, given that the selling in the fourth quarter seemed indiscriminate and driven as much by the calendar as anything else. But even with that in mind, the pace of the recovery so far has been stunning. We were able to use weakness in the weeks that straddled the holidays to rebalance existing portfolios and get new cash invested, with excellent results so far.

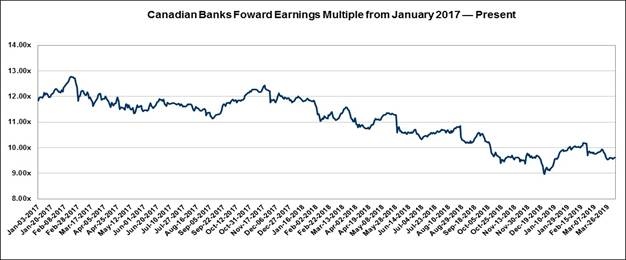

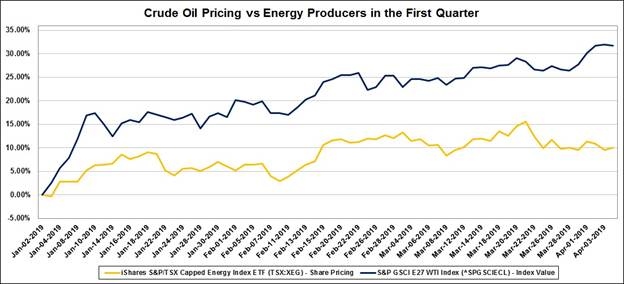

I still feel the Canadian market and our portfolios have room to run, based on two charts:

Above you can see that over the past nine quarters the price-to-earnings ratios of the Canadian banks have been going steadily down. This means that increasing earnings within the banks over the past few years have not been reflected with corresponding share price appreciation. Below you can see the massive increase in oil prices during the first quarter was not fully reflected in the share prices of the oil producers.

These two sectors make up about one-third of both the market and our portfolios. I’m optimistic that these areas can push returns higher over the next nine months, barring an unexpected macroeconomic shock. Regardless, the portfolio will churn out another 3 per cent gain in dividends alone before the end of the year, which is reason enough to remain patiently invested.

Looking beyond 2019, things are murky. We could try to get out of the market before a recession and get back in immediately after, but predicting recessions is a notoriously fruitless task and the opportunity cost of missed dividends and market returns is too great to hold cash that earns relatively little. Instead, we’ll abstain from the frothy areas of the market, continue to own companies with dividends that are sustainable through a recession and be ready to put capital to work in strong businesses that get unfairly punished when the next storm comes.

TOP PICKS

TD BANK (TD.TO)

Most recently purchased at $75.

It’s hard to believe that TD shares are only up about 3 per cent in a year where earnings grew substantially and the economy remains strong. While I think fears about Canadian consumer credit are overblown, TD Bank has the least exposure to that line of business among the banks if one’s worried about it. It doesn’t even trade at its normal historical premium. We continue to add full positions in TD for all new clients with long-term dividend growth all but assured.

ARC RESOURCES (ARX.TO)

Most recently purchased at $8.50.

The discount for Canadian oil and gas stocks remains attractive in my opinion. ARC is a conservatively-run producer with a diversified asset base that includes significant vertical integration. At share price and commodity price levels, ARC yields nearly 7 per cent and still generates significant free cash. I have a ton of confidence this management team, whom I met with recently, will capitalize on emerging opportunities in Western Canada for natural gas feedstock including LNG Canada, petro-chemicals and LPG exports alongside their already robust and diversified marketing capabilities. Collecting 7 per cent while we wait is the result of the company being removed from the TSX 60. Their production mix of natural gas, natural gas liquids and light oil is not well understood in my opinion.

NFI GROUP (NFI.TO)

Most recently purchased at $33.50.

NFI Group is the newest holding to my portfolio after dropping nearly 50 per cent in the latter half of 2018. I have been watching NFI for some time and have been impressed by their management team. The market became very enamoured with the company in the last few years, but the shifting economic tides last fall caused a precipitous decline that is overdone in my view. The company now trades at about 10-times earnings and 5 per cent dividend yield following a 13-per-cent increase with Q4 results. There is some economic sensitivity to their business to be sure, however public transit agencies facing growing population and little political will to develop transit infrastructure continue to turn to buses to fill the gaps. Additionally, many of these purchasers are looking to lower emissions and renewing their fleet with zero emission or hybrid solutions, which apply well to the structured routes that buses take. Finally the company is growing its parts and service business, which should offset some of the more cyclical aspects of their business, as these run counter-cyclically with new orders while broadly growing market share. Broader markets have recovered to new highs while this company remains near its lows.

| DISCLOSURE | PERSONAL | FAMILY | PORTFOLIO/FUND |

|---|---|---|---|

| TD | Y | Y | Y |

| ARX | Y | Y | Y |

| NFI | Y | Y | Y |

PAST PICKS: MAY 7, 2018

WPT INDUSTRIAL REIT (WIR_u.TO)

- Then: $13.25

- Now: $13.82

- Return: 4%

- Total return: 10%

ALTAGAS (ALA.TO)

- Then: $25.01

- Now: $17.71

- Return: -29%

- Total return: -23%

TD BANK (TD.TO)

- Then: $73.35

- Now: $76.35

- Return: 4%

- Total return: 8%

Total return average: -2%

| DISCLOSURE | PERSONAL | FAMILY | PORTFOLIO/FUND |

|---|---|---|---|

| WIR_U | Y | Y | Y |

| ALA | Y | Y | Y |

| TD | Y | Y | Y |

WEBSITE: newhavenam.com

Advertisement