Aug 30, 2022

U.S. stocks end at lowest level in a month; oil sinks

, Bloomberg News

BNN Bloomberg's closing bell update: August 30, 2022

VIDEO SIGN OUT

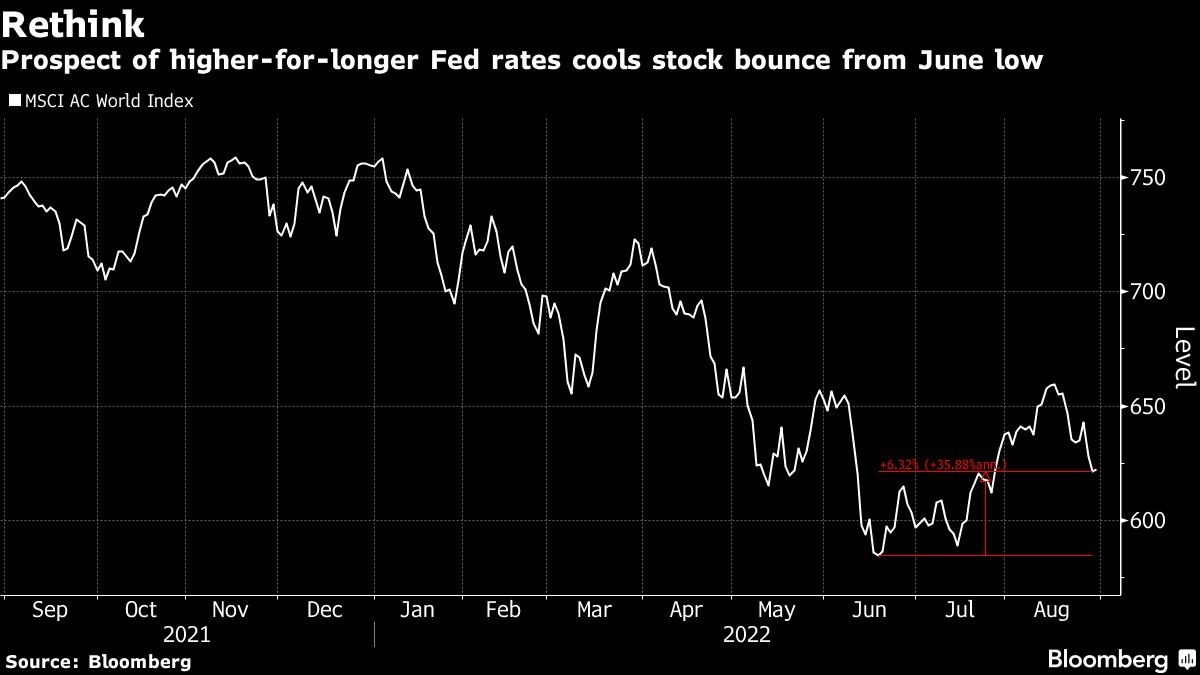

US stocks fell for the third consecutive day as fresh data pointed to resilience in household and labor demand, affirming the Federal Reserve’s resolve to continue to be aggressive in its fight against inflation. Commodities from oil to copper sank as the dollar rose.

The S&P 500 and the tech-heavy Nasdaq 100 finished the session at their lowest levels in a month. Treasuries ended Tuesday mixed after an unexpected rebound in August consumer confidence pushed swap rates toward pricing in another three-quarter percentage point hike for the Fed’s September meeting.

Three regional Fed presidents, in separate remarks on Tuesday, reiterated Chair Jerome Powell’s intention to bring down inflation. A reading on job openings Tuesday added to signs that the labor market remains tight and wage pressures persist. Jobless claims will air Thursday before Friday’s August payrolls report.

“The repercussions from Friday are going to make us extra sensitive to a lot of the incoming data, especially around employment,” said Shawn Cruz, head trading strategist at TD Ameritrade. “It’s not surprising that getting that consumer sentiment data today and the JOLTS data had a pretty strong reaction in markets. That’s probably what you should expect from now until the September Fed meeting, in particular anything around employment.”

Analysts remain mixed on what recent remarks by Fed officials and upcoming data could mean for stocks. While Credit Suisse Group AG recommended investors go underweight global equities following the Jackson Hole symposium, JPMorgan Chase & Co. strategists say that a reading on the US labor market that spells bad news for the economy is actually a bullish signal for stocks.

Meanwhile, bonds are sliding toward the first bear market in a generation, burning investors who erred in bets that central banks would pivot away from rapid interest-rate hikes.

The Fed this week is also set to step up the unwinding of its near-US$9 trillion balance sheet. The impact of quantitative tightening is going to be relatively benign for the first six to 12 months, but could start to amplify its effects on the economy around the middle part of next year, Jeff Schulze, investment strategist at ClearBridge Investments, said in an interview.

Other risks range from China’s economic slowdown to an energy crisis that threatens to tip Europe into recession with winter approaching.

Here are some key events to watch this week:

- ECB Governing Council members due to speak at event Tuesday through Sept. 2

- China PMI, Wednesday

- Euro-area CPI, Wednesday

- Russia’s Gazprom set to halt Nord Stream pipeline gas flows for three days of maintenance, Wednesday

- Cleveland Fed President Loretta Mester due to speak, Wednesday

- China Caixin manufacturing PMI, Thursday

- US nonfarm payrolls, Friday

- UK leadership ballot closes Friday. Winner announced Sept. 5

Some of the main moves in markets:

Stocks

- The S&P 500 fell 1.1 per cent as of 4 p.m. New York time

- The Nasdaq 100 fell 1.1 per cent

- The Dow Jones Industrial Average fell 1 per cent

- The MSCI World index fell 1 per cent

Currencies

- The Bloomberg Dollar Spot Index rose 0.2 per cent

- The euro rose 0.2 per cent to US$1.0019

- The British pound fell 0.5 per cent to US$1.1656

- The Japanese yen was little changed at 138.73 per dollar

Bonds

- The yield on 10-year Treasuries was little changed at 3.10 per cent

- Germany’s 10-year yield was little changed at 1.51 per cent

- Britain’s 10-year yield advanced 10 basis points to 2.70 per cent

Commodities

- West Texas Intermediate crude fell 5.1 per cent to US$92.02 a barrel

- Gold futures fell 0.8 per cent to US$1,735.70 an ounce

in New York, U.S., on Thursday, Oct. 11, 2018. U.S. stocks fell for a sixth day, extending the longest losing streak of Donald Trump's presidency, as energy shares plunged and a rally in tech failed to lift the broader market., Bloomberg")