Feb 6, 2023

U.S. stock euphoria deflated with Powell as 'wild card'

, Bloomberg News

BNN Bloomberg's mid-morning market update: Feb. 6, 2023

VIDEO SIGN OUT

Stocks gave back some of this year’s gains, with traders waiting to see if Jerome Powell will dampen the bullish reaction to his recent remarks amid bets the Federal Reserve will keep its firm grip on policy.

As equities came off overbought levels, Treasuries took a hit following the best start to a year for cross-asset returns since 1987. The Fed’s boss will have an opportunity in an interview Tuesday to remind Wall Street that bets on rate cuts in 2023 are probably misplaced. Fed funds futures show another 25 basis-point hike in March as a nearly done deal, while pegging a 75 per cent chance of another one in May. The odds for a June hike have also risen.

“Fed Chair Powell remains a big wild card every time he speaks,” said Chris Senyek at Wolfe Research. “Investors will be looking to see if he ‘walks back’ his very dovish tone from last Wednesday, particularly with respect to financial conditions and the U.S. ‘disinflationary process.’ We still believe that the Fed will be ‘higher for longer’.”

Fed Bank of Atlanta President Raphael Bostic said January’s strong jobs report raises the possibility that the central bank will need to increase interest rates to a higher peak than policymakers had previously expected.

Geopolitical concerns also simmered on the background, with the U.S. preparing to impose a 200 per cent tariff on Russian-made aluminum and U.S.-listed Chinese shares tumbling as Washington’s move to shoot down an alleged surveillance balloon from the Asian nation.

A rout in megacaps like Apple Inc., Amazon.com Inc. and Google’s parent Alphabet Inc., which reported results last week, weighed on sentiment. The group’s reality check came after the Nasdaq 100 approached bull-market territory. Investors will continue to focus on earnings to figure out whether the recent rally was a “bear trap” driven by “fear of missing out,” noted Chris Larkin at E*Trade from Morgan Stanley.

“The major averages have become overbought after their strong January rallies,” said Matt Maley, chief market strategist at Miller Tabak + Co. “We are not trying to say that any short-term pullback will be followed by another strong rally. In fact, we believe that a short-term pullback could — and probably will — turn into another leg lower in the bear market that began just over a year ago.”

JPMorgan Chase & Co. strategist Marko Kolanovic reiterated that stock investors should fade last week’s Fed-induced rally, arguing the U.S. economy’s disinflationary process could just be “transitory.”

The S&P 500 now accurately reflects signs of better-than-expected economic growth and a drop in bond yields, according to Goldman Sachs Group Inc. strategists led by David Kostin. At the same time, higher valuations, lackluster corporate earnings and elevated interest rates mean there’s little room for the rally to extend, they said, a view that was broadly echoed by their counterpart at Morgan Stanley, Michael Wilson.

To Solita Marcelli at UBS Global Wealth Management, the risk-reward trade-off for equities doesn’t look appealing. She continues to recommend that equity investors position defensively and be prepared for additional volatility ahead.

“We remain bearish equities,” said Eric Johnston at Cantor Fitzgerald. “There has been a dramatic change in sentiment and positioning which has gotten much more bullish, making this a tailwind for our bearish view. And while this dramatic change has happened, the outlook for earnings, the Fed, and multiples is unchanged. All of the stock being bought now will just create that much more supply on the way down.”

Now with the path for further monetary tightening in focus, bond investors still broadly expect U.S. inflation to ebb further. The so-called breakeven rate on five-year five-year forwards — a proxy for inflation expectations — slumped to 2.18 per cent on Friday from 2.31 per cent a week prior. It was little changed Monday.

A similar gauge for 10-year inflation-linked bonds, meantime, hovered near 2.25 per cent Monday. That compares to a recent peak of 2.6 per cent in late-October, according to data compiled by Bloomberg. Separately, a recent drop in the price of gasoline futures weighed on short-term breakevens.

“Amid the ongoing race between declining inflation and a flagging economy, every data set of positive news will soon be perceived as another barrier to recession,” said Silvercrest Asset Management’s Robert Teeter. “We look for continued improvements in inflation and a persevering economy to provide modest gains on the year, with portfolio performance subject to judicious stock selection.”

