Wall Street bears battered by the Reddit crowd earlier this year have yet to regain their gumption, even with stocks at records and valuations near two-decade highs.

The median short interest in members of the S&P 500 sits at just 1.6 per cent of market value, near a 17-year low, according to Goldman Sachs Group Inc. In Europe, a short-covering frenzy has sent bearish bets collapsing like never before in Morgan Stanley data.

At the same time, hedge-fund longs are around the highest relative levels in years at JPMorgan Chase & Co.’s prime brokerage.

They’re all signs of the bullish mania propelling global equities to fresh records this month, thanks to the economic re-opening and big policy stimulus. The smart money has little appetite to wager against either expensive or deadbeat companies -- especially after being lashed by the day-trader army earlier this year.

“There’s just mass euphoria,” said Benn Dunn, president of Alpha Theory Advisors. “No one wants to get their head ripped off by a short anymore.”

The easing of lockdowns and vaccine rollout have driven a risk-on rotation in favor of what was once the least popular equities -- low-quality and value shares. Hedge funds in both the U.S. and Europe have rushed to cover their shorts, with little appetite to add fresh bearish wagers on the newly underperforming parts of the market like growth equities.

Elevated valuations would seem to provide ammo for short sellers. The S&P 500 is trading at around 23 times next year’s earnings, near the highest since 2000. Compared with the 10-year Treasury yield, the benchmark is offering the thinnest risk premium since 2010.

But bearish bets are proving painful. A Goldman Sachs basket of the most-shorted stocks has surged three times as much as the broader U.S. market in 2021, partly because a horde of Robinhood traders stampeded into a few short targets last quarter.

No wonder so many investors have given up. According to a survey by the National Association of Active Investment Managers, the most-bearish group that typically holds a net-short position has actually stayed long or at least neutral in 21 of the past 25 weeks. That’s a bullish stretch not seen since 2018.

“This is a long-only type market based on the overwhelming fundamental story,” said Phil Camporeale, portfolio manager in multi-asset solutions for JPMorgan Asset Management.

At the same time, equity positioning has just reached a fresh all-time high among discretionary investors, according to Deutsche Bank AG.

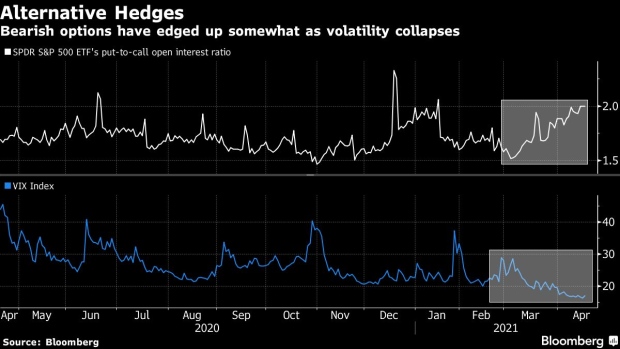

That’s not to say investors aren’t adding downside protection, they’re just choosing to do it in the options market. Bearish contracts on the S&P 500 and its biggest exchange-traded tracker have increased relative to bullish ones in the past month.

Still, muted costs for volatility contracts suggest optimism is still largely the name of the trading game.

For example, long positioning relative to shorts among JPMorgan’s hedge-fund clients has only been higher 7 per cent of the time since January 2018. In Europe, as the Stoxx 600 has rallied to records, shorts on its constituents have vanished to 1.65 per cent of free float, near a record low, according to Morgan Stanley.

“Short selling of what were historically the ‘go-to’ shorts has slowed dramatically and not been replaced by ‘new’ shorts,” the team led by Mathieu Renault wrote in a note.

Advertisement