U.S. stocks posted their biggest four-day rally since November 2020 as dip buying in battered technology shares continued Wednesday.

The S&P 500 gained 0.9 per cent while the tech-heavy Nasdaq 100 added 0.8 per cent with Alphabet Inc. and Advanced Micro Devices Inc. higher after strong results. However, the rally may not last. In late trading, Meta Platforms plunged more than 20 per cent after the Facebook parent reported disappointing results. A rout of that magnitude would wipe out almost US$150 billion in market share from the company. Meanwhile, the biggest exchange-traded fund that tracks the Nasdaq 100 tumbled 1.7 per cent after rallying 8 per cent in the prior four sessions. Spotify Technology SA also sank almost 20 per cent on its results.

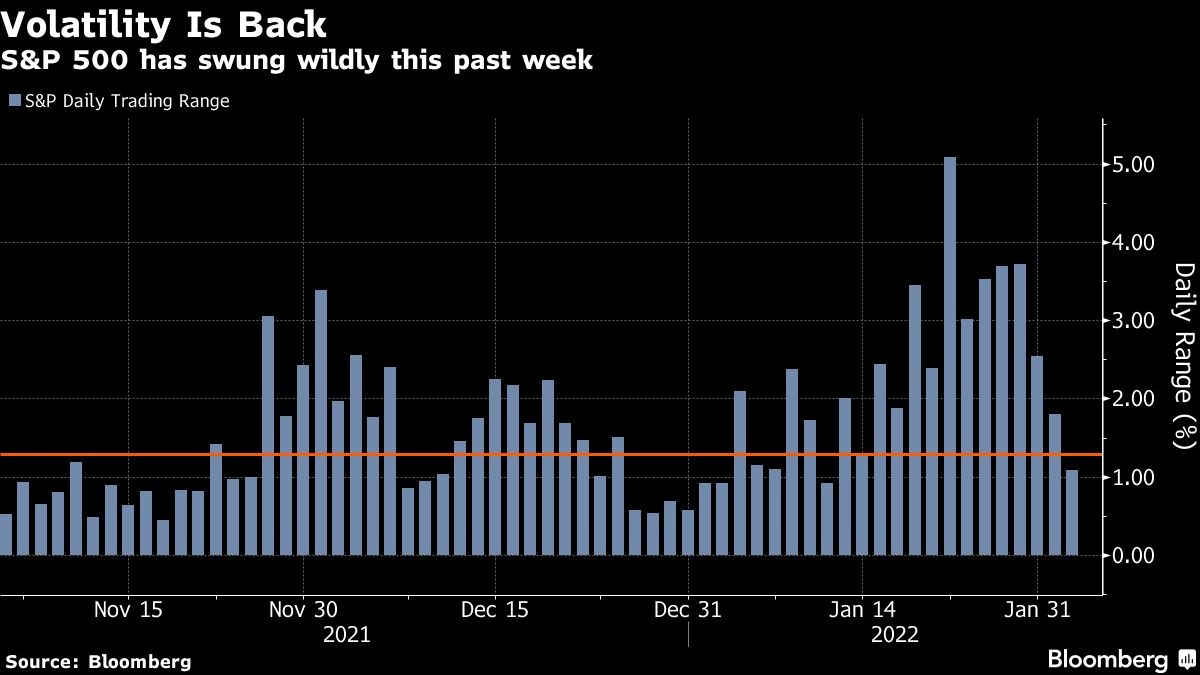

It’s been a volatile start to the year with investors swinging between concerns over Federal Reserve tightening and confidence in the economic recovery. A robust earnings outlook is helping to ease the uncertainty, at least for the moment. However, many dangers, including stubborn inflation, geopolitical risks and pandemic flare-ups still lingers in the background.

“We are seeing writ large the market tug-of-war between the reality of a changing monetary backdrop and what that means for multiples -- and eventually economic growth -- and what’s still good earnings growth,” said Peter Boockvar, chief investment officer at Bleakley Advisory Group.

The latest Fed commentary hinted at a calibrated approach to raising interest rates to fight high inflation, soothing some concerns the economy might take a hit from tighter monetary policy. None of six Fed officials speaking so far this week have backed the idea of a half-point rate increase in March, and the most aggressive, James Bullard, president of the St. Louis Fed, said five hikes -- one more than every quarter -- is “not too bad a bet.” Treasury yields dipped and the dollar was weaker.

“Fed officials backing away from a 50bp hike is important because it suggests the Fed will not aggressively offset a near-term economic rebound,” wrote Dennis DeBusschere, founder of 22V Research. “If true, that would favor a significant reversal in cyclicals, higher real yields, and reopening stock performance.”

ADP data ahead of Friday’s jobs report showed employment at U.S. companies contracted in January by the most since the early days of the pandemic with the spike omicron cases. Poor job numbers could urge the Fed to reconsider aggressive rate hikes. However, a dip in employment is not unexpected with government officials warning of the possibility in recent days.

“It was a weak number versus surveys, but not a cause for concern for the Fed in their hiking plans,” said Adam Shakoor, portfolio manager at Columbia Threadneedle Investments. “The Fed has already telegraphed the labor market as tight and near maximum employment at the end of 2021, so we should expect to see some deceleration in these figures play out in 2022.”

What to watch this week:

- Earnings are due from Amazon, Ford Motor, Meta Platforms, Qualcomm, Spotify

- Bank of England, European Central Bank rate decisions, Thursday

- Fed Board of Governors confirmation hearing, Thursday

- U.S. factory orders, initial jobless claims, durable goods, Thursday

- U.S. payrolls report for January, Friday

- Winter Olympics kick off in China, Russia’s President Vladimir Putin due to attend opening ceremony, Friday

Some of the main moves in markets:

Stocks

- The S&P 500 rose 0.9 per cent as of 4 p.m. New York time

- The Nasdaq 100 rose 0.8 per cent

- The Dow Jones Industrial Average rose 0.6 per cent

- The MSCI World index rose 0.8 per cent

Currencies

- The Bloomberg Dollar Spot Index fell 0.2 per cent

- The euro rose 0.3 per cent to US$1.1305

- The British pound rose 0.4 per cent to US$1.3571

- The Japanese yen rose 0.2 per cent to 114.46 per dollar

Bonds

- The yield on 10-year Treasuries declined one basis point to 1.78 per cent

- Germany’s 10-year yield was little changed at 0.04 per cent

- Britain’s 10-year yield declined four basis points to 1.26 per cent

Commodities

- West Texas Intermediate crude rose 0.1 per cent to US$88.32 a barrel

- Gold futures rose 0.3 per cent to US$1,807 an ounce

Advertisement