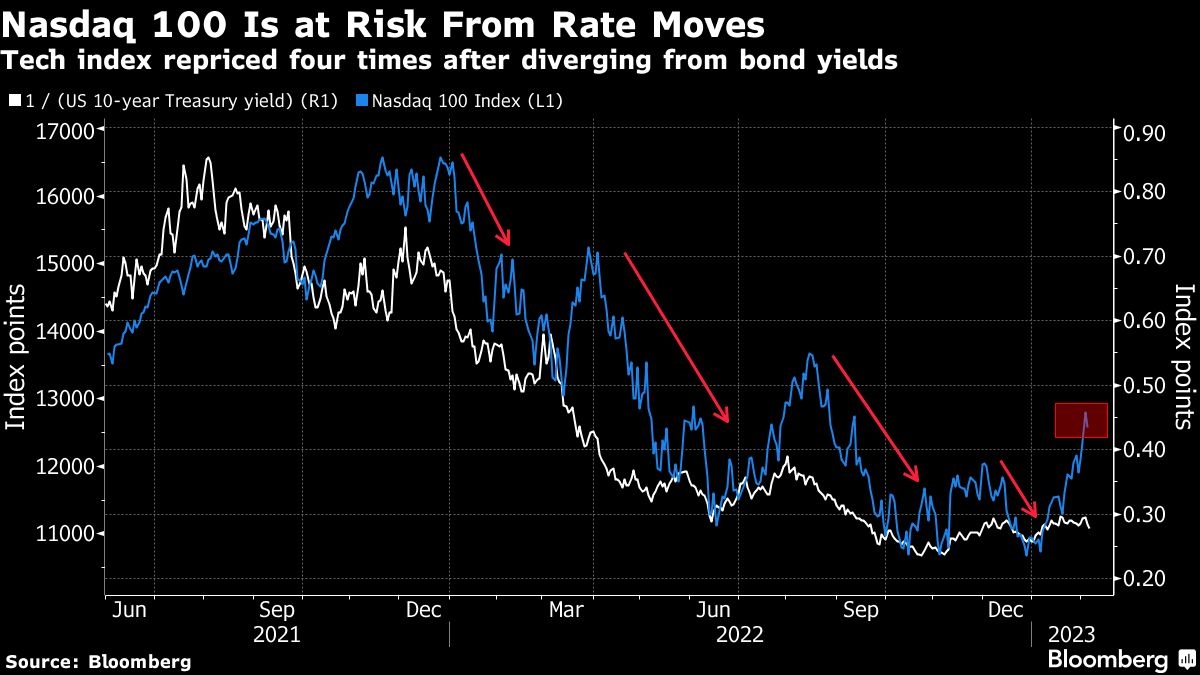

Meantime, the divergence between the Nasdaq 100 and 10-year Treasury yields is becoming extreme, which has been a negative signal for the index during the past 18 months, according to cross-asset sales trader Gurmit Kapoor. The tech-heavy benchmark has been particularly sensitive to the bond market, and has seen strong corrections during the past four occurrences when it decoupled from rates.

That doesn’t mean it’s all gloom and doom for tech stocks. The share of investors willing to increase exposure to the industry over the next six months rose to 41 per cent in the latest MLIV Pulse survey from 32 per cent in September.

In corporate news, Dell Technologies Inc. is eliminating about 6,650 roles as it faces plummeting demand for personal computers, becoming the latest technology company to announce thousands of job cuts. Tyson Foods Inc., the biggest U.S. meat company, said fiscal first-quarter earnings plunged 70 per cent from a year ago and missed expectations.

Elsewhere, the yen fell on the back of a Nikkei report that the Japanese government approached Bank of Japan Deputy Governor Masayoshi Amamiya about succeeding Haruhiko Kuroda at the helm of the central bank. A selloff in emerging markets deepened, with currencies having their biggest two-day decline since March 2020.

Key events:

- U.S. trade, Tuesday

- Fed Chair Jerome Powell interviewed by David Rubinstein at the Economic Club of Washington, Tuesday

- President Joe Biden delivers the State of the Union address before Congress, Tuesday

- U.S. wholesale inventories, Wednesday

- New York Fed President John Williams is interviewed at Wall Street Journal live event, Wednesday

- US initial jobless claims, Thursday

- ECB President Christine Lagarde participates in EU leaders summit, Thursday

- Bank of England Governor Andrew Bailey appears before Treasury Committee, Thursday

- U.S. University of Michigan consumer sentiment, Friday

- Fed’s Christopher Waller and Patrick Harker speak, Friday

Some of the main moves in markets:

Stocks

- The S&P 500 fell 0.6 per cent as of 4 p.m. New York time

- The Nasdaq 100 fell 0.9 per cent

- The Dow Jones Industrial Average fell 0.1 per cent

- The MSCI World index fell 1.1 per cent

Currencies

- The Bloomberg Dollar Spot Index rose 0.6 per cent

- The euro fell 0.6 per cent to US$1.0730

- The British pound fell 0.3 per cent to US$1.2024

- The Japanese yen fell 1.1 per cent to 132.62 per dollar

Cryptocurrencies

- Bitcoin rose 0.5 per cent to US$23,008.57

- Ether rose 1.5 per cent to US$1,647.26

Bonds

- The yield on 10-year Treasuries advanced 11 basis points to 3.63 per cent

- Germany’s 10-year yield advanced 10 basis points to 2.30 per cent

- Britain’s 10-year yield advanced 19 basis points to 3.24 per cent

Commodities

- West Texas Intermediate crude rose 1.4 per cent to US$74.41 a barrel

- Gold futures rose 0.3 per cent to US$1,881.90 an ounce