Oct 23, 2019

Snap gains as analysts see proof of turnaround in user growth

, Bloomberg News

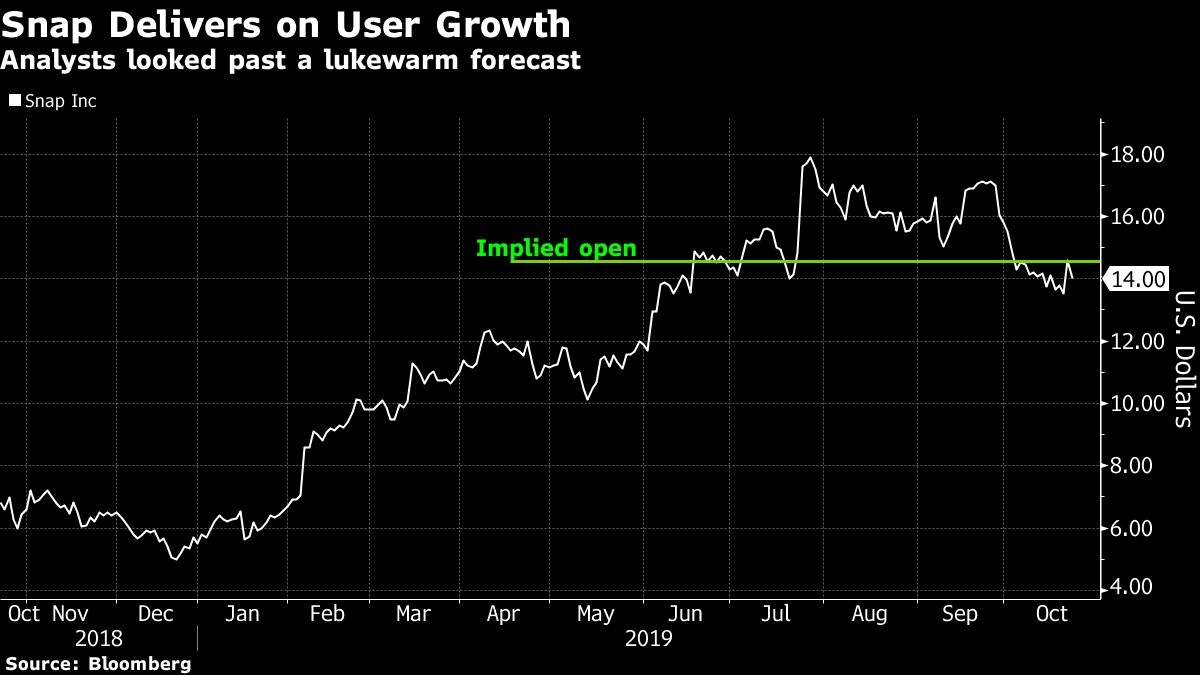

Snap Inc. shares rose in pre-market trading on Wednesday, reversing an early decline after the Snapchat parent company reported third-quarter results that analysts said underlined its 2019 turnaround story.

The quarter was seen as validating the optimism that had been growing in the lead-up to the report. Jefferies wrote that the results show that Snap is “not a one-hit wonder,” while the upward trend in daily active users “shows the growth is sustainable.”

The results were not wholly positive for the social-media company. The revenue outlook was seen as light, although many analysts noted Snap’s history of being conservative with forecasts. Many firms also expressed valuation concerns after a 180-per-cent rally in the stock off a December low, leading to some trimmed price targets.

Shares gained 3.9 per cent before the bell, though the stock’s initial reaction to the report had been negative. The stock is down more than 20 per cent from a recent peak, based on its Tuesday close, though it remains a strong year-to-date outperformer.

Here’s what analysts are saying about the results:

JPMorgan, Doug Anmuth

Upgrades to overweight from neutral; price target raised to US$20 from US$17.

“Snap’s platform and business have both improved dramatically over the past several quarters,” based on revenue growth and user trends, and this quarter “showed more encouraging trends.”

The stock is “at an inflection point” with Ebitda, and shares look “increasingly compelling” after recent weakness.

Morgan Stanley, Brian Nowak

The results “underscore the company’s better execution” this year.

Looking into 2020, Snap needs to show “more consistent” growth in daily active users and engagement, as well as improved ad tools. Recent successes reflect “a period of low-hanging fruit” in terms of its improvements, and “we look for more ad unit/targeting innovation to continue to move SNAP into the ‘must buy and highly measurable’ category.”

Equal-weight rating, US$17 price target.

Nomura Instinet, Mark Kelley

In terms of adjusted Ebitda, the outlook “calls for break-even to a positive [US]$20mn to exit the year, accomplishing the stretch goal to achieve break-even in 2019.”

Raises Ebitda expectations for 2019 and 2020, and lifts price target to US$16 from US$15. Neutral rating.

UBS, Eric Sheridan

The results showed “solid operating progress,” but continued forward execution is needed.

Neutral rating, US$16 price target.

Jefferies, Brent Thill

The results show that Snap is “not a one-hit wonder,” and the trends in daily active users “shows the growth is sustainable.”

While the revenue outlook was slightly below expectations, “we assume conservatism given SNAP has beaten the high end of guidance” in the past.

“Fundamentally positive” on the stock, “but would wait for a pullback to get constructive.”

Hold rating, PT lowered to US$17 from US$18.

Susquehanna Financial Group, Shyam Patil

The company “continues to progress on its turnaround,” as seen by the “strong” results and the “generally solid” outlook, which looks “fine” as Snap is typically conservative.

Affirms neutral rating and trims price target to US$16 from US$18 “as the tempered outlook warrants a slightly reduced multiple.”

Loop Capital Markets, Alan Gould

The guidance suggests “slightly less robust growth in the current quarter,” although Snap’s outlooks have been conservative in the past.

Snap “should continue to benefit from the unduplicated reach it provides marketers in the core younger demos and advertisers’ desire to help build competition for the dominant internet platforms.”

The company “is growing nicely” and it should see positive free cash flow next year, but valuation is a concern at current levels.

Hold rating, US$15 price target.

What Bloomberg Intelligence Says:

The outlook “raises concerns about the longevity of Snap’s story,” but sales have the “room to outgrow” the weak guidance. Improved ad pricing and higher engagement can help lift Snap’s average revenue per user, but it “needs to continue to deliver user growth to instill confidence in longer-term expectations.” —Analyst Jitendra Waral