There are seven types of inflation and three major drivers.

Demand-pull inflation occurs when the demand of a good or service exceeds supply. Demand-pull happened during the early days of COVID-19 as governments doled out money to everyone. As the economy recovered back to full employment, demand has remained high relative to supply.

Cost-push inflation is generally driven from increased costs of production from materials and labour. Cost-push also happened during the pandemic and was exacerbated by the Russia-Ukraine war.

Both of these factors can lead to built-in inflation, which is where labour sees rising prices and demands higher wages. This is the wage price spiral economists talk about. This was a big part of the 1970s inflation and what the central banks want to make sure does not happen today. Let’s look at the different ways central banks are measuring inflation today and figure out if they can generate a soft/no landing scenario markets have celebrated in the past few months.

TRIMMED MEAN INFLATION

One way is to look at what is called a trimmed mean. What is the median good or service price doing? This does not count the extreme moves in the more volatile priced items and looks at the middle. The chart shows the percentage of costs rising between three to five per cent and five to 10 per cent versus the categories of below three per cent and above 10 per cent. The median are the prices rising about 2.5 per cent to 8.7 per cent (see the expanded table below.) What the trend shows over the past year is that the median costs categories (orange and dark blue) are growing. More categories of prices are rising at a higher than desired level.

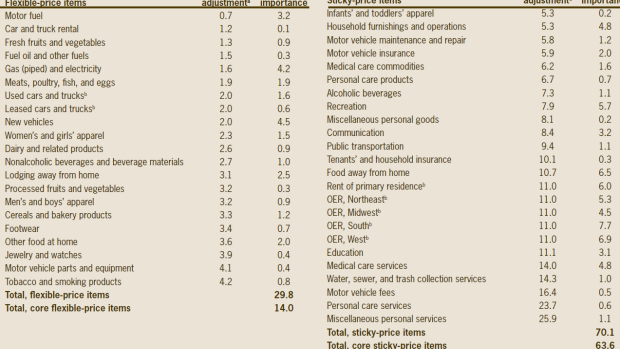

STICKY INFLATION

When will Apple have to drop prices of their smart phones to compete? If you can answer that question, you can have a sense of where we are going with the idea of sticky inflation. How about Coke and Pepsi weekly supermarket battles. I’m seeing significantly less of them these days and prices are rising for both. The table below looks at the categories of goods and services and breaks them down into flexible and sticky. Items like rents and tuition change annually on average, where the price of motor fuel and fresh fruits and vegetables changes much more frequently.

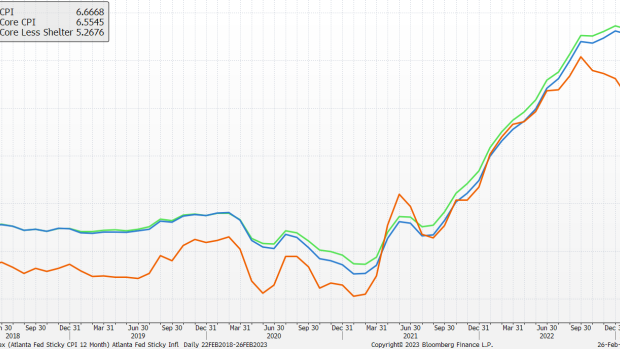

Each month when the U.S. Bureau of Labor Statistics releases the CPI report, the Atlanta Fed calculates the sticky inflation baskets. We can see that prices are generally staying higher for longer, although most may know that the housing cost adjustments are lagging. The good news here is that more supply is coming and this should help lower rental prices. We can see that sticky core less shelter has been coming down for several months. U.S. Federal Reserve Chair Jerome Powell highlighted this a few months ago in a speech and is likely a major catalyst for the market recovery in the past few months. And while it has come down, it is still higher than the Fed Funds rate. In theory, history shows that overnight rates need to be higher than inflation to be restrictive.

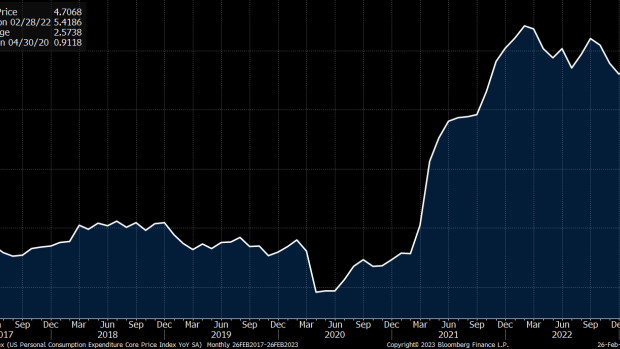

Core PCE Inflation Personal Consumption Expenditures Price Index, Excluding Food and Energy | U.S. Bureau of Economic Analysis (BEA)

The core PCE excludes food and energy, and as in the example above, of the two main volatile prices groups, commodity-based prices move more frequently. So this is a similar view, but a slightly different look versus the sticky inflation basket. The core PCE surprised markets last week by rising when it was expected to decline and was a negative for asset prices.

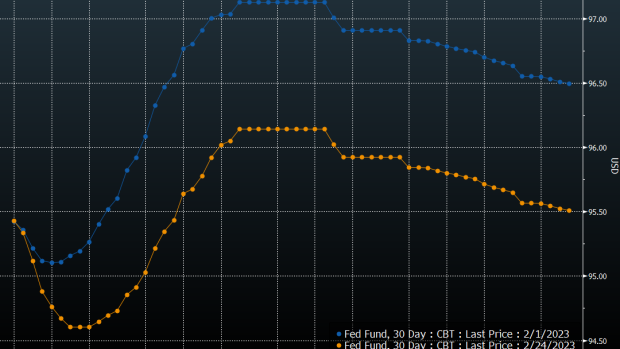

Since the last Federal Open Market Committee (FOMC) meeting on Feb 1, most FOMC members, have reiterated the higher for longer message. This has moved the terminal rate for Fed Funds from 4.90 per cent in June to 5.40 per cent in October. The market is still pricing in an easing cycle in 2024, but the terminal rate is almost 100 basis points higher.

Central banks want to avoid the shift to a 1970s like built-in inflation phase (wage price spiral) at any cost. The hotter the labour market remains, the more wage demands will be a factor, the more we have to worry about inflation being sticky.

The higher for longer message the FOMC and other central banks are trying to drill home makes the hope for a soft landing a lower probability and the odds of a harder landing more likely. Investors should expect the FOMC to be more restrictive until (as they reiterate) inflation comes back down to their 2 per cent target. From our lens, that only happens with notable weakness in the labour markets, which remains elusive. Historically, when we start to see the unemployment rate move up, a recession is a virtual certainty. Until then, expect inflation to remain built-in and sticky and asset markets to be more volatile.

Follow Larry online:

Twitter: @LarryBermanETF

YouTube: Larry Berman Official

LinkedIn Group: ETF Capital Management

Facebook: ETF Capital Management

Web: www.etfcm.com

Advertisement