Sep 12, 2019

U.S. recession indicators flash mixed signals as talk heats up

, Bloomberg News

Eisman Questions Whether Global Industrial Slowdown Becomes Recession

VIDEO SIGN OUT

Investors are abuzz over the risk of a looming U.S. recession, yet economic indicators are giving mixed signals at worst that the record-long expansion will end soon.

Yes, manufacturing is slumping, uncertainty is mounting globally and businesses are paring spending as global demand slows and the U.S.-China trade war rages. But unemployment near a five-decade low is buoying consumers, stock prices remain elevated and the Federal Reserve is already cutting interest rates, with further reductions expected.

Economists surveyed by Bloomberg reckon there’s a 35 per cent chance of a recession in the next 12 months, up from 15 per cent a year earlier, based on median estimates. Even if the economy skirts a downturn, growth is still expected to slow, which will have implications for President Donald Trump’s re-election chances in 2020.

“I don’t see any indication right now that a recession is imminent,” said Ben Herzon, an economist at Macroeconomic Advisers by IHS Markit. “There are definitely areas of concern.”

Even so, it may be too late once these indicators begin to decline. It’s partly what makes recessions so hard to predict -- even after they’ve already begun.

Here is a selection of key indicators to monitor along with what color -- green, yellow or red -- each gauge is flashing now:

Jobless Claims (Green)

One of the most closely-watched recession indicators, initial jobless claims have yet to show signs of deteriorating. They show how many Americans are applying to receive unemployment benefits and a sustained pickup suggests companies are boosting layoffs. Still, claims have often leveled off before surging -- a period we might be in now.

Consumer Spending (Green)

Consumption makes up more than two-thirds of the economy, and the latest gross domestic product data underscore how Americans are driving the expansion. Retail sales offer a timely snapshot of spending each month and a sustained downward trend would signal consumers are pulling back, and economic growth may ultimately falter. While things look good for now, figures due Friday are projected to show cooler gains in August.

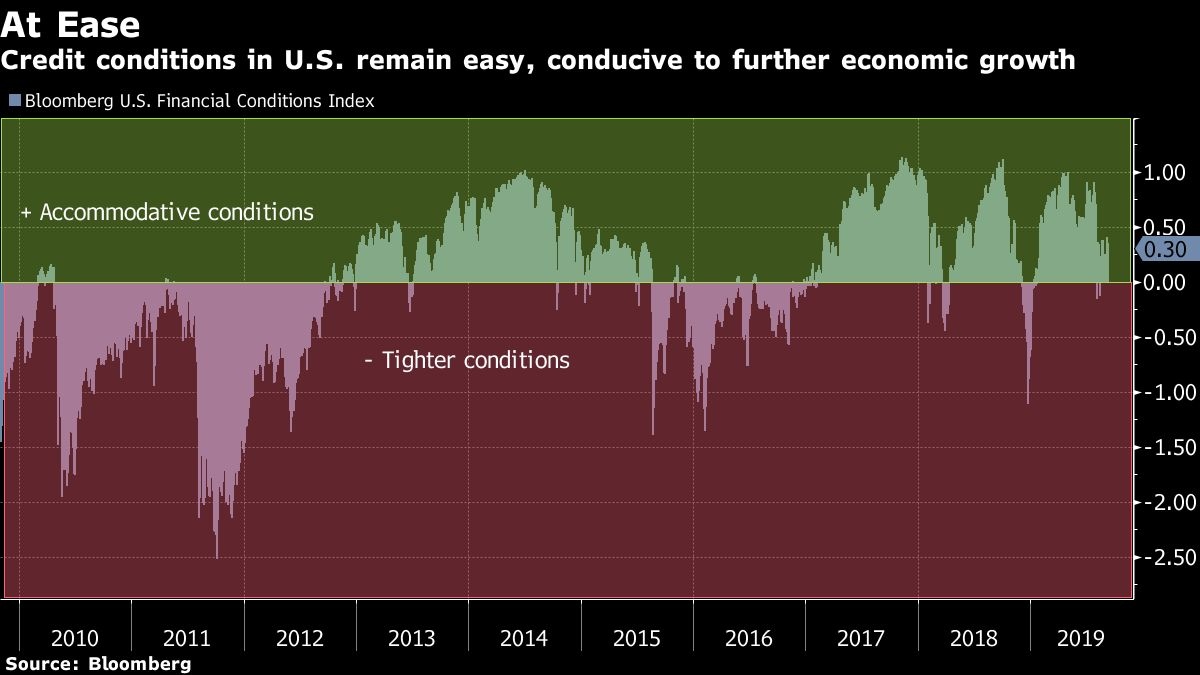

Credit Conditions (Green)

A significant tightening in credit conditions can also prelude a recession as banks tighten the spigot in the face of increasing risks. This can be especially challenging for small and medium-sized businesses in need of capital. A Bloomberg gauge shows conditions remain favourable.

Average Weekly Hours (Green)

This measure faltered in July, with hours in manufacturing falling to the lowest level since 2011 before August data showed a rebound at factories and overall. A sustained downward trend would suggest layoffs are around the corner. “The first order from companies when faced with an economic shock or potential downturn is to cut hours worked,” said Michelle Meyer, head of U.S. economics at Bank of America Corp.

Housing Market (Yellow)

Housing is a leading indicator in some respects: Americans have to feel comfortable enough in their future financial situation to commit to a mortgage and builders have to feel the outlook is bright enough to construct residences. While sales have stagnated and single-family home permits have cooled since early 2018, the sector’s implications for the economy have become trickier to read -- thanks to a shortage of affordable properties and challenges for developers to profit from lower-priced homes.

Yield Curve (Yellow-Red)

When the rates on short-term Treasury securities are higher than those for long-term securities -- known as an “inverted” curve -- it could spell trouble. The spread between three-month and 10-year securities has been inverted for much of the past four months, and such a trend has preceded each of the last seven recessions. Still, the indicator has a history of predicting downturns with long and variable lags, and there’s a case that it’s a less reliable signal than in the past.

Manufacturing (Yellow-Red)

The Fed’s measure of factory output contracted in the first two quarters of 2019, fitting the technical definition of recession. In addition, the Institute for Supply Management’s purchasing managers’ index showed the sector contracted in August for the first time since 2016, while industry job gains have sharply cooled. Manufacturing makes up only about 11% of the economy but there’s that weakness will spread more broadly into services, and ultimately to jobs and consumer spending.

Equipment Orders (Yellow)

A related measure, U.S. factory orders for business equipment -- or bookings for non-military capital goods excluding aircraft -- has been cooling since the end of 2017. Former Pacific Investment Management Co. chief economist Paul McCulley viewed this as a leading indicator. Weakness preceded the last recession, though a downturn didn’t follow poor orders throughout the 2010s.

Profit Margins (Yellow-Red)

Stephen Gallagher, chief U.S. economist at Societe Generale SA, has been looking to the trend in corporate profit margins. One gauge of those, seen below, has declined to levels not reached since the U.S. was emerging from the last recession.

“They’re getting squeezed," Gallagher said of companies. “When they’re experiencing very thin margins, their anticipations on profitability begin shrinking and they -- as a result -- tend to cut back or scale back their plans for investment, scale back their plans for hiring.”

--With assistance from Vince Golle.