Ryan Bushell, president of Newhaven Asset Management

Focus: Canadian dividend-paying stocks

_______________________________________________________________

MARKET OUTLOOK

Canadian dividend stocks are out of favour, especially those deemed to be sensitive to interest rates.

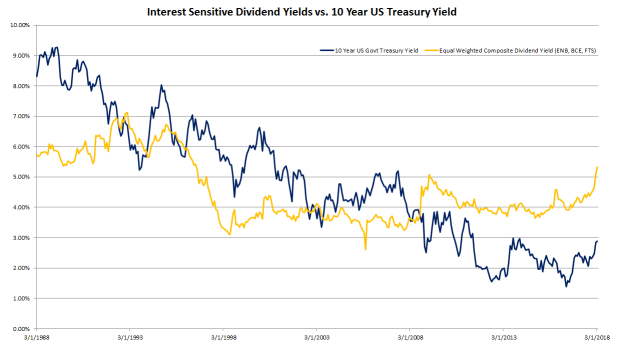

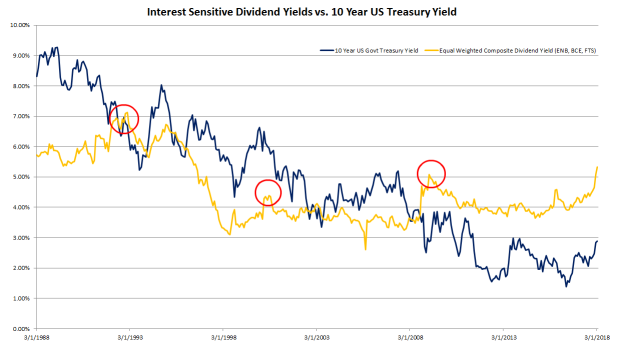

The chart above depicts a three-decade period for the dividend yield of three Canadian bellwether dividend stocks relative to the yield on 10-year U.S. Treasury Bonds. The equally weighted group of Enbridge,Fortis and BCE is currently yielding over 5 per cent for the first time since the financial crisis in 2008. They're yielding nearly 2.5 per cent more than U.S. 10-year government bonds, which is an all-time high. You might think that there must be something wrong with their businesses, but each company is seeing acceleration in their respective business fundamentals, and all three companies just raised dividends by an average of 6.5 per cent. So what gives? I believe there are three main reasons for the recent weakness:

1. Market sentiment is against them

Investors are once again shunning tangible cash flows and dividends in favour of potential cash flows in companies that have little (if any) earnings and pay no dividends. Amazon, Tesla, Snapchat, marijuana, cryptocurrency/blockchain … We said we would never again repeat the late '90s, but here we are.

2. Interest rates are rising — for real this time

The rise in interest rates from all-time lows reached in the summer of 2017 has been dramatic and, with the global economy accelerating, uncertainty surrounding trade and already low unemployment, the potential for inflation is greater than at any point in the last decade. But there's context necessary here. The last time 10-year bond yields rose to 3 per cent, the yield on the above basket of stocks was around 4 per cent. The last time these stocks yielded 5.3 per cent, 10-year bond rates were 7 per cent. Sure, rates are rising, but how far? The middle of the baby boom generation just turned 64, meaning they're just retiring or newly retired and will continue to be a deflationary force to be reckoned with for some time yet. We're nine years into this economic expansion, input costs and interest rates are rising while the U.S. dollar is falling. The next recession is coming and what happens to rates then?

3. The war on … Trade?

NAFTA could be dissolved at any moment. Canada and the u.s. have the largest “free” trade relationship in the world. The Canadian dollar unexpectedly rallied nearly 10 per cent last summer to more than US$0.80. If I'm an international investor, why would I put capital to work in Canada, even with compelling valuations, when the currency could fall out of bed at any moment? Not to mention fears about an extended Canadian consumer, oil prices and our own political and taxation issues. This last point is hurting all Canadian stocks, even our financial and energy companies that should be benefitting from these late cycle conditions.

So what are we to do as Canadian dividend investors: Give up? Move on? Stay the course?

First some context:

Over the last 20 years, the TSX has returned 6.5 per cent/year on a total return basis. The S&P 500 has returned 6.3 per cent in Canadian dollars, yet it is now trading at nearly a 50 per cent book value premium to the TSX, with about 30 per cent in technology.

