The U.S. Federal Reserve has a big conflict.

The monetary policy goals of the U.S. Federal Reserve are to foster economic conditions that achieve both stable prices and maximum sustainable employment. Given the insolvency of Silicon Valley Bank (SVB) and the risk to financial conditions, the Federal Open Market Committee should probably pause their rate hikes and possibly cut rates.

This would likely complicate their ability to fight inflation. At least this was the historical playbook. It would be very difficult to achieve everything.

Unfortunately, we think this makes a harder landing and stagflationary scenario far more likely. We note some economists are already calling for a Fed pause in rate hikes. The short end of the curve has mostly priced out additional rate hikes this year and more aggressive easing beginning later this year. So much for the higher for longer message Powell delivered to Congress last week.

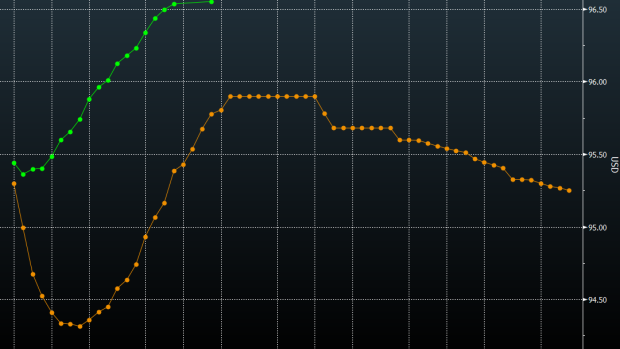

Fed Fund Futures Curve March 13 8:45am vs. Post Powell Congressional Testimony March 8th

By the time we go to air at 4:30 p.m. EDT on March 13, we will probably know most of the policy resolution/plan for SVB and markets will either be calm or more anxious looking for the next domino.

It’s clear to us that the FOMC mandate likely needs to change and the Federal Deposit Insurance Corporation program support needs some modernization. Like we saw in 2001 and 2009, these changes take time for Congress to act.

Dodd-Frank was not implemented until 2010, a full year after the markets bottomed. We will likely see some additional stopgap measures to reduce systemic contagion immediately. This could help for a few days or weeks, but like during COVID, the market did not stabilize until we saw the massive support programs from the lender of last resort.

To be sure, SVB was a unique situation. The ratio of uninsured deposits (97.3 per cent) were so far off what any other bank averages (45 per cent). From everything we have read, we do not think SVB has systemic risk to banking, but it did to the depositors. And that’s the key here. You need to know your cash is safe.

It was a modern day run on the bank seemingly co-ordinated via Silicon Valley’s own social media channels. When confidence shakes, Wall Street always shoots first and asks questions later. They are shooting any bank that has similar risks to assets as SVB and Signature Bank.

Larger banks are under some stress too. The emergency program implemented is called Bank Term Funding Program (BTFP) should help mitigate the short-term depositor risks, but more programs could be needed. In the GFC, a program like the Temporary Liquidity Guarantee Program was very successful.

KRE is the regional bank ETF in the U.S. There are no pure U.S. regional bank ETFs in Canada, but there are U.S. bank ETF exposures. Looking back to before the GFC, we see value building below US$40 and at $30 it’s exceptional for a longer-term position. We do not see this as similar risks to the GFC, so unlikely to see much lower extremes. Not for the faint of heart to be sure, but this is where I’m looking to add some exposure. These levels are all subject to revision as the situation develops.

In Canada, the ZEB equal weight bank ETF should fall in sympathy with the U.S. led stress. For us, we are looking below $30 to add exposure. We have not liked the valuation at all over the past year and have had very little direct exposure.

We have been critical of NIRP, ZIRP, QE and uncontrollable deficit spending policies since the GFC. COVID clearly accelerated the need for extraordinary measures. But as we have seen, since the first Fed put was implemented after Long-Term Capital Management in 1998, the system can handle these extraordinary polices well, but that they have always led to unintended consequences.

New challenges are addressed, and the can is kicked once again. The political will to fix the long-term insolvency of entitlements is close to nil. We will see this political malignancy magnified as the U.S. debt ceiling debate rages in the coming months. Printing money has been the easy way out. It’s important to understand the central bank role as the lender of last resort.

It’s a key function of a fractional reserve system along with oversight and regulation. There was a clear miss here from that perspective. Who owns that?

Now, with sticky inflation risks building, the out cards are harder to play. The central bank conundrum gets increasingly more difficult. This too shall pass, but each time it gets a bit more difficult for all the central bank horses and all the government’s men to put Humpty together again..

Follow Larry online:

Twitter: @LarryBermanETF

YouTube: Larry Berman Official

LinkedIn Group: ETF Capital Management

Facebook: ETF Capital Management

Web: www.etfcm.com

Advertisement