Jun 21, 2022

Stocks surge after US$2T wipeout; Bonds fall

, Bloomberg News

Peak in interest rates are in, pivot to long duration assets: James Thorne

VIDEO SIGN OUT

US equities rebounded Tuesday after last week’s rout erased nearly US$2 trillion from the S&P 500. Treasuries retreated.

The S&P 500 added 2.4 per cent, led by energy and consumer discretionary shares, while the tech-heavy Nasdaq 100 surged 2.5 per cent following the long weekend. Revlon Inc. gained 62 per cent in the wake of its Chapter 11 bankruptcy filing, Kellogg Co. was up 2.0 per cent after plans to separate into three companies, and a basket of the most-shorted stocks rose 2.7 per cent. The drop in Treasuries took the benchmark 10-year yield back to 3.3 per cent.

Sentiment this week is being helped by comments from President Joe Biden that a US recession isn’t “inevitable,” but the outlook remains parlous for investors weighing whether the market has bottomed. History suggests bear markets usually take time to find a floor, especially when they are accompanied by a recession, as happened in 2008’s financial crisis. Richmond Federal Reserve President Thomas Barkin said the US central bank should raise interest rates as fast as feasible in order to quell rampant inflation.

“We could likely skirt recession, almost touch it but not quite, because we think that the Federal Reserve has become much more sensitive to the effects of their actions on the economy, both in terms of employment and in terms of stability,” John Stoltzfus, chief investment strategist at Oppenheimer, said in an interview. “We’re not out of the woods yet, but we think we’re walking in the right direction.”

After unexpectedly accelerating to a fresh 40-year high in May, US consumer price growth is seen slowing, with a Bloomberg survey of economists predicting 6.5 per cent by the fourth quarter and to 3.5 per cent by the middle of next year.

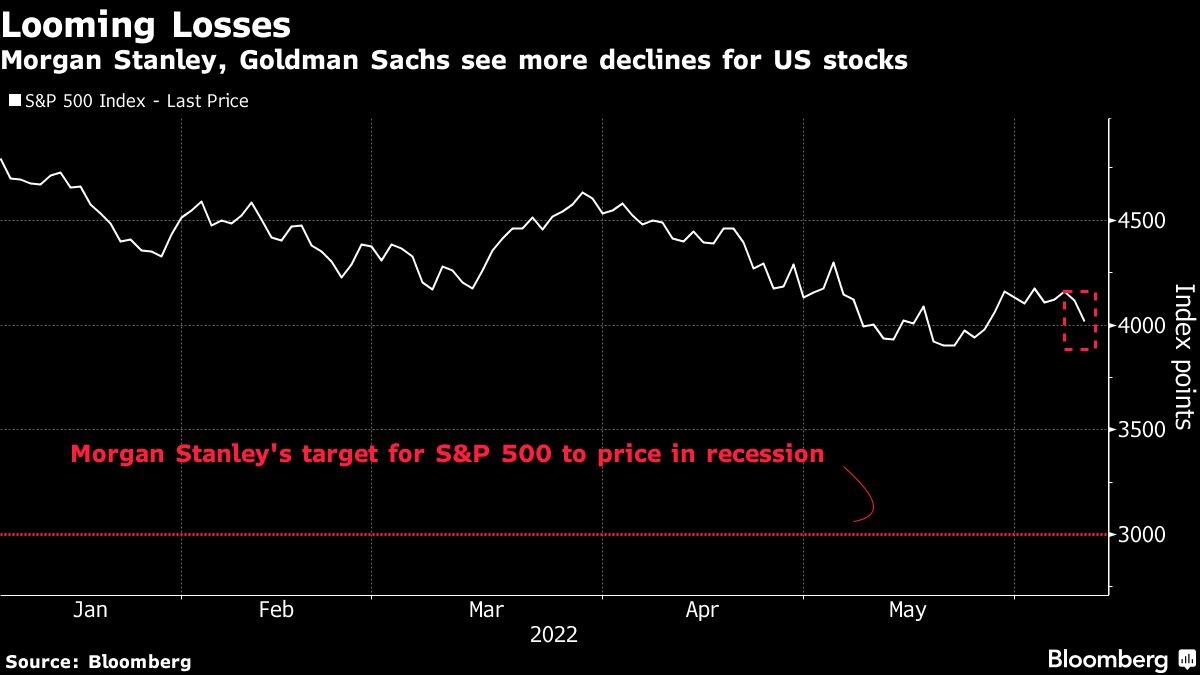

Yet fears are increasing that Fed policy makers intent on cooling price pressures will go too far and trigger an economic slowdown. Strategists at Morgan Stanley and Goldman Sachs Group Inc. warned equities may have further to fall to fully price in the risk of recession, reflecting wider skepticism about Tuesday’s rebound.

“Central banks are facing a growth-inflation trade-off. Hiking interest rates too much risks triggering a recession, while not tightening enough risks causing unanchored inflation expectations,” strategists at BlackRock Investment Institute including Jean Boivin said in a note. “It’s tough to see a perfect outcome.”

Crude oil gained. Bitcoin scaled US$20,000 as cryptocurrencies got a reprieve from recent turbulence. The dollar was little changed and the yen hovered near a 24-year low, sapped by the contrast between a super-dovish Bank of Japan and a hawkish Fed.

European stocks gained for a second day, with chemicals and automakers leading the advance in the benchmark Stoxx 600 Index.

What to watch this week:

- Fed Chair Jerome Powell semi-annual Senate testimony, Wednesday

- Bank of Japan April minutes, Wednesday

- Powell US House testimony, Thursday

- US initial jobless claims, Thursday

- PMIs for Eurozone, France, Germany, UK, Australia, Thursday

- ECB economic bulletin, Thursday

- US University of Michigan consumer sentiment, Friday

- RBA’s Lowe speaks on panel, Friday

Some of the main moves in markets:

Stocks

- The S&P 500 rose 2.4 per cent as of 4:02 p.m. New York time

- The Nasdaq 100 rose 2.5 per cent

- The Dow Jones Industrial Average rose 2.2 per cent

- The MSCI World index rose 1.8 per cent

Currencies

- The Bloomberg Dollar Spot Index was little changed

- The euro rose 0.2 per cent to US$1.0529

- The British pound rose 0.1 per cent to US$1.2267

- The Japanese yen fell 1.2 per cent to 136.67 per dollar

Bonds

- The yield on 10-year Treasuries advanced eight basis points to 3.30 per cent

- Germany’s 10-year yield advanced two basis points to 1.77 per cent

- Britain’s 10-year yield advanced five basis points to 2.65 per cent

Commodities

- West Texas Intermediate crude rose 1 per cent to US$110.65 a barrel

- Gold futures fell 0.4 per cent to US$1,832.50 an ounce