Looking at the chart again, the last three times the average yield on Fortis-Enbridge-BCE peaked out (January 1993, August 2000, March 2009) their returns the next five years were compelling both on an absolute and relative basis:

| 5 YEAR TOTAL RETURN (ANNUALIZED) | |||

|---|---|---|---|

| START DATE | ENB/FTS/BCE (EQUAL WEIGHT) | TSX COMPOSITE | S&P 500 (CAD) |

| JANUARY 1993 | 30.20% | 17.80% | 23.70% |

| AUGUST 2000 | 16.20% | 0.70% | -6.80% |

| MARCH 2009 | 18.90% | 13.70% | 18.00% |

| AVERAGE | 21.77% | 10.73% | 11.63% |

We know what the last five years have looked like, but what matters today is the next five. Being a successful long-term investor is less about what you do when times are good and more about remaining disciplined at all points during the cycle and having the conviction to buy and hold quality companies when others are selling or ignoring them.

TOP PICKS

CANADIAN NATURAL RESOURCES (CNQ.TO)

Most recent purchase at $38.80.

Oil prices remain above $60, the Canadian dollar is falling and CNQ recently reported very solid 2017 results and raised their dividend (for the 18th consecutive year) by 22 per cent.The share price is the same as it was in June 2016 when the oil price was $50. The dividend yield is now up to 3.3 per cent and the fundamentals for the oil price continue to strengthen. Inventories are approaching five-year averages (Cushing storage has been cut in half) and have not built much so far in 2018 despite elevated refinery maintenance. OPEC has committed to over-tightening the market vs. exiting from quotas too early while compliance remains high. U.S. production continues to grow but so do exports, which indicate strong global demand. Longer-term pipeline egress is on the horizon and CNQ also includes a very inexpensive option on LNG development off the west coast of Canada as the country's largest natural gas producer.

ENBRIDGE (ENB.TO)

Most recent purchase at $40.50.

The performance of this company over the past three months has been shocking to me. As mentioned earlier interest rates are up, but not nearly enough to justify this type of pessimism. If the market is worried about Enbridge’s ability to fund their capital program or pay down debt or their dividend, they should look no further than their ability to sell more than $1 billion in common shares last fall in a private placement to only three investors. Additionally, the company has earmarked more than $10 billion in saleable assets, which the market is clearly ignoring at a time where there are record-high amounts of private equity/pension money looking for stable cash flowing assets. Bottom line: this company has guided to a minimum 10 per cent dividend growth through 2022. At current share price levels, you're basically locking in a 9.7 per cent yield in a company that has never cut its dividend and posted an 11 per cent compound annual total return since the '50s. This is what compounding is all about.

AUTOCANADA (ACQ.TO)

Most recent purchase at $20.

AutoCanada has been very quiet over the past couple of years just going about their business of adding a few dealerships a year to diversify their formerly Alberta-centric business. They now have a much more balanced dealership mix (60 per cent domestic/40 per cent import) and less than half of their dealerships are now in Alberta. I’m not much for technical analysis, but this stock has built a huge (two-year) base and there is good support here at $20. The company reports on Friday and I'm expecting a decent end to 2017 and reasonably confident 2018 guidance.

| DISCLOSURE | PERSONAL | FAMILY | PORTFOLIO/FUND |

|---|---|---|---|

| CNQ | Y | Y | Y |

| ENB | Y | Y | Y |

| ACQ | Y | Y | Y |

PAST PICKS: JUNE 27, 2017

ENBRIDGE (ENB.TO)

- Then: $52.75

- Now: $41.42

- Return: -21.46%

- Total return: -18.16%

VERMILION ENERGY (VET.TO)

I believe the path for oil prices look bright as we move past the current refinery maintenance season. Demand is strong and inventories are starting the summer drawdown season close to five-year averages. China and India are importing significantly more oil after changes to Chinese import restrictions to independent refiners and India's recovery following a currency circulation issue that held back economic growth and commerce. Vermillion is an international producer with primary exposure to higher Brent-based oil and European natural gas pricing. They just raised their dividend 7 per cent and the shares yield more than 6 per cent. The shares are even more attractive than when I recommended them last June, with the oil price significantly higher. Sentiment will turn at some point.

- Then: $42.05

- Now: $40.32

- Return: -4.11%

- Total return: 0.24%

TD BANK (TD.TO)

A wonderful buying opportunity opened up in Canadian bank stocks early last summer following the Home Capital fallout and subsequent rescue by none other than Warren Buffett, leading to outsized returns for the remainder of the year. The Canadian banks remain cheap, as share prices are only begrudgingly responding to earnings and dividend growth. I considered recommending a bank again, but think you may get a better shot at them during a broader market correction at some point this summer.

- Then: $65.26

- Now: $75.68

- Return: 15.96%

- Total return: 18.98%

Total return average: 0.35%

| DISCLOSURE | FAMILY | PERSONAL | PORTFOLIO/FUND |

|---|---|---|---|

| ENB | Y | Y | Y |

| VET | Y | Y | Y |

| TD | Y | Y | Y |

WEBSITE: www.newhavenam.com

LINKEDIN: Ryan Bushell

Advertisement